Print ISSN : 2708-616X | Online ISSN : 2708-6178 | Title DOI: https://doi.org/10.62458/160224

Volume 9 | Number 2 | July – December 2024 | DOI: https://doi.org/10.62458/jafess921

Received : July 2024 | Revised: September 2024 | Accepted: December 2024

Juliet Cadungog-Uy, Ph.D.

CamEd Business School

Email: [email protected]

Edman Padilla Flores, CPA, MBA ![]()

CamEd Business School, Cambodia

Email: [email protected]

ABSTRACT

Purpose: This study aims to assess the financial literacy awareness and practices of village savings group members in rural Cambodia, focusing on their earning, saving, spending, borrowing, insurance coverage, financial concepts awareness, and use of mobile applications.

Methodology: The study employed a quantitative research approach, surveying 109 savings group members from 24 villages in Cambodia’s Kampot and Kampong Thom provinces using a structured questionnaire administered through face-to-face interviews. The collected data were then analyzed using descriptive statistics.

Findings: The study identified a relatively strong financial literacy among the respondents, indicating the potential for further capacity building. However, significant barriers to financial inclusion and access to formal financial services were revealed. The study also highlighted gaps in insurance coverage, particularly for agricultural and health risks, and limited use of mobile financial applications.

Implications: The findings highlight the urgent need for targeted interventions to improve access to formal financial services, strengthen insurance product uptake, and address challenges in using digital financial tools in rural Cambodia.

Originality: This study offers detailed micro-level insights into the financial literacy, practices, and challenges of village savings group members, which is essential for developing effective strategies to enhance financial inclusion.

Limitations and directions for future research: The findings may not be generalizable to other contexts, as the study was conducted within a specific rural community. Future research could explore financial practices in different geographical and socioeconomic settings and delve into the root causes of barriers to inform targeted interventions and policy recommendations.

Keywords: Financial literacy; Savings groups; Financial inclusion; Rural Cambodia

INTRODUCTION

Financial literacy, a critical life skill, encompasses the knowledge, attitudes, and behaviors necessary for informed financial decision-making and problem-solving. It is the bedrock of financial sustainability for individuals, families, enterprises, and national economies (Swiecka et al., 2020; Zaimovic et al., 2023). Understanding concepts like budgeting, saving, investing, and avoiding financial fraud is essential for effective personal and family financial management (Baranova et al., 2024; Gadzhiev et al., 2024), ultimately contributing to broader economic prosperity and stability.

However, Cambodia faces a pressing challenge. Despite the Royal Government of Cambodia’s National Financial Inclusion Strategy (NFIS) 2019-2025, financial literacy remains a significant barrier to inclusion. Cambodia’s financial literacy score is a concerning 18%, ranking 135th out of 144 countries surveyed (Royal Government of Cambodia, 2019). This score is significantly lower than neighboring countries like Vietnam (24%) and Thailand (27%), placing Cambodia on par with Nepal and Haiti (Klapper et al., n.d.).

The implications of this lack of financial literacy are profound. Recent studies, including Samreth et al. (2024), highlight the crucial role of financial literacy in enhancing financial inclusion and reducing reliance on informal finance with its exorbitant interest rates. Their research identifies a strong correlation between financial literacy, general education levels, household income, and social capital, underscoring the need for targeted financial education programs, particularly for lower-income households. Further studies emphasize the importance of tailored financial education programs, community involvement, and the integration of financial literacy into broader educational curricula to improve financial outcomes and support economic development in Cambodia (Tes & Heng, 2024; Chet et al., 2023).

This study aims to support a Cambodian NGO working on community-savings group projects in rural areas of Cambodia’s Kampot and Kampong Thom provinces. With a growing population of 858 savings group members, primarily women, these groups have raised an accumulated savings of more than $80,000, averaging $1,000 to $1,500 per group. The savings groups have kept their money in a metal box, with one officer keeping the box, one holding the key, and another member recording their group transactions.

The savings members have started income-generating activities such as small businesses, home gardening, livestock raising, organic farming, drinking water production, selling food or sugarcane juice, operating a fish pond, and other cultivations. In addition, the community-saving groups serve as platforms for disseminating health and nutrition messages and other information.

This study is significant as it assesses savings group members’ financial literacy awareness and practices. It focuses on their earning and saving practices, spending and borrowing practices, protection and insurance coverage, financial concepts awareness and use of mobile applications, barriers to accessing bank services, and knowledge and skills they want to learn. The findings from this study will provide valuable insights to policymakers, educators, and financial institutions, guiding them in formulating strategies and programs to enhance financial literacy, promote financial inclusion, and ultimately drive economic growth in Cambodia. This is not just about improving individual financial outcomes but also about building a more prosperous and stable Cambodia.

The next section reviews related literature, followed by an outline of the research methodology. The fourth section presents the study’s findings and discusses previous studies’ findings. The final section offers concluding remarks.

LITERATURE REVIEW

Financial literacy is a fundamental component in fostering economic development at both individual and national levels. It encompasses the knowledge and skills necessary to make informed and effective financial decisions crucial for personal financial well-being and broader economic stability. Financial literacy directly impacts people’s ability to manage their finances at the individual level. It enables them to make informed decisions regarding budgeting, saving, investing, and managing debt, which are essential for financial stability and security. Increased financial literacy helps individuals avoid excessive debt and bankruptcy, thereby promoting economic stability (Dzodzikova et al., 2022; Akimov, 2023). Financial literacy is also linked to better financial behaviors, such as higher savings rates and more prudent investment choices, contributing to personal wealth accumulation and financial security (Bunyamin & Wahab, 2022).

Entrepreneurship is a key driver of economic growth and innovation. Financial literacy plays a critical role in entrepreneurial success by enhancing the ability of entrepreneurs to access and manage financial resources effectively. Studies have shown that higher levels of financial literacy among entrepreneurs lead to better business performance and sustainability (Burchi et al., 2021; Li & Qian, 2020). Financially literate entrepreneurs are more capable of navigating financial markets, securing funding, and making strategic business decisions, which are vital for the growth and sustainability of their enterprises (Anshika & Singla, 2022).

At the macroeconomic level, financial literacy contributes to economic stability and growth. A financially literate population is better equipped to participate in the economy, leading to increased economic activity and growth. Financial literacy improves financial inclusion, allowing more people to access financial services and products and stimulating economic development (Zaimovic et al., 2023). Additionally, financial literacy helps mitigate economic crises by reducing the likelihood of widespread financial mismanagement and promoting more stable financial systems (Kiszl & Winkler, 2022).

The importance of financial literacy has led to numerous educational initiatives and policy measures aimed at improving financial knowledge and skills. Integrating financial education into school curricula is one effective approach to building financial literacy from a young age, which has been shown to have long-term benefits for economic development (Sabirin et al., 2023). Furthermore, targeted financial education programs for different demographic groups, such as women and young people, can help address specific financial literacy gaps and promote inclusive economic growth (Swiecka et al., 2020; Akimov, 2023).

Financial literacy significantly contributes to poverty reduction by enhancing individuals’ ability to make informed financial decisions and access financial services. Studies have shown that financial literacy alleviates relative household poverty through increased participation in entrepreneurial activities, commercial insurance, and better lending choices (Wang et al., 2022; Popli, 2023). Financial literacy also has immediate and long-term effects on poverty reduction in rural households by improving their economic status and financial education (Xu et al., 2023).

The relationship between financial literacy and income generation is well-documented. Financial literacy has been found to have a robust positive effect on household income, mediated by access to financial services (Twumasi et al., 2022). It also positively impacts the socioeconomic status of low-income households (Munisamy et al., 2022) and enhances the future income prospects of youth from low-income households through improved job-readiness and financial knowledge (Cedeño et al., 2021).

Financial literacy also plays a vital role in asset building by promoting financial inclusion and sustainable financial behaviors. Studies have found that financial literacy significantly improves access to various financial services, which is essential for asset building (Hasan et al., 2021; Rahayu et al., 2021). Furthermore, financial inclusion, driven by financial literacy, has been shown to reduce household budget deficits and poverty, particularly among women, thereby supporting asset building (Seng, 2021).

According to Faulkner (2021), the nations leading the world in financial literacy include Australia, Canada, Finland, Germany, Israel, the Netherlands, Sweden, and the United Kingdom. Rosenfeld (2022) also ranks Denmark, Norway, and Sweden at the top, each with a financial literacy rate of 71%. Canada and Israel are next at 68%, the United Kingdom at 67%, Germany and the Netherlands at 66%, Australia at 64%, and Finland at 63%.

Informal savings groups, such as village savings and loan associations, are crucial in promoting financial inclusion, especially among marginalized populations like rural women and low-income households. These groups have been identified as a potential pathway to financial inclusion in various contexts, including Nigeria, Zambia, and Uganda (Oranu et al., 2020; Bwalya & Zulu, 2021; Okuna et al., 2023).

The impact of savings groups on poverty reduction is well-documented. In Uganda, savings groups have been shown to significantly reduce poverty by providing access to financial services, creating employment opportunities, and improving household resources like education and health (Okuna et al., 2023). Similarly, participation in savings groups in Kenya and Peru has enabled households to save, borrow, and invest in small businesses, contributing to poverty alleviation (Muthike, 2020; Frisancho & Valdivia, 2020).

However, the relationship between savings groups and formal financial service usage presents a complex picture. While these groups bolster financial inclusion, they may not always translate into increased engagement with formal financial institutions, as observed in Peru (Frisancho & Valdivia, 2020).

