Print ISSN : 2708-616X | Online ISSN : 2708-6178 | Title DOI: https://doi.org/10.62458/160224

Volume 9 | Number 2 | July – December 2024 | DOI: https://doi.org/10.62458/jafess922

Received : July 2024 | Revised: September 2024 | Accepted: December 2024

Rido Thath, Ph.D.

CamEd Business School

Email: [email protected]

ABSTRACT

Purpose: This study examines the determinants of tax revenue in Southeast Asia, focusing on the impact of human development and government effectiveness on tax revenue.

Methodology: The panel data method, specifically the fixed effects and random effects models, was employed to examine the determinants of tax revenue. The study used data (1992 to 2022) from eight Southeast Asian countries retrieved from the World Bank’s World Development Indicators and the International Monetary Fund online database.

Findings: This study reveals a positive relationship between human development and tax revenue and government effectiveness and tax revenue.

Implications: The results of this study carry important implications for policymakers. They suggest that enhancing government effectiveness and human development, which encompasses income, health, and education, can lead to an increase in tax revenue. Policymakers are therefore encouraged to prioritize the implementation of policies that bolster government effectiveness, such as the use of modern technology in tax administration, and economic policies that not only boost income but also improve health and education outcomes.

Originality: This study contributes to the existing literature by providing evidence on the relationship between tax revenue and key policy variables. Moreover, it has tested data sets and variables that differ from those used in previous panel data analyses.

Limitations and directions for future research: This study provides valuable evidence on various factors that affect tax revenue. However, based on data availability, other policy variables, such as the quality of tax administration, tax exemption, and incentives, should be included to explore their impact on tax revenue.

Keywords: Tax revenue; Human Development; Government effectiveness; Southeast Asia

Introduction

Tax revenue is one of the major sources of government budgets in most countries, except for several resource-rich economies that can generate revenue from natural resources for financing public expenditure (Devarajan & Do, 2023). The government needs budgets to supply various services, including financing essential investments in education, health, and physical infrastructure to promote economic growth and sustainable development to improve the welfare of citizens. The size of the budget needed differs from government to government grounded on their policy priorities, ideologies, and social structure, such as the change in the demographic composition, and based on external factors such as the international trade regimes and geopolitics, and the incidence of the outbreak of pandemics such as the COVID-19, which generally pressure the government to increase public expenditure (Crowe et al., 2022; Dougherty et al., 2022; Fu & Chang, 2021). In a more social-oriented leftist government, more considerable tax revenue is needed as the government desires to provide most of the public services to the people, while in a more liberal government, a lower budget is required to provide public services as the government tends to be smaller and most services are provided by the market or private sectors and the responsibility of the individual (Högström & Lidén, 2023). Regarding the demographic composition, the more aging the society is, the higher the budget the government needs, while the revenue from taxation is lower due to the decreasing working-age population (Crowe et al., 2022; Dougherty et al., 2022).

The issue of taxation is complex and multifaceted, and it depends on the development stage of the economy. Developing economies tend to mobilize lower tax revenue as they depend more on small-scale and subsistence farming, making it difficult for the government to impose a tax, and the informal sector, most of which are not taxable, accounts for a sizeable share of the economic pie. These factors render lower tax revenue in many developing economies. According to Besley & Persson (2014), in low-income economies, tax revenue generally comes from 10 to 20 percent of the GDP, while high-income countries can collect as much as 40 percent of the GDP. The causes of the relatively low tax revenue in developing countries vis a vis their developed counterparts go beyond economic reasons; political, sociological, and cultural factors also influence the effort of tax collection; developing countries, for instance, have weaker institutions and their policies are less transparent, and corruption is rampant, rendering the leakage of the already small tax revenue (Ajaz & Ahmad, 2010; Besley & Persson, 2014). However, developing countries need larger budgets for financing necessary investments, such as the infrastructure investment that is one of the main drivers of economic growth and development (Wang, 2002); since the infrastructure is generally not well-developed in many developing countries, its investment was found to have a relatively more significant impact than the same magnitude of investment in developed countries (Han et al., 2021).

As adequate tax revenue cannot be mobilized to deliver public services, finance the infrastructure, and other investments for development purposes, developing countries are pressured to explore ways to increase tax revenue as well as other alternative sources of revenue, probably the non-tax revenue, which is defined as all forms of government revenue except for taxation. It includes user charges, fees, fines, and revenue from government capital and funds. In broader terms, non-tax revenue includes sovereign debt (Deng & Smyth, 2000). Non-tax revenue is one of the most important sources of revenue in developing countries. However, the non-tax revenue generated from resource extraction was found to be anti-democratic (Prichard et al., 2018), which is also anti-growth, as democracy was found to have a positive relationship with economic growth (Acemoglu et al., 2019; Barro, 1996). Otherwise, the only available option is to reduce public expenditure and scale down public services, which will negatively affect the welfare of the people and cause negative repercussions on the popularity and stability of the government. Thus, taxation must be examined thoroughly, given its critical role in maintaining economic stability and sustainability. Understanding the factors influencing tax revenue is essential for governments seeking to improve revenue without stirring public discontent or adverse repercussions.

