1. COURSE DESCRIPTION

This course begins with a review of key IFRS principles, continuing to study each IFRS in detail, with continuous reference to the relevant IFRS standards. In the first week, the course covers the conceptual framework which describes the fundamental accounting concepts. We will then cover non-current assets, leases, inventory, biological assets and revenue. This is followed by provisions, foreign exchange, financial instruments and taxes. Then, we will look at applicable IFRS at the year end including retrospective treatment, events after reporting period and earnings per share. At this point of the course, students will have a good knowledge of various IFRS in order to prepare a full set of financial statements from a trial balance. After preparing financial statements on an accruals basis, the course will cover ratios and statement of cash flows. Towards the end of the course, the subject of study is consolidation of subsidiaries and accounting for associates.

2. REASON FOR THE COURSE

This course aims to develop knowledge and skills for understanding and applying accounting standards and the theoretical framework for the preparation of financial statements of entities, including groups, and for analyzing and interpreting those financial statements. The course focuses on the application of IFRS in financial reporting because in Cambodia, IFRS and IFRS for SMEs are required by law for all companies meeting certain size requirements. The regional and international trend is that IFRS is becoming increasingly common for financial reporting.

Accounting and finance graduates will face extensive interaction with financial statements. This may be in the role of a financial accountant, responsible for preparing the financial statements. It may also be in the role of a lender, or investment analyst utilizing data drawn from the financial statements. It could be in the role of an auditor whose responsibility includes assessing whether financial statements comply with the relevant accounting standards. Thus, it is essential to have a deep and firm knowledge of financial reporting and the standards used in financial reporting.

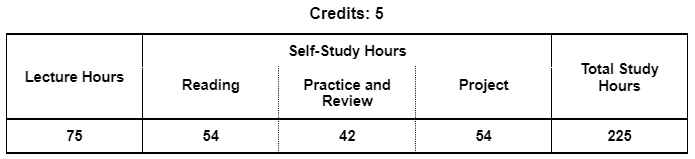

3. STUDY HOURS

4. ROLE IN CURRICULUM

Prerequisites:

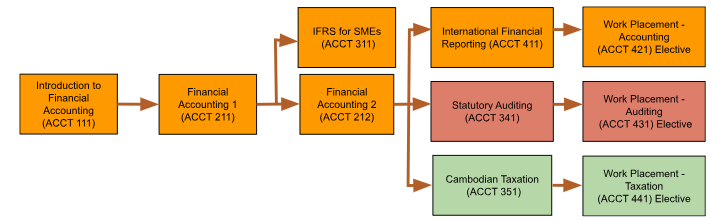

Students must have finished Financial Accounting 1 and 2 before attempting this course.

On successful completion of this course, students will be able to:

| Knowledge | Level of Learning | Related PLO |

|---|---|---|

| Describe IFRS (CK1) Explain the objective and applicability of IFRS to various business transactions |

Understand | PC5 |

| Cognitive Skills | Level of Learning | Related PLO |

| Apply IFRS (CC1) Apply IFRS to a broad range of transactions and recognition and measurement of assets and liabilities common to large companies and multinationals. |

Analyze | PC5 |

| Prepare a Financial Report (CC2) Construct the four main financial statements for a large company in compliance with IFRS. |

Create | PC5 |

| Appraise business performance and position using financial statement analysis from the perspective of an investor. | Evaluate | PC1 |

| Communication, Information Technology, and Numerical Skills | Level of Learning | Related PLO |

| Prepare financial statements of a listed company in Cambodia (CCIT1) Utilize spreadsheets to facilitate financial statement analysis and financial reporting. |

Apply | PCIT1 |

| Interpersonal Skills and Responsibilities | Level of Learning | Related PLO |

| Work Ethically (CIP1) Exercise professionalism and professional skepticism in financial reporting and analysis. |

Characterize | PIP2 |

Grades will be determined based on the following assessments and score allocations:

| SKILL | Assessment | Skill Weighting for Grade | ||||

|---|---|---|---|---|---|---|

| Participation | Project | Controlled Case Studies | Final Controlled Case Study | |||

| Describe IFRS (CK1) | 50% | 50% | 10% | |||

| Apply IFRS (CC1) | 50% | 50% | 10% | |||

| Prepare a Financial Report (CC2) | 40% | 60% | 40% | |||

| Prepare financial statements of a listed company in Cambodia (CCIT1) | 100% | 30% | ||||

| Work Ethically (CIP1) | 100% | |||||

This course is primarily lecture based; assigned readings will support learning and serve as a reference to material covered in class. During class, approximately half of the class will be devoted to lectures with another half of the class for working on and reviewing the solutions to case studies and problem sets.

