1. COURSE DESCRIPTION

This course introduces the students to the fundamentals of the regulatory framework relating to financial reporting and to the qualitative characteristics of useful information. Students will gain a solid understanding of the fundamentals and principles of account preparation, including the process of recording, processing, and reporting business transactions and events. The course also covers important topics such as reconciliations, trial balance preparation, error correction, and suspense accounts, all of which are essential for preparing accurate financial statements for incorporated and unincorporated entities. Additionally, students will learn how to prepare consolidated financial statements for a parent company with a single subsidiary. While the primary focus of the course is on mastering the preparation of the main financial statements, there is also a concise overview of notes and disclosures. In the final sessions, students will develop the ability to analyze and interpret financial statements.

2. REASON FOR THE COURSE

This course aims to develop students’ knowledge of the principles and concepts of financial accounting, as well as their proficiency in using double-entry accounting techniques to prepare basic financial statements in accordance with IFRS.

Nearly all roles that bachelor of accounting and finance graduates pursue will require extensive interaction with financial statements. For example, graduates may work as financial accountants who are responsible for preparing financial statements, investors or investment analysts who collate and analyze data drawn from financial statements, or auditors who assess whether financial statements comply with relevant accounting standards.

Therefore, it is essential that graduates have a deep and firm knowledge of financial accounting. This course will provide them with the skills and knowledge they need to be successful in their careers.

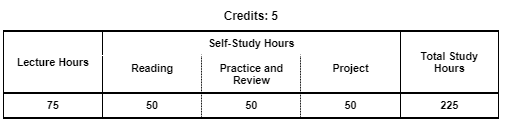

3. STUDY HOURS

4. ROLE IN CURRICULUM

Prerequisites:

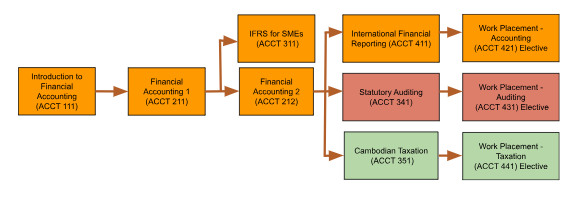

Students must have successfully passed Financial Accounting I (ACCT 211) before attempting this course.

On successful completion of this course, students will be able to:

| Knowledge | Level of Learning |

Related PLO |

|---|---|---|

| Discuss the regulatory framework, qualitative characteristics, and basic principles of financial reporting (CK1) Discuss the regulatory framework for financial reporting, the qualitative characteristics of useful financial information, and basic accounting principles. |

Understand | PC5 |

| Cognitive Skills | Level of Learning |

Related PLO |

| Apply accounting principles and techniques (CC1) Apply the fundamental accounting principles and techniques to accurately record, process, and report business transactions and events. |

Apply | PC5 |

| Perform reconciliations, prepare trial balance, correct errors, and manage suspense accounts (CC2) Perform reconciliations, prepare trial balance, correct errors, and manage suspense accounts to ensure the accuracy and reliability of financial statements for both incorporated and unincorporated entities. |

Apply | PC5 |

| Prepare basic and consolidated financial statements (CC3) Prepare financial statements for both single companies and groups of companies. |

Create | PC5 |

| Analyze and interpret financial statements (CC4) Analyze and interpret financial statements to assess a company’s financial performance and position, identify trends and patterns, and make informed decisions about the company’s business. |

Analyze | PC1 |

| Communication, Information Technology, and Numerical Skills | Level of Learning |

Related PLO |

| Use spreadsheets and accounting software (CCIT1) Use spreadsheets and accounting software to efficiently prepare, analyze, and interpret financial statements. |

Apply | PCIT2 |

| Interpersonal Skills and Responsibilities | Level of Learning |

Related PLO |

| Collaborate with team members and demonstrate ethics and professionalism in financial reporting (CIP1) Collaborate effectively with team members and demonstrate ethical and professional behavior in the preparation and presentation of financial statements. |

Value | PIP2 |

Grades will be determined based on the following assessments and score allocations:

| SKILL | Assessment | Skill Weighting for Grade | ||||

|---|---|---|---|---|---|---|

| Participation | In-Class Test | Accounting simulation | Final Exam | |||

| Discuss the regulatory framework, qualitative characteristics, and basic principles of financial reporting (CK1) | 90% | 10% | 10% | |||

| Apply accounting principles and techniques (CC1) | 50% | 20% | 30% | 30% | ||

| Perform reconciliations, prepare trial balance, correct errors, and manage suspense accounts (CC2) | 50% | 20% | 30% | 10% | ||

| Prepare basic and consolidated financial statements (CC3) | 30% | 70% | 20% | |||

| Analyze and interpret financial statements (CC4) | 50% | 50% | 10% | |||

| Use spreadsheets and accounting software (CCIT1) | 100% | 10% | ||||

| Collaborate with team members and demonstrate ethics and professionalism in financial reporting (CIP1) | 100% | 10% | ||||

This course is taught with a variety of teaching methods, including lecture, discussion, didactic questioning, case study analysis, demonstration, and group work.

