1. COURSE DESCRIPTION

This course introduces students to the context and purpose of maintaining financial records for accounts preparation. It then concentrates in depth on the double-entry system and on recording, processing, and reporting business transactions and events, including specific accounting for non-current assets. The course also covers how to identify and correct errors, including the use of reconciliations and the posting of year-end adjustments. Finally, students will use the knowledge and skills they have developed to prepare financial statements for sole traders and partnerships.

2. REASON FOR THE COURSE

To develop knowledge and understanding of the underlying principles and concepts of maintaining financial records and technical proficiency in the use of double-entry accounting techniques.

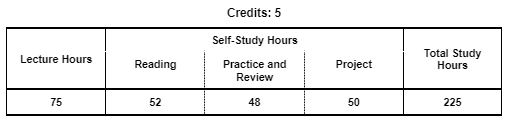

3. STUDY HOURS

4. ROLE IN CURRICULUM

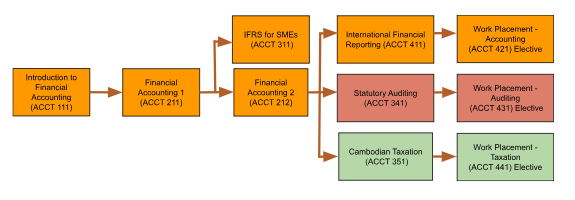

Prerequisites:

There is no prerequisite for this course.

On successful completion of this course, students will be able to:

| Knowledge | Level of Learning |

Related PLO |

|---|---|---|

| Explain the context and purpose of maintaining financial records (CK1) Explain the context and purpose of maintaining financial records for accounts preparation. |

Understand | PK1 |

| Discuss the basic accounting principles and concepts (CK2) Discuss the key accounting principles and concepts underlying the double-entry system. |

Understand | PK1 |

| Cognitive Skills | Level of Learning |

Related PLO |

| Apply the double-entry system (CC1) Record, process, and report business transactions and events using the double-entry system. |

Apply | PC5 |

| Correct accounting errors and omissions (CC2) Identify and correct errors in financial records, including the use of reconciliations and the posting of year-end adjustments. |

Apply | PC5 |

| Prepare financial statements for sole traders and partnerships (CC3) Prepare financial statements for sole traders and partnerships in accordance with international financial reporting standards. |

Apply | PC5 |

| Communication, Information Technology, and Numerical Skills | Level of Learning |

Related PLO |

| Use spreadsheets for efficient financial recording, processing and reporting (CCIT1) Use spreadsheets to automate and streamline financial tasks, including recording, processing, and reporting financial information. |

Apply | PCIT2 |

| Interpersonal Skills and Responsibilities | Level of Learning |

Related PLO |

| Be a team player and maintain confidentiality (CIP1) Work effectively as part of a team to complete accounting tasks and meet deadlines, while maintaining confidentiality of accounting information. |

Value | PIP1 |

Grades will be determined based on the following assessments and score allocations:

| SKILL | Assessment | Skill Weighting for Grade | |||||

|---|---|---|---|---|---|---|---|

| Participation | In-class tests | Midterm Project | Final Project | Final Exam | |||

| Explain the context and purpose of maintaining financial records (CK1) | 100% | 5% | |||||

| Discuss the basic accounting principles and concepts (CK2) | 50% | 50% | 10% | ||||

| Apply the double-entry system (CC1) | 30% | 40% | 30% | 30% | |||

| Correct accounting errors and omissions (CC2) | 30% | 40% | 30% | 15% | |||

| Prepare financial statements (CC3) | 30% | 40% | 30% | 20% | |||

| Use spreadsheets for efficient financial recording, processing and reporting (CCIT1) | 50% | 50% | 10% | ||||

| Be a team player (CIP1) | 50% | 50% | 10% | ||||

This course uses a variety of teaching methods to engage students and promote learning, including lectures, discussions, didactic questioning, case study analysis, demonstrations, written examinations, and group projects.

| Midterm Project: | Financial Reporting in Practice (CK1, CIP1) |

| Work Group: | Group |

| Output Format: | APA Format Report, Presentation |

| Language: | English |

| Description: | Students will work in groups of 3-5 to document the accounting and financial reporting process of a medium to large size business or organization. The project requires meetings, interviews and site visits to the target business or organization in Cambodia. |

| Final Project: | Bookkeeping Simulation (CC1,CC2, CC3, CCIT1, CIP1) |

| Work Group: | Group |

| Output Format: |

Accounting Records and Financial Reports in Spreadsheets |

| Language: | English |

|

Description:

|

Students will work in groups of 3-5 to record, process, and report business transactions using the double-entry system. Students will also be required to identify and correct errors in financial records, prepare financial statements for sole traders or partnerships, and utilize spreadsheets for efficient financial recording, processing, and reporting. |

The course targets the 50 lessons in the study plan below. Each lesson is 1.5 class hours each; there are a total of 75 class hours. The study plan below describes the learning outcome for each lesson, described in terms of what the student should be able to do at the end of the lesson. Readings should be done by students as preparation before the start of each class. Implementation of this study plan may vary somewhat depending on the progress and needs of students.