During the course, there is one Project:

| Assignment: | Company’s Performance Analysis (CC3) |

| Work Group: | Individual |

| Output format: | APA Format Report |

| Language: | English |

| Description: |

At the end of the course, each student will choose a public company that follows IFRS (the company’s last year’s annual report has to be available in English). Companies will be chosen on the first-come, first-served basis and this process will be moderated by the instructor. Students will conduct an analysis of the company’s strategic position, performance and conclude as to whether the business should be considered as a potential investment. |

The course targets the 50 lessons in the study plan below. Each lesson is 1.5 class hours each; there are a total of 75 class hours. The study plan below describes the skills to be learned in each lesson (learning outcome). Readings should be completed before the start of each class. Implementation of this study plan may vary depending on the progress and needs of students. References are supporting documents which students may optionally read for deeper understanding or clarification.

| Lesson Learning Outcomes | Teaching and Learning Activities, Assessment | |

|---|---|---|

| 1 |

Course Introduction, Financial Statement Analysis

|

Lecture Discussion Kahoot!Reading: References: BPP Text Chapter 1 pp 4-8, Chapter 2 pp 31-35, Chapter 19 |

| 2 |

Financial Statement Analysis

|

Lecture Discussion Case studyReading: References: BPP Text Essential Reading 19 pp 704-706, Chapter 19 |

| 3 |

Cash Flow Statement

|

Lecture Demonstration and discussion Case StudyReading: References: BPP Text Chapter 21 pp 525-546 |

| 4 |

Cash Flow Statement

|

Case Study Reading: References: BPP Text Chapter 21 pp 525-546 |

| 5 |

Foreign Currency Gains and Losses

|

Lecture Discussion Group ExerciseReading: References: BPP Text Chapter 17 pp 421-442 |

| 6 |

Foreign Currency Translations

|

Lecture Discussion Group ExerciseReading: References: BPP Text Chapter 17 pp 421-442 |

| 7 |

EPS

|

Lecture Discussion Group exerciseReading: References: BPP Text Chapter 18 pp 455-476 |

| 8 |

Diluted EPS

|

Lecture Demonstration and discussion Case study discussionReading: References: BPP Text Chapter 18 pp 455-476 |

| 9 |

Business and Industry Analysis

|

Lecture Demonstration and discussion Example and exerciseReading: References: BPP Text Chapter 19 pp 477-510 |

| 10 |

Revaluation of Property Plant and Equipment

|

Lecture Demonstration Example, exercise and group problem solvingReading: References: BPP Text Chapter 3 pp 45-70 |

| 11 |

Revaluation of Property Plant and Equipment

|

Lecture Demonstration Example, exercise and group problem solvingReading: References: BPP Text Chapter 3 pp 45-70 |

| 12 |

Investment Property

|

Lecture Demonstration and discussion Example and exerciseReading: References: BPP Text Chapter 3 pp 45-70 |

| 13 |

Borrowing Costs

|

Lecture Case study discussion Group problem solvingReading: References: BPP Text Chapter 3 pp 45-70 |

| 14 |

Intangible Assets

|

Lecture Discussion Group exerciseReading: References: BPP Text Chapter 4 pp 71-90 |

| 15 |

Impairment of Assets

|

Lecture Discussion Group exerciseReading: References: BPP Text Chapter 5 pp 91-106 |

| 16 |

Provisions

|

Lecture Discussion Group exerciseReading: References: BPP Text Chapter 13 pp 329-354 |

| 17 |

Inventory, Biological Assets

|

Lecture Discussion Group exerciseReading: References: BPP Text Chapter 14 pp 355-368 |