Savings groups face challenges such as inadequate capital, corruption, and limited government support. Policymakers in Uganda and Nigeria have been urged to increase support for these groups through financial assistance, capacity building, improved supervision, and addressing challenges like limited income base and vulnerability to theft (Okuna et al., 2023; Oranu et al., 2020).

Robust financial management practices within savings groups, including record keeping, security of savings, budgeting, segregation of duties, and the availability of a functional constitution, are essential for their effective operation and the confidence of group members (Lagu, 2023). However, factors such as member default and the mismatch between the demand and supply of funds can hinder the sustainability of these groups (Abaho et al., 2022; Burlando et al., 2021).

While savings groups primarily serve as short-term cash-management vehicles rather than profit-generating entities, research suggests optimizing the cycle setup and lending policies can enhance their financial efficiency (Bossuyt et al., 2023). Additional challenges include low financial literacy among members, problems with group leadership, and the impact of external shocks like the COVID-19 pandemic (Murugiah, 2021; Okuna et al., 2023; Adegbite et al., 2022).

The Cambodia National Financial Inclusion Strategy (NFIS) 2019-2025, adopted on July 12, 2019, aims to increase access to and use of formal financial services, specifically focusing on reducing the financial exclusion of women by half (Khmer Times, 2021). This strategy draws on the 2017 Making Access Possible (MAP) Cambodia Country Diagnostic Report, which utilized extensive data, including surveys and interviews, to understand the state of financial inclusion in the country.

Currently, 59% of Cambodian adults utilize formal financial services, 12% rely solely on informal services, and a concerning 29% remain entirely excluded (Royal Government of Cambodia, 2019). This uptake of financial services is deeply intertwined with income levels. Farmers, representing a significant portion of the population, earn the lowest average monthly income and consequently have limited engagement with formal financial services. Conversely, formally employed individuals with higher incomes demonstrate the highest usage of these services. While financial inclusion rates are similar across genders, a slight advantage exists for females (73%) compared to males (69%).

Several key barriers hinder financial inclusion in Cambodia. Low financial literacy and limited financial awareness prevent effective engagement with and utilization of financial services. Additionally, the majority of the population (75%) earns less than KHR 1 million (US$ 246) per month, leaving limited disposable income to cover the costs associated with formal financial services (Royal Government of Cambodia, 2019).

The NFIS 2019-2025 outlines priority activities to achieve its goals. These include encouraging savings in formal institutions, promoting innovative credit products for SMEs, expanding payment system capabilities, enhancing access to insurance, strengthening financial sector regulatory capacity, and increasing consumer empowerment, protection, and financial transparency. These activities, informed by MAP analysis and tailored to address customer needs and barriers, are structured into short, medium, and long-term action plans. Effective implementation of these plans is crucial for bolstering the financial sector and the overall economy (Royal Government of Cambodia, 2019).

Several studies shed light on the determinants of financial literacy, particularly among rural populations. Socioeconomic and demographic characteristics such as gender, income, age, and education significantly impact financial literacy levels (Twumasi et al., 2022; Zhang & Xiong, 2020). Financial intermediaries, particularly microfinance institutions, have shown promise in enhancing both financial literacy and inclusion among low-income individuals in rural areas (Bongomin et al., 2020).

A study conducted in Cambodia and Vietnam found a positive correlation between higher educational levels, income, and improved financial literacy. Older individuals and those in stable occupations also exhibited higher levels of financial literacy (Morgan & Trinh, 2019). This study also revealed a strong link between financial literacy and positive financial behaviors, with financially literate individuals more likely to engage in savings and formal financial systems (Morgan & Trinh, 2019).

Innovative approaches to financial education, such as the use of technology, have shown promise in improving financial literacy in rural Cambodia. A study exploring the application of Action Design Research in developing a tablet application for financial education demonstrated that combining financial literacy with technology literacy can significantly enhance understanding and management of financial matters among rural populations. The project highlighted the importance of integrating information systems with traditional teaching methods to achieve more effective learning outcomes (Zaitsev & Mankinen, 2022).

Recent studies highlight the crucial role of financial literacy in Cambodia. Samreth et al. (2024) emphasize the importance of financial literacy in fostering financial inclusion and reducing reliance on high-interest informal finance. They suggest that financial education programs should focus on lower-income households, underscoring the positive correlation between general education, social capital, and financial literacy. They advocate for community-based interventions and integrate financial education with general education as effective strategies to enhance financial literacy. Additionally, Tes and Heng (2024) argue for the necessity of financial literacy education among Cambodian students, viewing it as a critical step toward developing financial management skills and facilitating informed financial decisions. They champion the cause of mandatory financial literacy education at all levels, highlighting its numerous benefits for individuals and the nation as a whole. Furthermore, Chet et al. (2023) explore the growing emphasis on financial literacy within the Cambodian education system, a trend supported by the National Bank of Cambodia and the Ministry of Education, Youth, and Sport. They investigate various factors influencing financial literacy, including economic conditions, family background, social networks, and media access, thereby shedding light on the complex nature of this essential skill.

While existing literature offers insights into financial literacy at a national level in Cambodia, research focusing specifically on the financial literacy of village savings group members is limited. Evaluating the awareness and practices of financial literacy (e.g., earning, saving, spending, borrowing, protection, and insurance) among these group members could yield valuable insights.

The literature also underscores challenges encountered by savings groups in other countries, such as inadequate capital, corruption, and limited government support. An investigation into the specific obstacles and challenges village savings groups face in Cambodia could inform policy interventions and support mechanisms to address these issues effectively.

By addressing these research gaps, this study could enhance the broader understanding of financial literacy, financial inclusion, and the role of savings groups in fostering sustainable financial behaviors and economic development in Cambodia.

METHODOLOGY

This study employed a quantitative research approach to assess the financial literacy awareness and practices among village savings group members in Cambodia. The study was conducted in the rural areas of Kampot and Kampong Thom provinces, known for their active village savings group activities. These two provinces are the project coverage areas of the NGO, which formed village savings groups in 27 villages in Kampot and 26 villages in Kampong Thom. Each village has one savings group with 12-20 members. The study covers 45 percent of the total villages with savings groups in the two provinces (13 villages in Kampot and 11 in Kampong Thom). Four to five respondents were selected randomly from each group, provided they agreed to be interviewed, as participation was voluntary. A total of 109 participants, mostly subsistence farmers, agreed to be respondents, with 55 participants from Kampot province and 54 from Kampong Thom province.

A survey questionnaire was developed and translated into the Khmer language to ensure effective communication with the respondents. The study administered the survey face-to-face.

The data collected from the survey were analyzed using Microsoft Excel and SPSS software. The analysis involved calculating frequency counts, sums, rankings, and percentages to provide a comprehensive understanding of the study participants’ financial literacy awareness and practices.

EMPIRICAL FINDINGS

Profile of Respondents

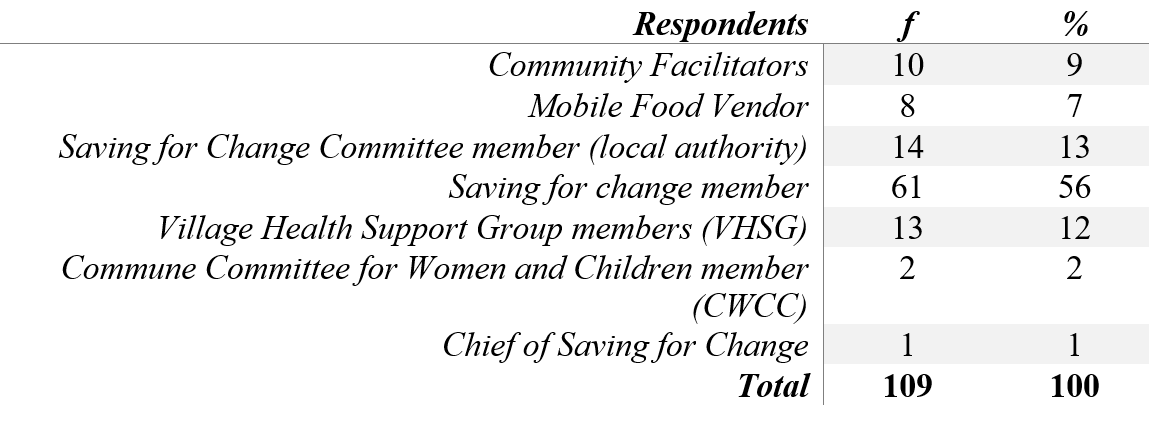

As shown in Table 1, the survey respondents were primarily members of the community’s Saving for Change (SfC) groups, with 56 percent being ordinary members and 25 percent being committee members and part of the Village Health Support Group. The remaining respondents were community facilitators and mobile food vendors who were also regular members of the SfC groups.