The economy of Southeast Asia has grown rapidly, and after the COVID-19 pandemic, the International Monetary Fund (IMF) expects the region to be the fastest-growing in the world (Menon, 2023). The majority of the countries in the region, once among the poorest of the poor, have experienced rapid economic growth and social and structural transformation. Poverty has significantly reduced, and the most underdeveloped countries in the region have successfully graduated from a low-income to at least a lower-middle income status. As development proceeds, the pressure on each country to increase tax revenue is mounting. Along with growing income, people tend to demand more and better-quality public services, and problems regarding the demographic transformation, such as aging and decreasing working-age population, emerge, which further depress the government revenue. This development indicates that knowledge of taxation and its determinants is important; however, previous studies exploring the determinants of tax revenue in Southeast Asia are limited. Only a few studies, such as studies by Anh and Thinh (2018), Minh Ha et al. (2022), and Saptono and Mahmud (2021), were relevant to the context of Southeast Asia. Thus, the current study seeks to enhance the understanding of taxation by investigating the factors influencing tax revenue in Southeast Asia. Specifically, we examine the relationship between tax revenue, the Human Development Index (HDI), and government effectiveness. Unlike previous studies, this study uses a more extended period and more recent data to estimate the determinants of tax revenues, and the results shed more light and contribute to the body of the literature on determinants of tax revenue.

Following the introduction, the next section reviews the determinants of tax revenue in general and specifically in Southeast Asia. Subsequently, the methodology, data sources, data analysis, and discussion are presented, and finally, the study concludes with policy implications.

Literature review

The Determinants of Tax Revenue

The literature on the determinants of tax revenue is rich. It shows that tax revenue issues are complex and multi-faceted. Various factors, including economic, political, institutional, socio-cultural, external, legal, and business cycles, were found to affect the level of tax revenue.

The economy’s structure determines the tax revenue level that the government collects. Economies with a larger share of value-added to the manufacturing sector can collect higher tax revenue as it is less complicated to collect tax from manufacturing firms than from small-scale farming households. Thus, if the value-added of the agriculture, fishing, and forestry sector accounts for a larger share of the national income, which is a typical characteristic of many developing countries, tax revenue is likely to be smaller. In addition, economies with a high ratio of the informal sector, which is also a typical characteristic of many developing countries, can collect lower tax revenue as it is difficult to tax the informal sector. This is one of the factors contributing to lower tax revenue in developing countries (Tanzi & Zee, 2001).

The main objective of taxation is to mobilize revenue to finance public services (Burgess & Stern, 1993). However, the government may use its authority to collect tax for political purposes rather than raising revenue for public expenditure, such as financing income redistribution programs or providing incentives to specific industries or firms that are considered strategically important for the economy (Avi-Yonah, 2006; Gwartney & Lawson, 2006; Hemels, 2017). For political reasons, the government may even forgo tax revenue to promote a strategic industry. Related to political factors, the quality of public institutions also plays a vital role in tax administration. In the study in Sub-Saharan Africa, Tagem and Morrissey (2023) found that institution variables, including the level of corruption, equitable distribution of resources, accountability, and democracy, were among the most critical determinants of variation of tax capacity in different countries. In addition to institutional factors, culture is found to influence taxation. Culture is context-based; thus, it works differently in different economies. Social stigmatization, an example of a specific case of culture, is perceived differently in the US and Germany. In the case of tax evasion, social stigmatization, i.e., announcing a taxpayer’s activities in the media, for instance, works better in the US than in Germany (Ermasova et al., 2021). It was found that culture can influence the morality of taxpayers, and tax morale affects the compliance and evasion of taxes (Alasfour et al., 2016; Torgler, 2002).

Besides economic, political, and institutional factors, tax laws and regulations determine what and who to be taxed, thus also affecting tax revenue. An economy with a broad tax base can raise more taxes at lower administrative costs than those with a narrow tax base. In the case of sales and individual income tax in the US, the variation of tax revenue is associated with how the tax base is composed (Kwak, 2013).