During the course, there is one Project:

| Assignment: |

Accounting simulation (All CLOs) |

| Group Work: | Group of 5 |

| Output Format |

The outputs will be submitted in 5 phases: |

| Language: | English |

| Description: |

This project aims to:

|

The course targets the 50 lessons in the study plan below. Each lesson is 1.5 class hours each; there are a total of 75 class hours. The study plan below describes the learning outcome for each lesson, described in terms of what the student should be able to do at the end of the lesson. Readings should be done by students as preparation before the start of each class. Implementation of this study plan may vary somewhat depending on the progress and needs of students.

| No | Lesson Learning Outcomes | Teaching (T), and Assessment (A) Methods |

|---|---|---|

| 1 |

Review of accounting basics

|

Lecture (T) Reading: Chapter 1 |

| 2 |

Business Entities

|

Lecture (T) Reading: Chapter 1 |

| 3 |

The qualitative characteristics of financial information

|

Lecture (T) Reading: Chapter 1 |

| 4 |

The Regulatory Framework and Corporate Governance

|

Lecture (T) Reading: Chapter 2 |

| 5 |

Business transactions and documentation

|

Lecture (T) Reading: Chapter 3 |

| 6 |

Ledger accounts and double entry

|

Lecture (T) Reading: Chapter 5 |

| 7 |

From trial balance to financial statements

|

Demonstration of balancing off ledger accounts and preparing a trial balance (T) Reading: Chapter 6 |

| 8 |

From trial balance to financial statements

|

Discussion on limitations of a trial balance (T) Reading: Chapter 6 |

| 9 |

Inventory

|

Lecture (T) Reading: Chapter 7 |

| 10 |

Inventory

|

Lecture (T) Demonstration of accounting entries under continuous and periodic inventory systems (T) Reading: Chapter 7 |

| 11 |

Inventory

|

Lecture (T) Reading: Chapter 7

|

| 12 |

Property, Plant and Equipment

|

Lecture (T) Reading: Chapter 8 |

| 13 |

Property, Plant and Equipment

|

Lecture (T) Reading: Chapter 8 |

| 14 |

Property, Plant and Equipment

|

Lecture (T) Reading: Chapter 8 |

| 15 |

Intangible non-current assets

|

Lecture (T) Reading: Chapter 9 |

| 16 |

Accruals and prepayments

|

Lecture (T) Reading: Chapter 10 |

| 17 |

Accruals and prepayments

|

Lecture (T) Reading: Chapter 10 |

| 18 |

Provisions and contingencies

|

Lecture (T) Reading: Chapter 11 |

| 19 |

Irrecoverable debts and allowances

|

Demonstration of determining and recording bad debts (T) Reading: Chapter 12 |

| 20 |

Irrecoverable debts and allowances

|

Demonstration of determining and recording movements in allowance for receivables (T) Reading: Chapter 12 |

| 21 |

Sales Tax

|

Lecture (T) Reading: Chapter 13 |

| 22 |

Receivables and Payables

|

Lecture (T) Reading: Chapter 14 |

| 23 |

Bank reconciliations

|

Lecture and discussion (T) Reading: Chapter 15 |

| 24 |

Bank reconciliations

|

Group problem based learning (T) Reading: Chapter 15 |

| 25 |

Correction of errors

|

Lecture and discussion (T) Demonstration of use of suspense account (T) Group problem based learning to solve errors using a suspense account (T) Spreadsheet exercise on correction of errors (A) Reading: Chapter 16 |

| 26 |

Incomplete records

|

Lecture (T) Reading: Chapter 17 |

| 27 |

Preparation of financial statements for sole traders

|

Demonstration of preparation of a statement of profit or loss and a statement of financial position (T) Reading: Chapter 18 |

| 28 |

Introduction to company accounting

|

Lecture (T) Reading: Chapter 19 |

| 29 |

Preparation of financial statements for companies

|

Lecture (T) Reading: Chapter 20

|

| 30 |

Preparation of financial statements for companies

|

Demonstration of preparation of financial statements (T) Reading: Chapter 20 |

| 31 |

Preparation of financial statements for companies

|

Demonstration of preparation of financial statements (T) Reading: Chapter 20 |

| 32 |

Preparation of financial statements for companies

|

Lecture (T) Reading: Chapter 20 |

| 33 |

Preparation of financial statements for companies, Events after the reporting period

|

Lecture (T) Reading: Chapter 20, 21 |

| 34 |

Statement of cash flows

|

Lecture (T) Reading: Chapter 22 |

| 35 |

Statement of cash flows

|

Demonstration of preparation of a statement of cash flows (T) Reading: Chapter 22 |

| 36 |

Statement of cash flows

|

Demonstration of preparation of a statement of cash flows (T) Reading: Chapter 22 |

| 37 |

Statement of cash flows

|

Demonstration of preparation of a statement of cash flows (T) Reading: Chapter 22 |

| 38 |

Introduction to consolidated financial statements

|

Lecture (T) Reading: Chapter 23 |

| 39 |

The consolidated statement of financial position

|

Demonstration of preparation of a consolidated statement of financial position (T) Reading: Chapter 24 |

| 40 |

The consolidated statement of financial position

|

Group case study to prepare a consolidated statement of financial position (T) Reading: Chapter 24 |

| 41 |

The consolidated statement of financial position

|

Lecture (T) Reading: Chapter 24 |

| 42 |

The consolidated statement of profit or loss

|

Demonstration of preparation of a consolidated statement of profit or loss (T) Reading: Chapter 25 |

| 43 |

The consolidated statement of profit or loss

|

Demonstration of preparation of a consolidated statement of profit or loss (T) Reading: Chapter 25

|

| 44 |

The consolidated statement of profit or loss

|

Demonstration of preparation of a consolidated statement of profit or loss (T) Reading: Chapter 25 |

| 45 |

Analysis and interpretation of financial statements

|

Case analysis and discussion (T) Reading: Chapter 26 |

| 46 |

Analysis and interpretation of financial statements

|

Group case study analysis (T) Reading: Chapter 26 |

| 47 |

Analysis and interpretation of financial statements

|

Group case study analysis (T) Reading: Chapter 26 |

| 48 |

Analysis and interpretation of financial statements

|

Group problem sets (T) Reading: Chapter 26 |

| 49 | Review and preparation for final exam (All CLOs) | Lecture |

| 50 | Review and preparation for final exam (All CLOs) | Lecture |

| Total Hours | ||

Textbooks

References