Table 1: Categories Respondents

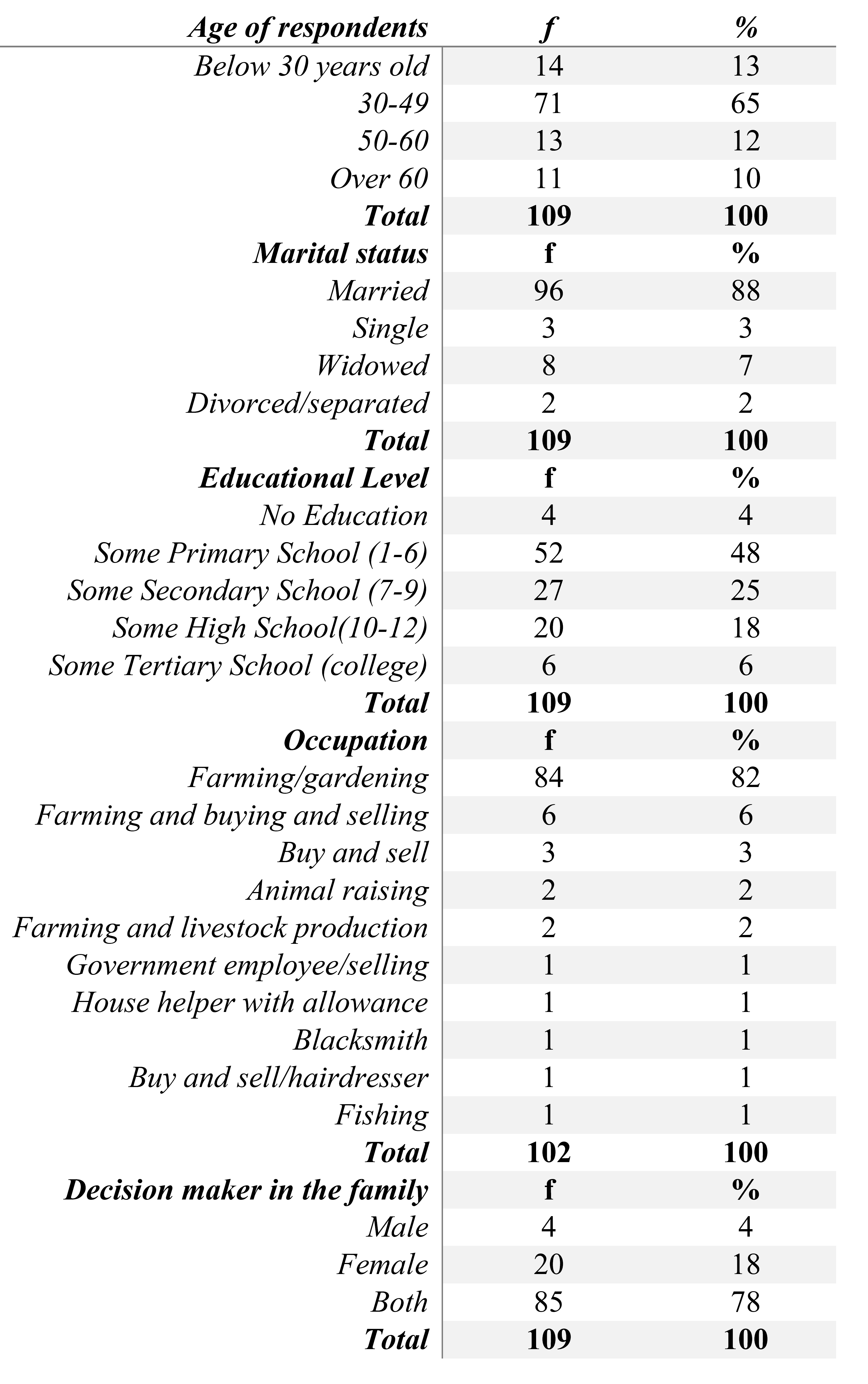

Table 2 shows that the majority of the respondents (65 percent) were between the ages of 30 and 50, and most (88 percent) were married. Farming was the primary occupation for 82 percent of the respondents, indicating that the SfC groups had a strong representation from the agricultural community.

The data also revealed interesting insights into the household decision-making dynamics within the respondents’ families. A significant percentage (78 percent) reported that both the husband and wife made decisions for the family, while 18 percent said that the females were the primary decision-makers in the households. This suggests a relatively collaborative decision-making process within the households, with women playing a significant role in financial and household decisions.

Table 2: Profile of Respondents

Earnings and Saving Practices of Respondents

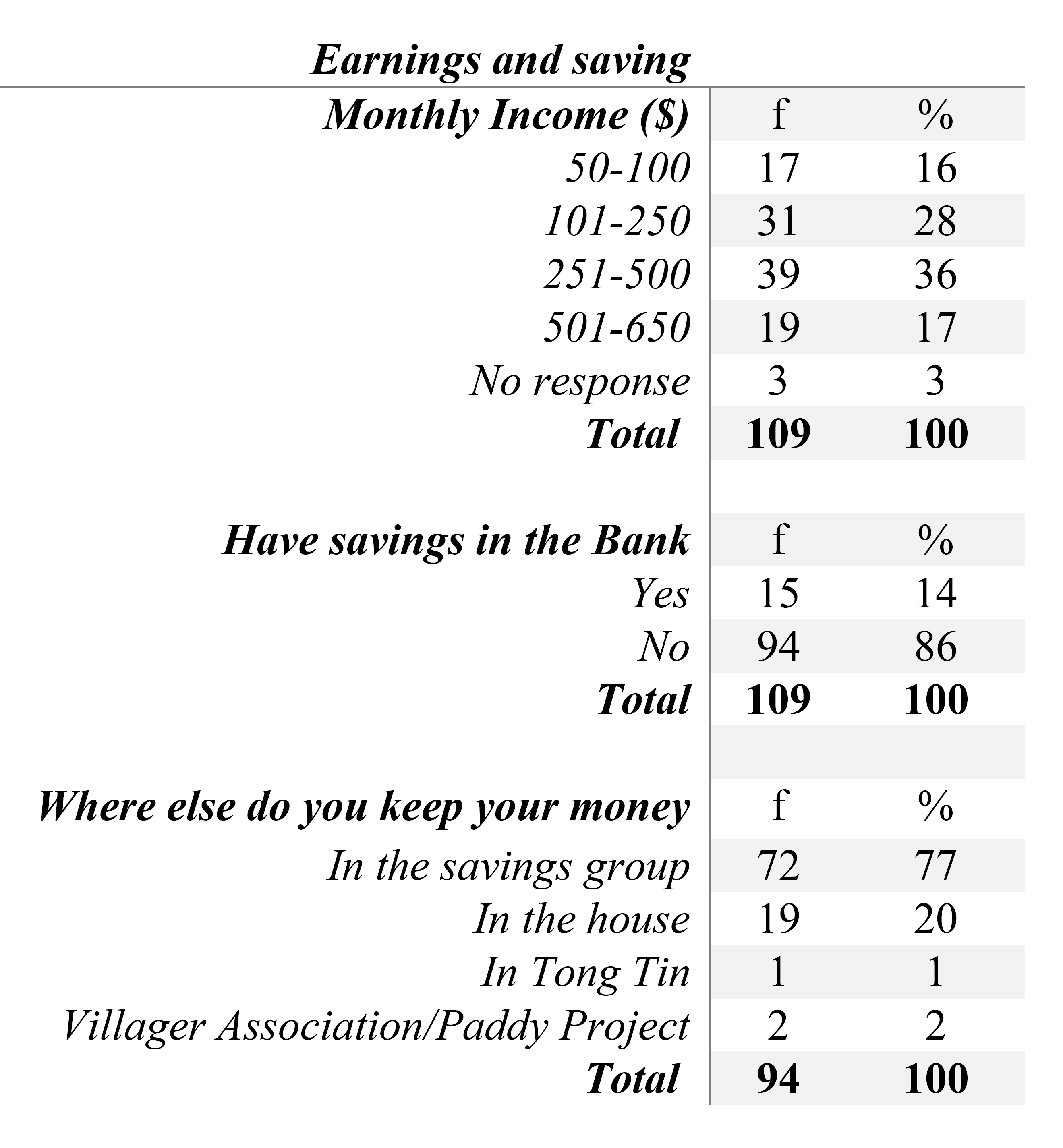

As Table 3 shows, the survey results revealed a diverse range of monthly incomes among the respondents. While 16 percent earned US$100 or less per month, a larger proportion (28 percent) earned between US$100 and US$250, and 36 percent earned up to US$500 monthly. This suggests that the SfC group members had varying levels of financial resources, with a significant number earning a modest monthly income.

However, despite these earnings, the majority of the respondents (86 percent) did not have any savings in the Bank. This indicates a potential lack of access or trust in formal financial institutions in this community. Instead, the majority (77 percent) of the respondents reported that they kept their savings within the SfC group, highlighting the importance of these informal savings mechanisms for the community.

The low proportion of respondents with formal bank savings (14 percent) suggests that financial inclusion and access to banking services may be challenging for this population. This finding underscores the need to understand the barriers and perceptions that prevent these individuals from utilizing formal financial services and to explore ways to enhance their financial resilience through alternative savings and investment opportunities.