In addition, tax revenue is generally associated with the business cycle, in the Spanish case, during the economic boom, the government can collect higher revenue, while a recession would see government revenue declining (Durán‐Cabré et al., 2020). These periods of boom and bust are linked to external or global factors. For example, during a global pandemic such as COVID-19, most economic activities have slowed down or stopped, many firms could not generate profit, cross-border trades were restricted, and government tax revenues declined (Stone & Saxena, 2020). Foreign aid or Official Development Assistance (ODA) is another external factor. The amount of aid varies depending on the economic condition of donor countries and their relationship with recipient countries. ODA is disbursed through grants, concessional loans, and technical assistance. Grants, for example, were found to have a negative relationship with tax revenue (Benedek et al., 2014; Thornton, 2014) because the government that relies on grants tends to make less effort to collect tax. Tax is not popular among the citizens; the government that increases tax rates and tax bases tends to be less popular with their voters and has to be more transparent and accountable to taxpayers; thus, if grants are available, the government will try not to increase tax revenue. Unlike grants, concessional loans, regardless of the concession level, were found to have a positive relationship with tax revenue (Thornton, 2014). As the government must pay back the loan, they will likely make more effort to collect tax to repay the loan, such as trying to improve the business environment so that firms will be more profitable and able to pay more taxes or to improve the capacity of tax administrators, and thus enhance the efficiency of tax collection and increase the volume of tax revenue collected. Similarly, external debt stock was found to have a positive relationship with tax revenue. As debts increase, the government is pressured to reduce them; thus, the government may become more prudent in taking more loans by considering only loan that has larger benefits or positive internal rate of returns or may find ways to improve tax revenue collection as well as reduce leakage from tax administration. The latter is linked to government effectiveness, one of the variables used to measure the quality of governance. Although a study in the context of Southeast Asia by Syadullah (2015) found an inconclusive effect of government effectiveness, it was expected to have a positive correlation with tax revenue; improved effectiveness will increase government revenue in various ways such as efficient collection of revenue or reducing leakage.

Other critical external factors besides ODA are Foreign Direct Investment (FDI) and Trade. FDI was found to have increased tax revenue (Camara, 2023); the channels through which FDI increases tax revenue are job creation, the increased productivity of workforces, and corporate and indirect taxes. Trade is the sum of imports and exports and has a significant relationship with tax revenue. However, the direction of the impact differs. If trade is associated with liberalization, reducing tariffs, and other trade barriers, the government may lose the sources of revenue that they once had collected from imposing tariffs (Asghar & Mehmood, 2017; Gropp et al., 1999; Karimi et al., 2016). Thus, the relationship is negative. Nonetheless, if trade enables the country to benefit from economies of scale and comparative advantage, the standard gain from trade argument, the tax revenue will likely increase. That means if trade improves economic activities, the government can increase tax revenue from various taxes such as income, salary, and profit taxes.

Inflation, although unfavorable, was found to have a positive relationship with tax revenue because when the general price level is rising, the tax bracket will be widened, which means that more people will be included in the tax bracket; for instance, their income would reach a certain level that requires them to pay taxes. Thus, the government will be able to mobilize increasing tax revenue. However, depending on the magnitude of inflation, too high inflation may cause severe economic consequences, particularly when investors are uncertain about their future investment and people’s livelihoods are eroded due to the rising cost of living (Prezas, 1991). Consequently, investors may choose to decrease their investments, while consumers may decide to reduce their consumption. This reduction in investment and consumption could lead to a decline in government tax revenue, and in the most severe situation, it could trigger an economic crisis.

Finally, the stage of economic development also influences tax revenue. Generally, the more developed the economy, the higher tax revenue the government can mobilize. One of the widely used indicators of development, the Human Development Index (HDI) was found to have a positive relationship with tax revenues (Ibadin & Oluwatuyi, 2021). There are different channels through which HDI can positively affect tax revenue. As HDI is a composite index of education, health, and income, its effect on tax revenue will be through these three development outcomes. Separately, when people are educated, they are more likely to comply with tax payments, which can reduce the occurrence of avoidance and evasion. In addition, educated and healthy labor forces are more productive, which translates into higher income and output, contributing to increased tax revenue. In general, if a tax system is progressive, higher-income individuals pay a higher proportion of their income in taxes than lower-income individuals. As a result, the government can mobilize more revenue from those with higher incomes. In addition, with high income, people will contribute to increased government tax revenue through various ways such as increased consumption and investment. In short, there is a positive relationship between HDI and tax revenue across various channels.

In conclusion, various factors affect tax revenue, categorized into economic, political, institutional, socio-cultural, external, legal, and business cycles. Based on the available data, this study selects variables relevant to the region to analyze after reviewing the studies on the determinants of tax revenue in Southeast Asia.