| 18 |

Financial Instruments

|

Lecture Demonstration and discussion Example and exerciseReading: References: BPP Text Chapter 11 pp 277-298 |

| 19 |

Convertible Loans

|

Lecture Discussion Group ExerciseReading: References: BPP Text Chapter 11 pp 277-298 |

| 20 |

Lessee Lease Accounting

|

Lecture Example and exercise Group problem solving Case study discussion.Reading: References: BPP Text Chapter 12 pp 299-322 |

| 21 |

Lessor Lease Accounting

|

Lecture Example and exercise Group problem solving Case study discussion.Reading: References: BPP Text Chapter 12 pp 299-322 |

| 22 |

Sale and Leaseback Transactions

|

Lecture Example and exercise Group problem solving Case study discussion.Reading: References: BPP Text Chapter 12 pp 299-322 |

| 23 |

Leases: Review and Practice

|

Lecture Case study discussion Group exerciseReading: References: BPP Text Chapter 12 pp 299-322 |

| 24 |

Financial Statement Adjustments for Financial Statement Analysis

|

Case study discussion Reading: References: BPP Text Chapter 19 pp 477-510, Chapter 20 pp 511-524 |

| 25 |

Revenue

|

Lecture Discussion Group exerciseReading: References: BPP Text Chapter 6 pp 117-142 |

| 26 |

Revenue from Construction Contracts

|

Lecture Discussion Group exerciseReading: References: BPP Text Chapter 6 pp 117-142 |

| 27 |

Government Grants

|

Lecture Discussion Group exerciseReading: References: BPP Text Chapter 6 pp 117-142 |

| 28 |

Income Tax – Deferred Tax

|

Lecture Discussion Group exerciseReading: References: BPP Text Chapter 15 pp 369-392 |

| 29 |

Income Tax – Deferred Tax

|

Lecture Discussion Group exerciseReading: References: BPP Text Chapter 15 pp 369-392 |

| 30 |

Income Tax – Disclosures

|

Lecture Discussion Group exerciseReading: References: BPP Text Chapter 15 pp 369-392 |

| 31 |

Consolidated Statement of Financial Position

|

Lecture Discussion Group exerciseReading: References: BPP Text Chapter 7 pp 153-176, Chapter 8 pp 177-218 |

| 32 |

Consolidated Statement of Financial Position – Unrealised Profit, Goodwill

|

Lecture Discussion Group exerciseReading: References: BPP Text Chapter 8 pp 177-218 |

| 33 |

Consolidated Statement of Financial Position – Fair Value Adjustments

|

Lecture Discussion Group exerciseReading: References: BPP Text Chapter 8 pp 177-218 |

| 34 |

Consolidated Statement of Profit and Loss and Other Comprehensive Income

|

Lecture Demonstration Case study discussion Group exerciseReading: References: BPP Text Chapter 9 pp 219-242 |

| 35 |

Group Disposals

|

Lecture Demonstration Case study discussion Group exercise Reading:References: BPP Text Chapter 9 pp 219-242 |

| 36 |

Financial Statement Analysis of Groups

|

Case study discussion Reading: References: BPP Text Chapter 9 pp 219-242 |

| 37 |

Accounting for Associates

|

Lecture Discussion Group exerciseReading: References: BPP Text Chapter 10 pp 243-266 |

| 38 |

Consolidation with Associates

|

Lecture Discussion Group exerciseReading: References: BPP Text Chapter 10 pp 243-266 |

| 39 |

Changes in Policy and Estimates, Errors,Events After the Reporting Period

|

Lecture Discussion Group exerciseReading: References: BPP Text Chapter 13 pp 328-355, Chapter 17 pp 421-442 |

| 40 |

Non-Current Assets Held for Sale, Discontinued Operations

|

Lecture Case study discussion Group problem solvingReading: References: BPP Text Chapter 17 pp 421-442 |

| 41 | Practice | |

| 42 | Practice | |

| 43 | Practice | |

| 44 | Practice | |

| 45 | Practice | |

| 46 | Practice | |

| 47 | Practice | |

| 48 | Practice | |

| 49 | Practice | |

| 50 | Final Assignment Presentations | |

| Total Hours | 75 hours |

Textbooks

References