Table 3: Earnings and Saving Practices

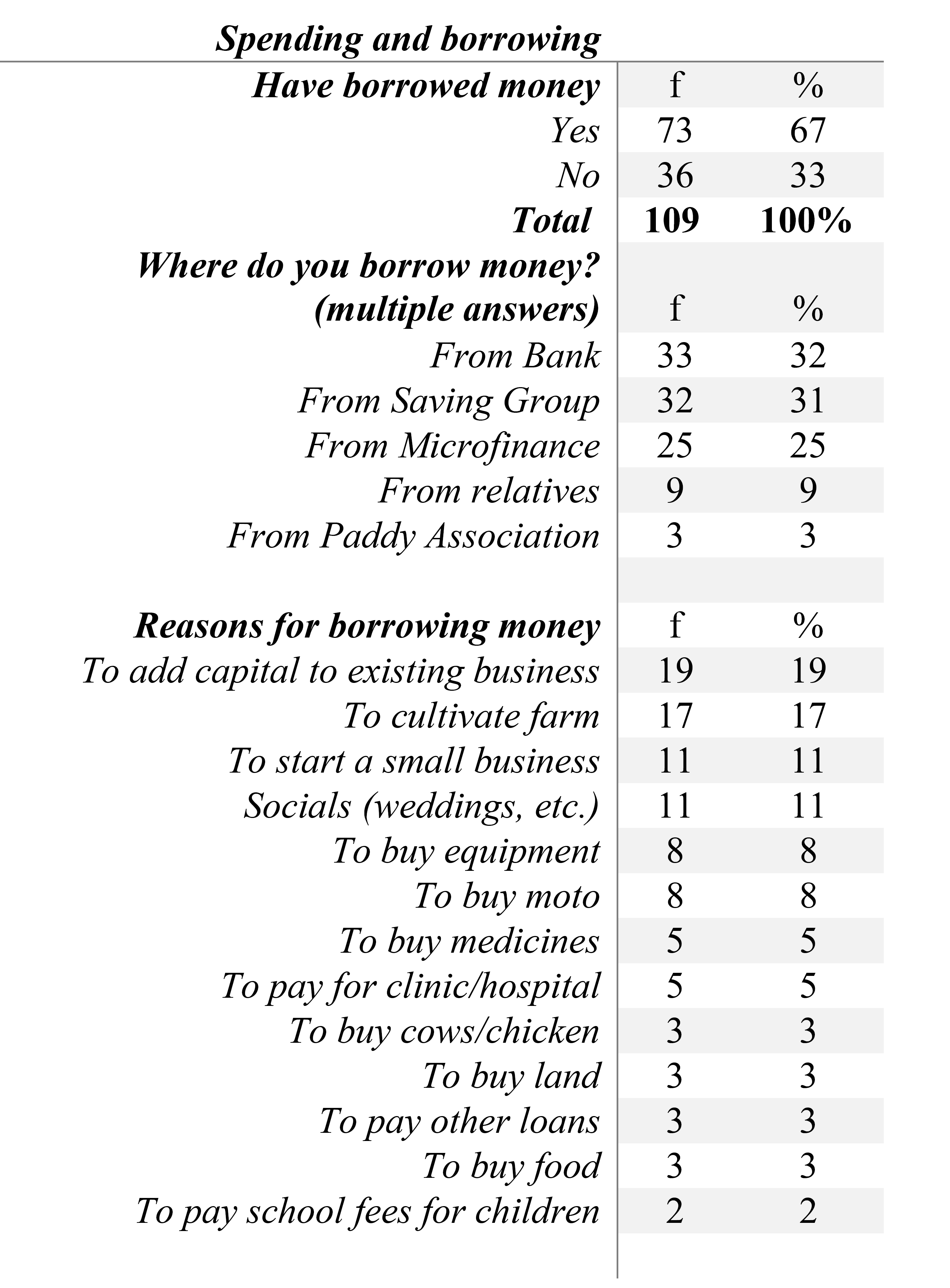

Spending and Borrowing Practices

As depicted in Table 4, the survey results also provided insights into the spending and borrowing practices of the SfC group members. A significant proportion (67 percent) of the respondents reported having borrowed money, with 32 percent borrowing from banks and 31% borrowing from the SfC savings group.

The primary reasons for borrowing included adding capital to their businesses (19 percent), starting a small business (11 percent), cultivating their farms (17 percent), and covering social expenses such as weddings (11 percent). These findings suggest that the respondents utilized borrowing to support their livelihoods, invest in entrepreneurial activities, and address economic and social obligations.

Table 4: Spending and Borrowing Practices

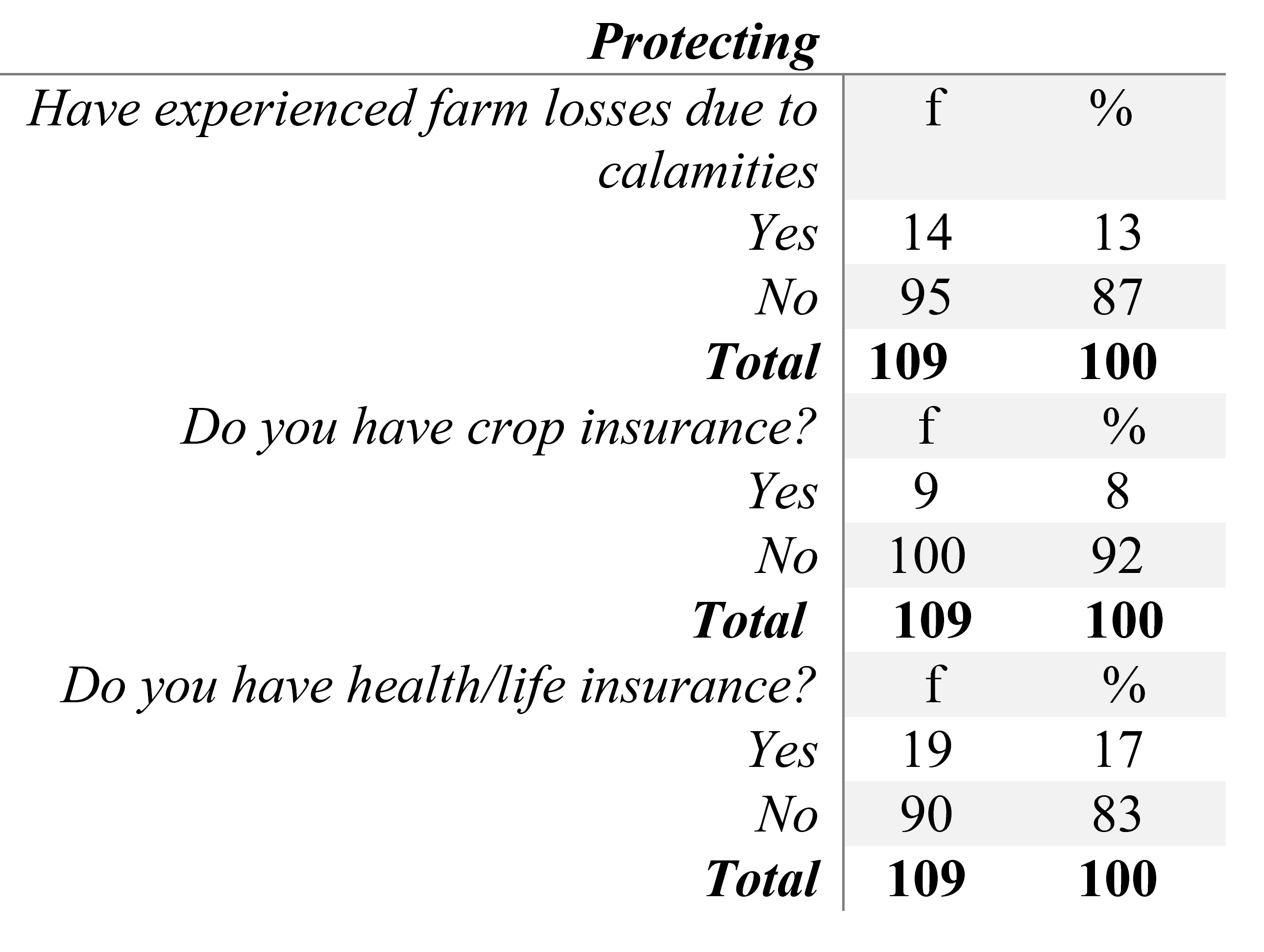

Protection and Insurance Coverage

Table 5 reveals that 13 percent of the respondents have experienced farm losses due to calamities. However, the survey showed that only 8 percent of the respondents have crop insurance coverage. Crop insurance is a critical risk management tool for farmers, providing financial protection against yield losses caused by various agricultural risks. The fact that most (92 percent) of respondents do not have crop insurance suggests a significant gap in access to and awareness of such insurance programs within this community.

Table 5 also shows that 17 percent of the respondents have some form of health or life insurance, while the remaining 83 percent do not. The relatively low rate of health and life insurance coverage among the respondents indicates room for improvement in increasing insurance penetration within this community.