The Determinants of Tax Revenue in Southeast Asia

Studies on the determinants of tax revenue in Southeast Asia are relatively scarce. In general, factors that were found to positively affect tax revenues include trade openness, FDI, the ratio of foreign debt to GDP, and the share of value-added in industry to GDP; while ODA and the share of agriculture value-added have a negative relationship with tax revenue (Minh Ha et al., 2022; Saptono & Mahmud, 2021). In addition, the study by Syadulla (2015), focusing on the relationship between governance and tax revenue, found various variables such as corruption, voice and accountability, and political stability to have significant negative effects on the tax ratio, while the variables that have a positive impact on the tax ratio include the rule of law and quality of regulation. However, Maryantika and Wijaya (2023) found no impact of corruption on tax revenue in the case of Indonesia, suggesting an inconclusive relationship between corruption and tax revenue. In addition, HDI was used as one of the explanatory variables and found to be positively correlated with tax revenue in the study on the case of Indonesia by Lestari and Yolanda (2023).

In conclusion, in Southeast Asia, factors influencing tax revenues include trade openness, FDI, the ratio of debt to GDP, agriculture, and industry value added, ODA, governance, and HDI. Since HDI was found to have a positive relationship with tax revenue, the current study is expected to contribute to the literature on the determinants of tax revenue in Southeast Asia by incorporating HDI and government effectiveness as the main policy variables to extend the econometric analysis of Minh Ha et al. (2022). In addition, the current study analyzed the more extended period and recent data sets.

Current Tax Revenue in Southeast Asia

The effort to raise tax revenue differs from region to region and among different groups of economies. According to the revenue statistics published by OECD (2023), the tax revenue as the ratio to GDP in 2021 was the highest in OECD countries (34.1 percent), followed by countries in Latin America and the Caribbean (21.7 percent), Asia-Pacific (19.8 percent), and Africa (16.0 percent). However, some Sub-Saharan African economies performed better than Latin American countries in tax revenue collection (Sen Gupta, 2007), indicating that the regional average may overlook a specific country’s tax effort. Nonetheless, there is no comparison between Southeast Asian tax revenue and other regions.

Southeast Asia is one of the fastest-growing regions. This region is home to a heterogeneous group of countries in terms of languages, cultures, government systems, colonial legacies, and other aspects. In terms of income, the region comprises lower-middle-income, upper-middle-income, and high-income countries.

The rapid development and transformation in living standards and demographics across Southeast Asia exert considerable strain on public revenue and expenditure. On the spending side, governments face pressure to enhance services, requiring budget increases. However, revenue growth has not kept pace with the rising expenditure.