| Lesson Learning Outcomes | Teaching (T), and Assessment (A) Methods | |

|---|---|---|

| 1 |

Accounting principles, concepts and characteristics 1

|

Lecture (T) Reading: Chapter 1 |

| 2 |

Accounting principles, concepts and characteristics 1

|

Lecture (T) Reading: Chapter 1 |

| 3 |

The elements of financial statements

|

Lecture (T) Reading: Chapter 2 |

| 4 |

Overview of the accounting process

|

Lecture (T) Reading: Chapter 2 |

| 5 |

Preparation of journal entries

|

Lecture (T) Reading: Chapter 2 |

| 6 |

Preparation of general ledger accounts 1

|

Lecture (T) Reading: Chapter 2 |

| 7 |

Preparation of general ledger accounts 2

|

Lecture (T) Reading: Chapter 2 |

| 8 |

Sales and purchases

|

Lecture (T) Reading: Chapter 3 |

| 9 |

Cash and bank

|

Lecture (T) Reading: Chapter 3 |

| 10 |

Trade and settlement discounts

|

Lecture (T) Reading: Chapter 3 |

| 11 |

Sales tax

|

Lecture (T) Reading: Chapter 3 |

| 12 |

Inventories 1

|

Lecture (T) Reading: Chapter 4

|

| 13 |

Inventories 2

|

Lecture (T) Reading: Chapter 4 |

| 14 |

Inventories 3

|

Lecture (T) Reading: Chapter 5 |

| 15 |

Noncurrent assets

|

Lecture (T) Reading: Chapter 5 |

| 16 |

Acquisition of noncurrent assets

|

Lecture (T) Reading: Chapter 5 |

| 17 |

Depreciation of non-current assets 1

|

Lecture (T) Reading: Chapter 6 |

| 18 |

Depreciation of non-current assets 2

|

Lecture (T) Reading: Chapter 6 |

| 19 |

Disposal of non-current assets

|

Lecture (T) Discussion (T) Learning Activity on Google Sheets (A) Reading: Chapter 6 |

| 20 |

Noncurrent asset register

|

Lecture (T) Reading: Chapter 5 |

| 21 |

Accrued expenses (accruals)

|

Lecture (T) Reading: Chapter 7 |

| 22 |

Prepaid expenses (prepayments)

|

Lecture (T) Reading: Chapter 7 |

| 23 |

Accrued income and unearned income

|

Lecture (T) Reading: Chapter 7 |

| 24 |

Trade and other receivables

|

Lecture (T) Reading: Chapter 8 |

| 25 |

Irrecoverable debts and allowance for receivables 1

|

Lecture (T) Reading: Chapter 8 |

| 26 |

Irrecoverable debts and allowance for receivables 2

|

Lecture (T) Reading: Chapter 8 |

| 27 |

Trade and other payables

|

Lecture (T) Reading: Chapter 9 |

| 28 |

Provisions

|

Lecture (T) Reading: Chapter 9 |

| 29 |

Capital and finance costs

|

Lecture (T) Reading: Chapter 9 |

| 30 |

Bank reconciliation 1

|

Lecture (T) Reading: Chapter 10 |

| 31 |

Bank reconciliation 2

|

Lecture (T) Reading: Chapter 10 |

| 32 |

Petty cash

|

Lecture (T) Reading: Chapter 10 |

| 33 |

Supplier statement reconciliation

|

Lecture (T) Reading: Chapter 10 |

| 34 |

Initial trial balance

|

Lecture (T) Reading: Chapter 11 |

| 35 |

Correction of errors 1

|

Lecture (T) Reading: Chapter 11 |

| 36 |

Correction of errors 2

|

Lecture (T) Reading: Chapter 11 |

| 37 |

Suspense accounts

|

Lecture (T) Reading: Chapter 11 |

| 38 |

Accounting for year-end adjustments

|

Lecture (T) Reading: Chapter 12 |

| 39 |

Sole trader financial statements 1

|

Lecture (T) Reading: Chapter 13 |

| 40 |

Sole trader financial statements 2

|

Lecture (T) Reading: Chapter 13 |

| 41 |

Closing entries and post-closing trial balance

|

Lecture (T) Reading: Chapter 13 |

| 42 |

Partnership financial statements

|

Lecture (T) Reading: Chapter 14 |

| 43 |

Partnership financial statements

|

Lecture (T) Reading: Chapter 14 |

| 44 |

Partnership financial statements

|

Lecture (T) Reading: Chapter 14 |

| 45 |

Incomplete records 1

|

Lecture (T) Reading: Chapter 15 |

| 46 |

Incomplete records 2

|

Lecture (T) Reading: Chapter 15 |

| 47 | Review and preparation for final exam (All CLOs) | Lecture |

| 48 | Review and preparation for final exam (All CLOs) | Lecture |

| 49 | Review and preparation for final exam (All CLOs) | Lecture |

| 50 | Review and preparation for final exam (All CLOs) | Lecture |

| Total Hours | ||

Textbooks

References