Table 5: Access to Insurance Coverage for Protection

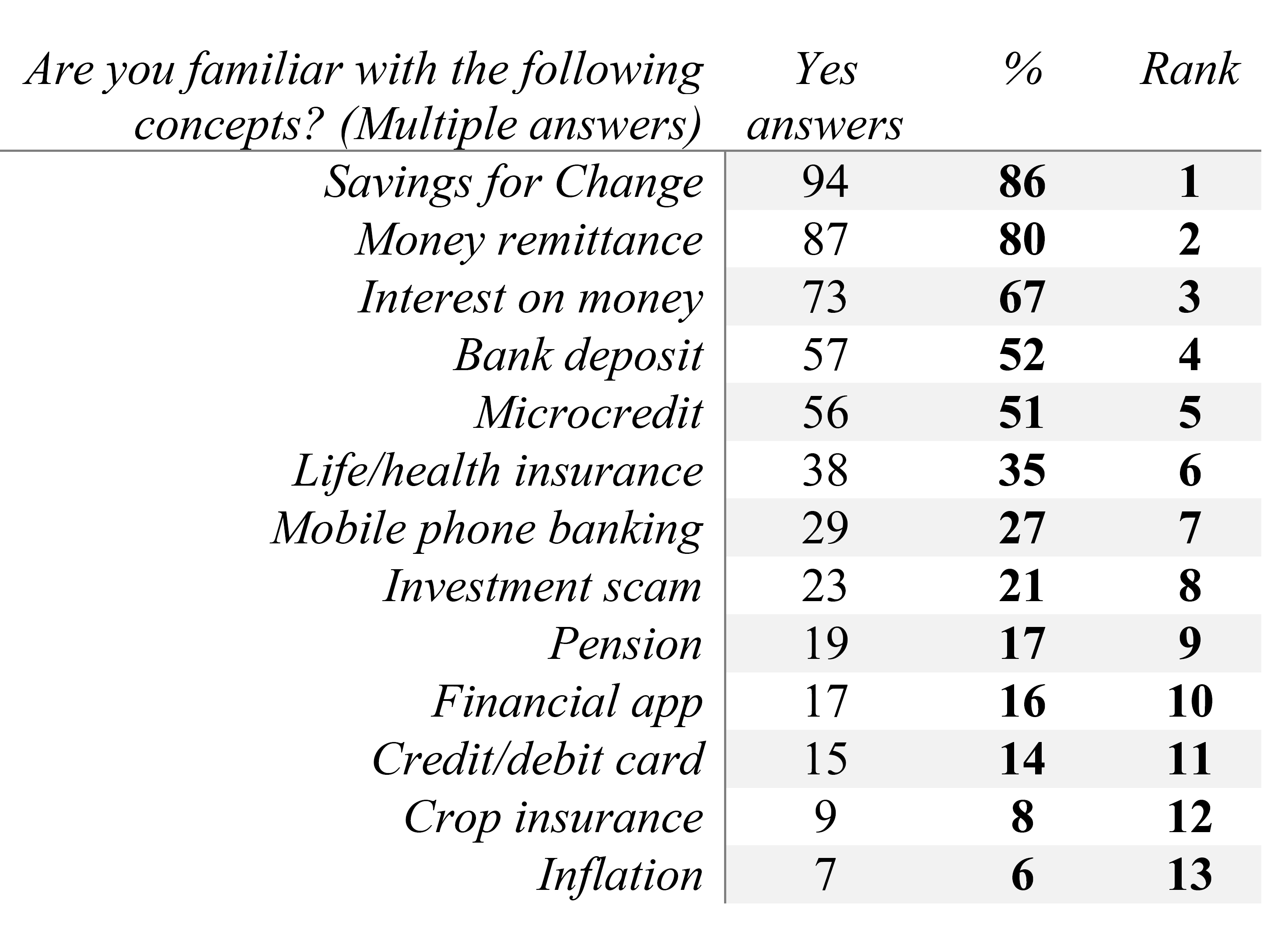

Financial Concepts Awareness and Use of Mobile Applications

The survey also explored the respondents’ familiarity with various financial concepts. As shown in Table 6, the majority of the respondents demonstrated a good understanding of concepts such as saving for change (86 percent), money remittance (80 percent), and interest on money (67 percent). This suggests that the SfC group members have a relatively strong grasp of fundamental financial principles.

Additionally, a notable proportion of respondents were familiar with more advanced concepts, such as bank deposits (52 percent) and microcredit (51 percent). This level of financial literacy indicates that the SfC group members have the potential to engage with a broader range of financial services and products, provided that the appropriate access and support mechanisms are available.

Table 6: Financial Concepts Awareness

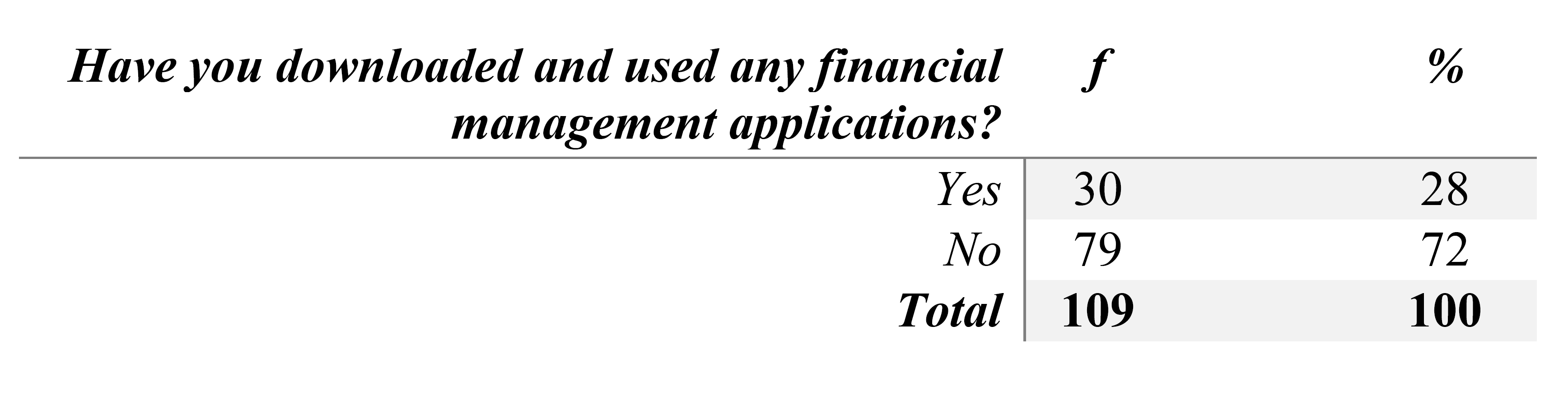

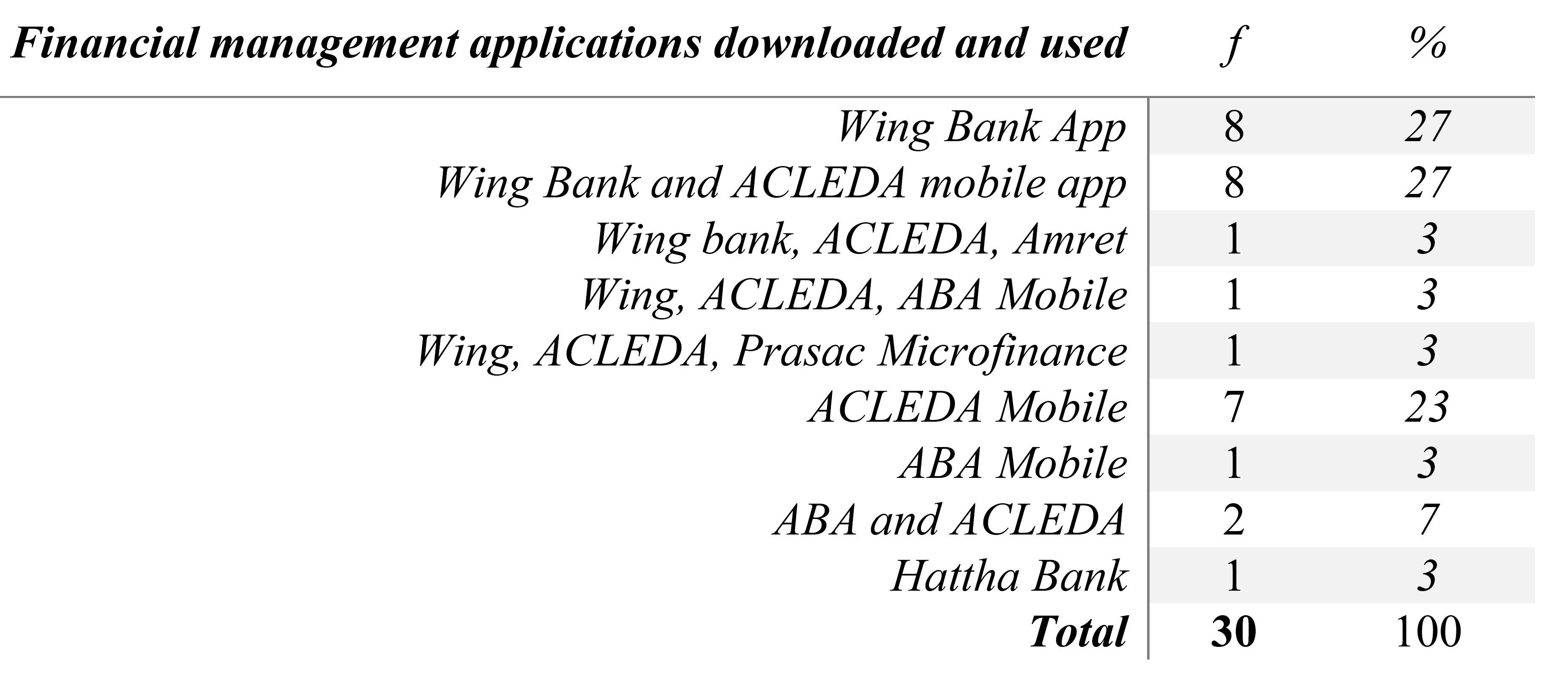

Table 7 shows that the utilization of mobile financial applications among the SfC group members was relatively low, with only 28 members have the potential to engage with a broader range of financial services and products, provided of the 109 respondents reporting that they had downloaded and used such apps. The most common financial apps used were the Wing Bank app and ACLEDA mobile app, and 13 respondents had downloaded and used two or more applications (see Table 8).

This limited adoption of mobile financial technologies suggests that barriers or challenges may prevent the SfC group members from fully leveraging the potential of these digital tools. Factors such as access to smartphones, digital literacy, and the relevance of the available mobile apps to the community’s specific needs could all influence the level of engagement with these financial technologies.