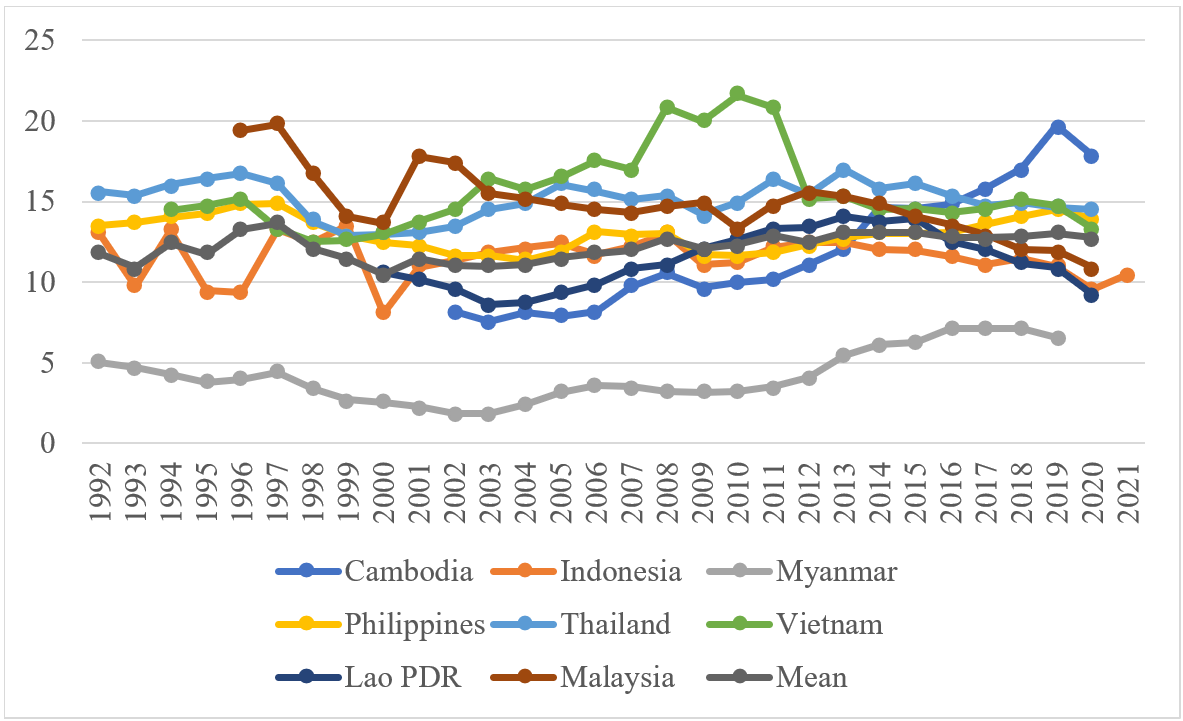

The Figure 1 shows the tax revenue trend as a percentage of GDP in eight Southeast Asian countries. Except for Myanmar, which has the lowest rate of tax revenue, the rate in the other countries fluctuates from around 10 percent to around 20 percent of GDP. The tax revenue in Cambodia has increased gradually from around 8 percent in 2002, when the data was first available, to about 18 percent in 2020, the highest among countries in the region. However, when the average rate is computed, it reveals that Thailand, Vietnam, and Malaysia have the highest average rate of tax revenue during the study period, followed by the Philippines, Cambodia, Indonesia, and Lao PDR. The rate is somewhat consistent with the general tendency that the more developed economies collect considerable tax revenue.

In sum, there is still room for increasing tax revenue in Southeast Asia since the ratio of tax revenue to GPD is still below the average of high-income countries. For this reason, it is crucial to understand the determinants of tax revenue.

Figure 1: Tax revenue (percentage of GDP) in Southeast Asia

Source: World Bank’s World Development Indicators and IMF

Methodology

Data Collected

The data used in this study is the panel data publicly available in the World Bank’s World Development Indicators online database, spanning from 1992 to 2022 for eight Southeast Asian countries: Cambodia, Indonesia, Lao PDR, Malaysia, Myanmar, the Philippines, Thailand, and Vietnam. Only the data on tax revenue, such as the percentage of GNI of Malaysia and Lao PDR, were retrieved from the IMF database since it is not available in the World Development Indicators online database. The panel is an unbalanced one as the availability of the data is different among the eight countries in terms of the year.

Statistical Method Used

Based on Min Ha et al. (2022), this study used panel data analysis to estimate the following regression equation.

Where:

i is the country (i = 1, 2, …,8 for eight countries in Southeast Asia)

t is the year (t = 1, 2, …,31 is the for the years from 1992 to 2022)

TAX is the tax revenue (percentage of GDP), a dependent variable

ODA is the net official development assistance received (percentage of GNI) and is expected to have a negative relationship with tax revenue

FDI is the net inflow of foreign direct investment (percentage of GDP) and is expected to be positively related to tax revenue

TRA is the sum of exports and imports of goods and services (as a percentage of GDP) and is expected to have a positive relationship with tax revenue

INF is the inflation measured by the consumer price index (annual percentage) and is expected to have a positive relationship with tax revenue

MAN is the manufacturing value-added (percentage of GDP) and is expected to be positively related to tax revenue

AGR is the agriculture, forestry, and fishing value-added (percentage of GDP) and is expected to have a negative relationship with tax revenue

DEB is the external debt stock (percentage of GNI). It is expected to be positively related to tax revenue. Due to data availability, the central government’s total debt (percentage of GDP) rather than the external debt stock was used for Malaysia

HDI is the UNDP’s Human Development Index (from 0 to 1, with 1 being the highest HDI) and is expected to be positively related to tax revenue

GEP is the government’s effectiveness (percentile rank) and is expected to have a positive relationship with tax revenue. According to the World Bank, government effectiveness reflects people’s perceptions of public service quality, civil service quality, independence from political influence, policy formulation and implementation quality, and the government’s commitment to credibility (World Bank, n.d.)

Eit is the disturbance terms

Results and Discussion

Results

Table 1 shows the descriptive statistics of the variables. As shown, the average tax revenue in the region is about 12 percent of GDP, with a minimum of about two percent and a maximum of about 22 percent. In addition, data on several variables are worth noting. ODA accounts for about 2.7 percent of GNI on average, with a minimum value of -0.6 percent, indicating that the country is a donor, not an aid recipient, as the country sent ODA to other countries. FDI also shows that Southeast Asian countries not only receive FDI but also invest in other countries. The variable trade (TRA) indicates that Southeast Asian countries are very open to trade, with an average trade volume of about 100 percent of their GDP, and the maximum is as large as about 220 percent of the GDP. The external debt stock variable DEB shows a heterogeneous picture of the region. DEB averages around 63.8 percent of the GNI. However, the interval is very large, with a minimum value of about 43 percent and a maximum value of about 267 percent. This large interval reflects different features of each country’s budget and public financial policies, as well as the ability of the country to access finance and service the debt. The HDI index shows an average of 0.576, with a minimum value of 0.356, indicating that the country is in the group of Low Human Development. This low HDI is because the data ranges from 1995 to 2021; the least developed countries in the region have improved their development indicators, and in 2021, all countries were at least in the group of Medium Human Development. Southeast Asian countries have not performed well, as indicated by the percentile rank of government effectiveness. On average, the percentile rank is about 43.4, which means that the regions perform better than 43.4 percent but worse than 56.6 percent of the countries in the ranking; however, the data for each country shows that many countries are in the percentile rank of lower than 30 percent.