Table 7: Access to Financial Management Applications

Table 8: Financial App Used by the Respondents

Barriers to Accessing Bank Services

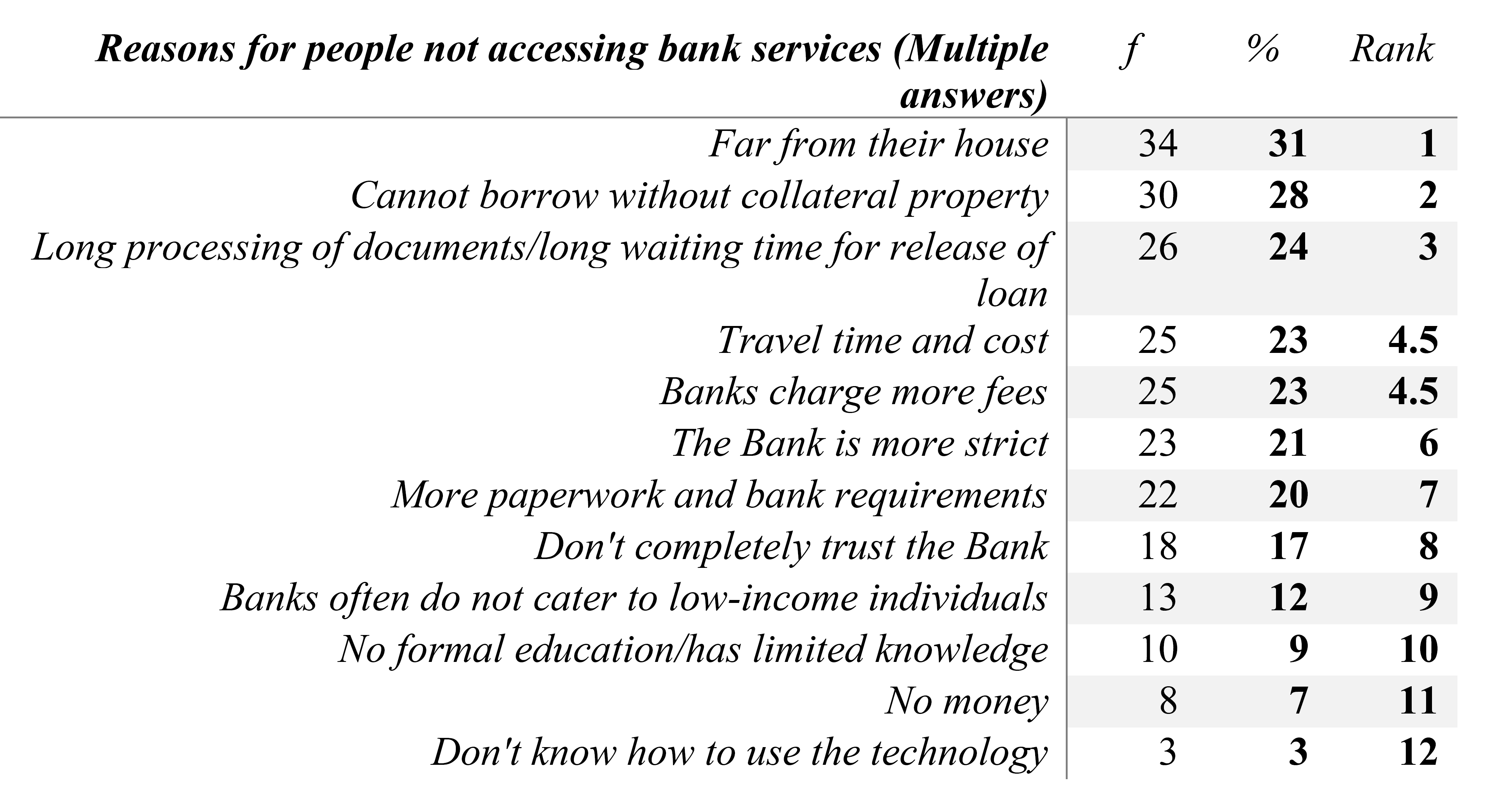

The respondents cited several key barriers when asked about their reasons for not accessing bank services (see Table 9). The most common reasons included distance, as 31 percent of respondents stated that their house was too far from the Bank, highlighting the geographical accessibility challenges this rural community faces. Additionally, 28 percent of respondents reported that they could not borrow from the Bank without collateral property, indicating a significant obstacle to accessing formal credit. The lengthy loan processing time, with 24 percent of respondents mentioning that they had to wait a considerable period before the loan was released, also deterred them from using bank services. Travel time and cost, cited by 23 percent of respondents, and high bank fees, mentioned by the same percentage, were further reasons that discouraged the SfC group members from utilizing formal financial institutions.

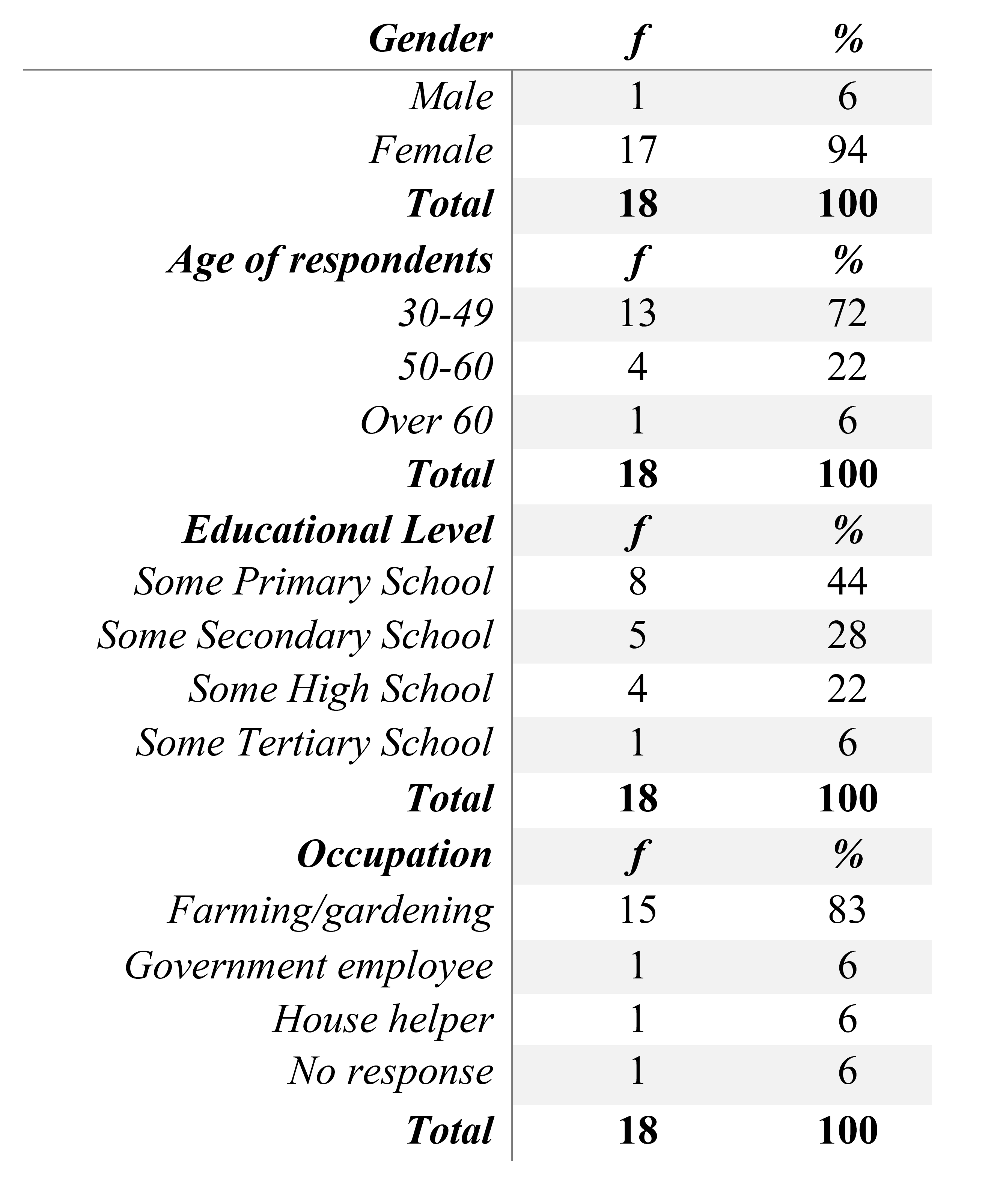

Furthermore, 17 percent of respondents expressed a lack of trust in the Bank, while 12 percent believed banks often do not cater to low-income individuals. Table 10 shows the demographics of those respondents who said “they do not completely trust the bank.” Most are females (94 percent), aged 30-49 (72 percent). Most of them have some primary school educational level (44 percent ), and most are engaged in farming and gardening (83 percent).

Table 9: Barriers to Accessing Bank Services

Table 10: Demographics of Respondents Who Say “They Do Not Completely Trust The Bank.”