Table 1. Descriptive statistics

Source: World Bank’s World Development Indicators and IMF

Note: Tax revenue as a percentage of the GNI of Malaysia and Lao PDR was retrieved from the IMF database since it was not available in the World Bank’s World Development Indicators online database.

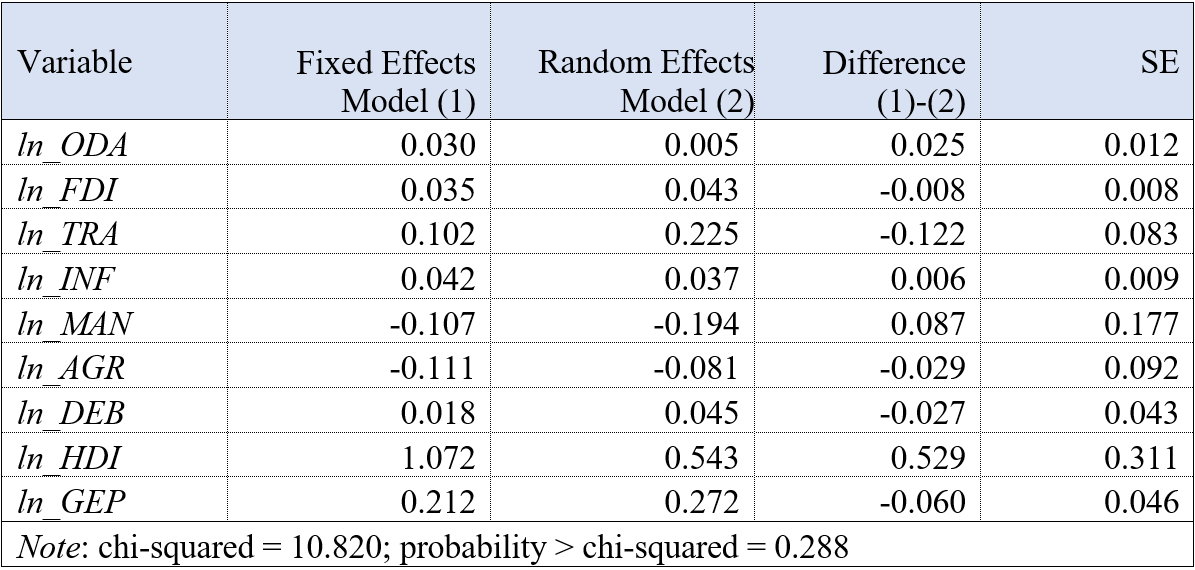

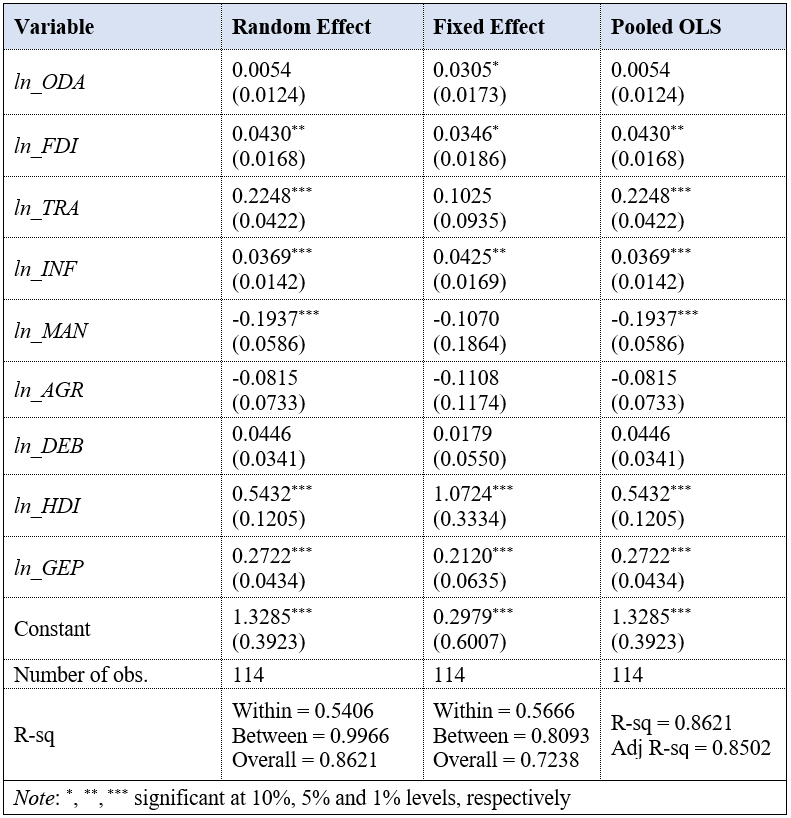

To explore the relationship between tax revenue and the explanatory variables, we used panel data regression to estimate the fixed effects and random effects models. The Hausman test was then used to compare the appropriateness of the fixed effects and the random effects models, and the pooled OLS was estimated to compare the coefficients of the three models.

Table 2 shows the results of the Hausman test. According to the result, the random effects model is preferable for the analysis. Table 3 shows the estimated coefficients of the three models: the random effects, the fixed effects, and the pooled OLS.

Table 2: The results of the Hausman test

Source: Author’s calculation

As the random effects model is preferable, its coefficients will be analyzed, while the fixed effects model and the pooled OLS will only be used for comparison and reference. Table 3 shows insufficient evidence of the significant relationship between ODA, the value added of agriculture, forestry, and fishing, and debt stock on tax revenue. A positive and significant relationship exists between FDI, trade, and inflation on tax revenue. That is, the larger the inflow of FDI, the larger the tax revenue the government can collect. Also, the increase in trade volume, the sum of imports and exports, will allow the government to collect various taxes, thus increasing tax revenue. Inflation also had a positive and significant relationship with tax revenue. As prices rise, the tax base will be enlarged so the government can collect more tax revenue.

Manufacturing value added was found to have a significant and negative relationship with tax revenue; that is, when the share of manufacturing value added increases, tax revenue will decline. HDI, which characterizes the development stage of countries, was found to have a significant and positive relationship with tax revenue. That means the higher the HDI, the larger the tax revenue the government can collect. HDI is a composite index of income, health, and education. A higher HDI indicates that the country is more developed with higher income and more productive workforces; therefore, the government can collect more tax revenue. It also means that when workforces are more productive, healthier, and better educated, they can contribute to a larger GDP and better understand the importance of tax revenue, thus complying well with the tax obligation. Therefore, higher HDI is correlated positively with larger tax revenue.

Table 3: The determinants of tax revenue

Source: Author’s calculation

This study found that FDI has a positive relationship with tax revenue. This finding is consistent with previous studies in developing countries (Camara, 2023) and Southeast Asia (Minh Ha et al., 2022). The same positive impact was also found in the case of eight West African countries (Okey, 2013). The inflow of FDI will boost economic activities and bring various benefits to the economy through job creation, technology transfers, and exports; thus, larger tax revenue will possibly be mobilized.

In addition to FDI, trade was also found to have a positive relationship with tax revenue. The literature on the impact of trade openness or liberalization has shown mixed results. For instance, Khattry and Rao (2002) found that low-income and upper-middle-income countries experienced declining tax revenue after liberalizing, which is contrary to the findings of this study. However, the result of the current study is consistent with those of Gnangnon and Brun (2019) and Gaalya et al. (2017), which found that countries that are open to trade, theoretically, will benefit from the gain from trade in terms of improved welfare of the people, the benefit of their comparative advantage, and economies of scale.

Inflation was found to be positively correlated with tax revenue. It has a distortion effect by shifting taxpayers to a higher tax bracket, which they usually have to pay higher taxes; thus, inflation will increase both the real tax paid and the marginal tax rate (Beer et al., 2023). In addition to rising tax revenue, the government benefits from inflation by reducing real public debt. However, this benefit is found to be temporary. If inflation is persistent, it will cause negative consequences to the economy. As taxation is already considered a burden to the taxpayers, inflation will be another burden; the two burdens will double the pain (Robson & Laurin, 2023).

The share of manufacturing in the GDP is expected to have a positive relationship with tax revenue. As manufacturing is associated with more modern and larger-scale industries, it is easier for the government to tax manufacturing than imposing tax on small-scale agriculture. Therefore, the coefficient of the manufacturing is expected to be positive. In Southeast Asia, studies such as those of Min Ha et al. (2022) and Saptono and Mahmud (2021) found that the manufacturing value added contributes to increasing tax revenue. However, this study found the opposite result. The reason may be that as many governments liberalize trade and provide incentives to manufacturing firms through tax holidays or reducing profit tax to encourage them to increase output and export, they see decreasing tax revenue from manufacturing sectors.