Knowledge and Skills Respondents Want to Learn

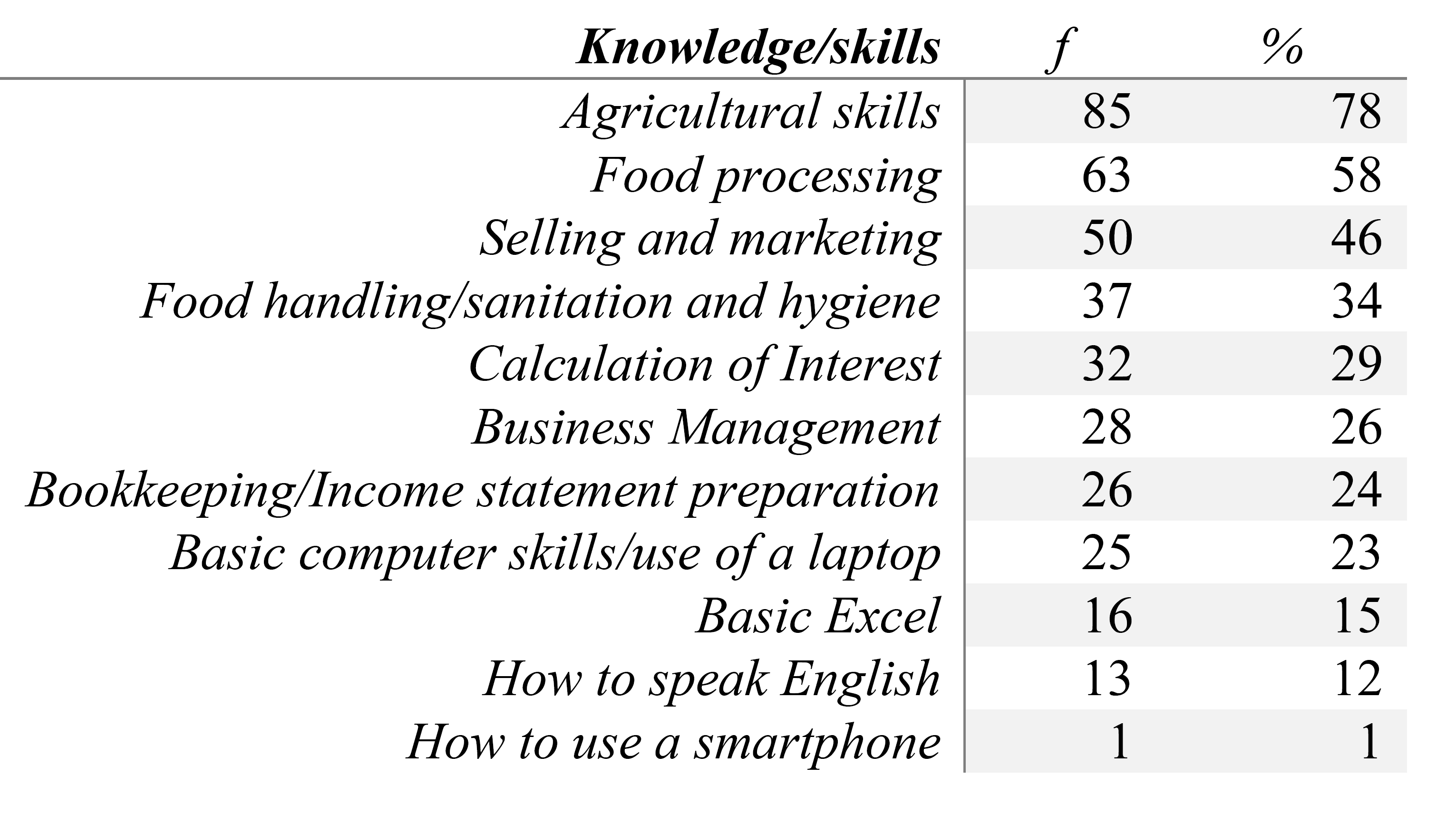

As shown in Table 11, most SfC group members were interested in acquiring knowledge and skills related to agriculture and food processing. This indicates a strong focus on enhancing their livelihood capabilities, particularly in areas closely connected to their primary occupations.

Table 11: Knowledge and Skills Respondents Want to Learn

DISCUSSION

The study highlights the crucial role of informal savings groups like SfC in advancing financial inclusion, especially for marginalized communities (Oranu et al., 2020; Bwalya & Zulu, 2021; Okuna et al., 2023). The reliance on SfC for savings and credit underscores their importance as alternative financial mechanisms. Barriers to accessing bank services—such as distance, collateral requirements, lengthy procedures, and lack of trust—reflect challenges noted in existing literature (Royal Government of Cambodia, 2019; Okuna et al., 2023; Oranu et al., 2020). This points to the urgent need for targeted interventions to improve the accessibility and affordability of formal financial services. Furthermore, the study shows that SfC members are keen to enhance their financial knowledge, particularly in agriculture and food processing. This result aligns with the literature’s call for context-specific financial education programs tailored to community needs (Samreth et al., 2024; Tes & Heng, 2024), highlighting the potential impact of integrating financial education with livelihood development initiatives. Moreover, the study supports broader literature that emphasizes the positive link between financial literacy and economic development outcomes such as poverty reduction, income generation, and asset building (Bunyamin & Wahab, 2022; Wang et al., 2022; Hasan et al., 2021).

Although the literature underscores the role of savings groups in facilitating formal financial inclusion, the study shows that SfC members had a low uptake of formal savings and limited use of mobile financial applications. This indicates that participation in savings groups may not necessarily lead to greater engagement in Cambodia’s formal financial institutions or digital financial tools. Additionally, the strong interest in agriculture and food processing knowledge among SfC members contrasts with the broader literature, which often focuses on general financial management skills. It underscores the importance of customizing financial education to meet the specific occupational needs of the target population.

The study offers valuable micro-level insights into the financial literacy, practices, and challenges of village savings group members in Cambodia, a demographic often overlooked in broader national surveys. By concentrating on this specific group, the research provides a detailed understanding of their financial behaviors and the obstacles they face. It highlights the specific barriers that hinder SfC members’ engagement with formal financial institutions and digital financial services, such as lack of trust, collateral requirements, and geographical distance. These context-specific challenges are essential for developing effective strategies to enhance financial inclusion.

CONCLUSION

“Financial inclusion is a strong enabler of addressing the country’s economic growth and reducing inequality,” according to the Credit Bureau Cambodia chairwoman and NBC governor Dr. Chea Serey, as reported by Phnom Penh Post. This statement underscores the national goal of improving financial literacy and inclusion through a more determined, multisectoral, and inclusive approach, reaching out to the underserved corners of the country.

The study’s findings provide valuable insights into the financial practices, literacy, and inclusion of the savings group members in the surveyed community. A key strength identified is the relatively strong financial literacy of the respondents, indicating the potential to further build upon this knowledge base and expand the financial capabilities of the savings group members.

However, the study also revealed significant barriers to financial inclusion and access to formal financial services. Factors such as geographical distance from banks, lack of collateral, lengthy loan processing, high costs, and perceived unfriendliness of banks were identified as major deterrents to the utilization of formal financial institutions. These findings align with existing literature on the challenges faced by marginalized communities in accessing formal financial services (Royal Government of Cambodia, 2019; Okuna et al., 2023; Oranu et al., 2020). This points to the urgent need for targeted interventions to improve the accessibility and affordability of formal financial services.

The study highlighted gaps in insurance coverage, particularly for agricultural and health risks, leaving the respondents vulnerable to financial shocks. Strengthening the availability and uptake of relevant insurance products could enhance the financial resilience of the savings group members. Furthermore, the limited use of mobile financial applications among the respondents also points to the need to address underlying challenges, such as digital literacy and the relevance of existing mobile solutions, to unlock the potential of digital financial services for this community.

The reliance on informal savings groups like SfC for savings and credit underscores their importance as alternative financial mechanisms, as noted in the existing literature (Oranu et al., 2020; Bwalya & Zulu, 2021; Okuna et al., 2023). However, the study shows that participation in savings groups may not necessarily lead to greater engagement with formal financial institutions or digital financial tools in Cambodia, which is an important nuance compared to the broader literature.

It is important to note that this study was conducted within a specific rural community, and the findings may not be fully generalizable to other contexts. Future research could explore the financial practices and inclusion of savings group members in different geographical regions or socioeconomic settings to gain a more comprehensive understanding of the financial landscape.

Moreover, further research could delve deeper into the root causes of the identified barriers, such as the underlying reasons for the lack of trust in formal financial institutions. This could inform the development of more targeted interventions and policy recommendations to address this population’s unique needs and challenges.

REFERENCES

Abaho, E., Mindra, R., Agasha, E., & Balunywa, A. (2022). Alternative business finance: Insights from selected informal savings groups in Uganda. African Journal of Economic and Management Studies, 13(2), 268-283. https://doi.org/10.1108/ajems-11-2021-0490

Adegbite, O., Anderson, L., Chidiac, S., Dirisu, O., Grzeslo, J., Hakspiel, J., … & de Hoop, T. (2022). Women’s groups and COVID-19: An evidence review on savings groups in Africa. Gates Open Research, 6. https://doi.org/10.12688/gatesopenres.13550.1

Akimov, A. (2023). Socioeconomic aspects of the development of financial literacy of the population. Scientific Library Publishing House. https://doi.org/10.36871/ek.up.p.r.2023.09.02.010

Anshika, A., & Singla, A. (2022). Financial literacy of entrepreneurs: A systematic review. Managerial Finance, 48(9/10), 1352-1371. https://doi.org/10.1108/mf-06-2021-0260

Baranova, A. A., Fridrih, M. M., & Sinyavskaya, E. E. (2024). Financial literacy. INFRA-M. https://doi.org/10.12737/1865717

Bossuyt, E., D’Espallier, B., & Mersland, R. (2023). Profit-generating entities or cash-management vehicles? Unpacking the financial performance of savings groups worldwide. Journal of Alternative Finance, 1(1), 3-23. https://doi.org/10.1177/27533743231201771

Bunyamin, M., & Wahab, N. A. (2022). The impact of financial literacy on finance and economy: A literature review. Labuan Bulletin of International Business and Finance (LBIBF), 20(2), 49-65. https://doi.org/10.51200/lbibf.v20i2.3677

Burchi, A., Włodarczyk, B., Szturo, M., & Martelli, D. (2021). The effects of financial literacy on sustainable entrepreneurship. Sustainability, 13(9), 5070. https://doi.org/10.3390/SU13095070

Burlando, A., Canidio, A., & Selby, R. (2021). The economics of savings groups. International Economic Review, 62(4), 1569-1598. https://doi.org/10.1111/IERE.12526

Bwalya, R., & Zulu, M. (2021). The role of savings group on the nutritional and economic wellbeing of rural households: The case of World Vision’s savings for transformation (S4T) in Zambia. Business and Economic Research, 11(2), 44-61. https://doi.org/10.5296/BER.V11I2.18451

Cedeño, D., Lannin, D. G., Russell, L., Yazedjian, A., Kanter, J. B., & Mimnaugh, S. (2021). The effectiveness of a financial literacy and job-readiness curriculum for youth from low-income households. Citizenship, Social and Economics Education, 20(3), 197-215. https://doi.org/10.1177/20471734211051770

Chet, C., Khim, C., Khem, S., Seang, L., & Sok, S. (2023). Teachers’ perspective on how financial literacy benefits primary students in Cambodia?. Cambodia Journal of Basic and Applied Research, 5(2), 4-8.

Dzodzikova, F., Hayrapetyan, A., Kumalagova, E., & Faladyan, A. (2022). The essence of financial literacy and its role in economic development. Scientific Library Publishing House. https://doi.org/10.36871/ek.up.p.r.2022.11.03.017

Faulkner, A. (2021). Financial literacy around the world: What we can learn from the national strategies and contexts of the top ten most financially literate nations. The Reference Librarian, 63(1–2), 1–28. https://doi.org/10.1080/02763877.2021.2009955

Frisancho, V., & Valdivia, M. (2020). Savings groups, risk coping, and financial inclusion in rural areas. https://doi.org/10.18235/0002910

Gadzhiev, N. N., Konovalenko, S. S., Skripkina, O. O., Murzak, N. N., Vavilkina, N. N., Gavrilova, T., Knyazeva, O. O., Ahmedova, H. H., Kiseleva, O. O., & Gusev, V. (2024). Fundamentals of financial literacy. INFRA-M. https://doi.org/10.12737/1859083

Hasan, M., Le, T., & Hoque, A. (2021). How does financial literacy impact on inclusive finance?. Financial Innovation, 7(1), 40. https://doi.org/10.1186/s40854-021-00259-9

Khmer Times. (2021, December 3). Financial inclusion instrumental in addressing country’s economic growth, says NBC. Khmer Times. https://www.khmertimeskh.com/50981729/financial-inclusion-instrumental-in-addressing-countrys-economic-growth-says-nbc/

Kiszl, P., & Winkler, B. (2022). Libraries and financial literacy. Reference Services Review, 50(3/4), 356-376. https://doi.org/10.1108/rsr-01-2022-0005

Klapper, L., Lusardi, A., & Oudheusden, P. V. (n.d.). Financial literacy around the world: Insights from the Standard & Poor’s Ratings Services Global Financial Literacy Survey. https://gflec.org/wp-content/uploads/2015/11/3313-Finlit_Report_FINAL-5.11.16.pdf

Lagu, Y. (2023). Financial management of village savings and loans associations in West Nile, Uganda. Financial Management, 9(1). https://doi.org/10.21522/tijmg.2015.09.01.art007

Li, R., & Qian, Y. (2020). Entrepreneurial participation and performance: The role of financial literacy. Management Decision, 58(3), 583-599. https://doi.org/10.1108/md-11-2018-1283

Morgan, P. J., & Trinh, L. Q. (2019). Determinants and impacts of financial literacy in Cambodia and Viet Nam. Journal of Risk and Financial Management, 12(1), 19. https://doi.org/10.3390/JRFM12010019

Munisamy, A., Sahid, S., & Hussin, M. (2022). Socioeconomic sustainability for low-income households: The mediating role of financial well-being. Sustainability, 14(15), 9752. https://doi.org/10.3390/su14159752

Murugiah, L. (2021). Saving management in Malaysia. Studies of Applied Economics, 39(10). https://doi.org/10.25115/eea.v39i10.5360

Muthike, E. L. M. (2020). The impact of households’ participation in informal saving towards poverty reduction: Case study of saving internal leading communities within the household level in Naivasha Sub County, Kenya. The International Journal of Humanities & Social Studies, 8(9). https://doi.org/10.24940/theijhss/2020/v8/i9/HS2009-048

Okello Candiya Bongomin, G., Mpeera Ntayi, J., & Akol Malinga, C. (2020). Analyzing the relationship between financial literacy and financial inclusion by microfinance banks in developing countries: Social network theoretical approach. International Journal of Sociology and Social Policy, 40(11/12), 1257-1277. https://doi.org/10.1108/ijssp-12-2019-0262

Okello Candiya Bongomin, G., Munene, J. C., & Yourougou, P. (2020). Examining the role of financial intermediaries in promoting financial literacy and financial inclusion among the poor in developing countries: Lessons from rural Uganda. Cogent Economics & Finance, 8(1), 1761274. https://doi.org/10.1080/23322039.2020.1761274

Okuna, V., Acanga, A., & Mwesigwa, D. (2023). The role of community saving initiatives in poverty reduction: An appraisal of saving groups in Alebtong District, Mid-North Uganda. International Journal of Poverty and Development, 5(3), 45-60. https://doi.org/10.47941/ijpid.1341

Oranu, C. O., Onah, O. G., & Nkhonjera, E. (2020). Informal saving group: A pathway to financial inclusion among rural women in Nigeria. Asian Journal of Agricultural Extension, Economics & Sociology, 38(12), 22-30. https://doi.org/10.9734/AJAEES/2020/V38I1230484.

Popli, N. (2023). Impact of financial literacy on rural economy. International Journal of Social Science & Economic Research, 8(7), 1872-1876. https://doi.org/10.46609/ijsser.2023.v08i07.015

Rahayu, A., Hasanah, L., & Pratiwi, L. (2021). Rahayu, A. S., Hasanah, L. A. N., & Pratiwi, L. S. (2021). The role of financial literacy in reducing poverty: Experience from Indonesia. Dinamika Ekonomi, 12(2), 133-141. https://doi.org/10.29313/DE.V12I2.7796

Rosenfeld, J. (2022, April 20). Financial literacy around the world: Top 10 countries and the US. GOBankingRates. https://www.gobankingrates.com/money/financial-literacy-around-the-world-top-10-countries-and-united-states/?utm_campaign=1162292&utm_source=yahoo.com&utm_content=5&utm_medium=rss

Royal Government of Cambodia. (2019). National financial inclusion strategy 2019-2025. https://www.nbc.gov.kh/download_files/publication/blueprints_eng/Final_NFIS_in_English.pdf

Sabirin, S., Benius, B., Neneng, S., Nurwati, S., & Hendrayati, S. L. (2023). The importance of early financial literacy management skills: Challenges and opportunities for economic development. International Journal of Business, Economics and Management, 6(2), 105-111. https://doi.org/10.21744/ijbem.v6n2.2120

Samreth, S., Aiba, D., & Phal, V. (2024). Financial literacy among microfinance borrowers: Its importance and determinants from a household survey in Cambodia (JICA Ogata Research Institute Discussion Paper No.17). JICA Ogata Research Institute for Peace and Development.

Seng, K. (2021). The poverty-reducing effects of financial inclusion: Evidence from Cambodia. In Financial inclusion in Asia and beyond (pp. 197-226). Routledge. https://doi.org/10.4324/9781003035916-7

Swiecka, B., Yeşildağ, E., Özen, E., & Grima, S. (2020). Financial literacy: The case of Poland. Sustainability, 12(2), 700. https://doi.org/10.20944/preprints201912.0305.v1

Tes, V., & Heng, K. (2024). Financial literacy education: What it is and how it is needed for Cambodian students. Cambodian Journal of Educational Research, 4(1), 57-83.

Twumasi, M. A., Jiang, Y., Ding, Z., Wang, P., & Abgenyo, W. (2022). The mediating role of access to financial services in the effect of financial literacy on household income: The case of rural Ghana. Sage Open, 12(1), 21582440221079921. https://doi.org/10.1177/21582440221079921

Wang, S., Cao, P., & Huang, S. (2022). Household financial literacy and relative poverty: An analysis of the psychology of poverty and market participation. Frontiers in psychology, 13, 898486. https://doi.org/10.3389/fpsyg.2022.898486

Xu, S., Yang, Z., Tong, Z., & Li, Y. (2023). Knowledge changes fate: Can financial literacy advance poverty reduction in rural households?. The Singapore Economic Review, 68(04), 1147-1182. https://doi.org/10.1142/s0217590821440057

Zaimovic, A., Torlakovic, A., Arnaut-Berilo, A., Zaimovic, T., Dedovic, L., & Nuhic Meskovic, M. (2023). Mapping financial literacy: A systematic literature review of determinants and recent trends. Sustainability, 15(12), 9358. https://doi.org/10.3390/su15129358

Zaitsev, A., & Mankinen, S. (2022). Designing financial education applications for development: Applying action design research in Cambodian countryside. European Journal of Information Systems, 31(1), 91-111. https://doi.org/10.1080/0960085X.2021.1978341

ZHang, H., & Xiong, X. (2020). Is financial education an effective means to improve financial literacy? Evidence from rural China. Agricultural Finance Review, 80(3), 305-320. https://doi.org/10.1108/afr-03-2019-0027