This study is different from Min Ha et al. (2022) and Saptono and Mahmud (2021) since HDI was used as one of the regressors rather than the per capita income, education, and life expectancy separately. HDI is a composite index that captures income, education, and health outcomes. It was found to have a positive and significant relationship with tax revenue. Studies that analyze the relationship between HDI and tax revenue are scarce. In the case of Turkey, Bayar and Sasmaz (2022) found an interplay between tax revenue and HDI; that is, higher HDI will increase tax revenue, while higher tax revenue will increase human development.

Finally, it was found that government effectiveness has a positive relationship with tax revenue. If the government effectiveness, which is the percentile rank of each country vis a vis the group, increases, tax revenue will also increase. In the study of governance and tax revenue in ASEAN countries, Syadulla (2015) used different governance indicators as explanatory variables for tax revenue; government effectiveness was one of the variables, but it was found to have no significant relationship with tax revenue. The study by Yaru and Raji (2022) in Sub-Saharan Africa confirms that no significant relationship exists between government effectiveness and tax revenue. The authors examined various governance indicators and found that only corruption significantly negatively impacts tax revenue. In contrast, other factors, such as political stability and absence of violence, rule of law, regulatory quality, voice, and accountability, had no significant relationship with tax revenue. Therefore, the current study provides evidence of the significant and positive relationship between government effectiveness and tax revenue.

Conclusion and policy implications

Tax is one of the most important sources of government revenues. As the pressure to mobilize tax revenue is mounting and many governments face mounting budget deficits, there is an increasing need to understand the factors influencing the revenue. Government effectiveness, one of the significant determinants of tax revenues, plays a vital role in revenue mobilization. Improving effectiveness is one of the policy options that the government can use to prove its accountability to taxpayers, maximize tax revenue, and reduce revenue leakage. When the government can mobilize revenue to finance public services expenditure as well as public investment that will improve the well-being of the people, that is, improving HDI, the government will be able to mobilize increasing revenue to further finance their capital and current expenditure needs. Thus, efficient tax revenue mobilization will produce an inducement effect that will keep the economy in a virtuous cycle of development.

Like this study, cross-country analyses overlook variables that influence tax revenue in individual countries. For instance, countries may implement different policies and utilize different technologies for tax collection. Therefore, future studies may consider conducting in-depth analyses within a single country, incorporating variables that are difficult to analyze in a cross-country context, such as specific tax policies and structures.

Acknowledgment

The earlier version of this paper was presented at the 18th International Convention of the East Asian Economic Association (EAEA) at Seoul National University, Republic of Korea. The author would like to extend sincere gratitude to CamEd Business School for providing financial support to attend the conference and undertake this research project.

References

Acemoglu, D., Naidu, S., Restrepo, P., & Robinson, J. A. (2019). Democracy does cause growth. Journal of Political Economy, 127(1), 47–100. https://doi.org/10.1086/700936

Ajaz, T., & Ahmad, E. (2010). The effect of corruption and governance on tax revenues. The Pakistan Development Review, 49(4), 405–417.

Alasfour, F., Samy, M., & Bampton, R. (2016). The determinants of tax morale and tax compliance: Evidence from Jordan. In J. Hasseldine (Ed.), Advances in taxation (pp. 125 – 171). Emerald Group Publishing Limited.

https://doi.org/10.1108/S1058-749720160000023005

Anh, L. H., & Thinh, T. Q. (2018). Factors impacting tax revenue of Southeast Asian Countries. In L. H. Anh, L. S. Dong, V. Kreinovich, & N. N. Thach (Eds.) Econometrics for Financial Applications (pp. 514-530). Springer International Publishing. https://doi.org/10.1007/978-3-319-73150-6_41

Asghar, F., & Mehmood, B. (2017). Effects of trade liberalization on tax revenue in Pakistan. Pakistan Economic and Social Review, 55(1), 187–212.

Avi-Yonah, R. S. (2006). The three goals of taxation. Tax Law Review, 60 (1), 1-28.

Barro, R. J. (1996). Democracy and growth. Journal of Economic Growth, 1, 1–27. https://doi.org/10.1007/BF00163340

Bayar, Y., & Sasmaz, M. U. (2022). Human development and tax revenues: Evidence from Turkiye. In Proceedings of 15th SCF International Conference on Economic, Social, and Environmental Sustainability in the Post COVIOD-19 World, 59-64. https://www.researchgate.net/profile/Oguzhan-Yelkesen/publication/369236940_The_Determinants_of_Sustainable_Development_in_E7_Economies_Insights_from_Panel_ARDLPMG_Approach/links/644b97d14af78873524562ce/The-Determinants-of-Sustainable-Development-in-E7-Economies-Insights-from-Panel-ARDL-PMG-Approach.pdf#page=65

Beer, S., Griffiths, M., Griffiths, M. M. E., Klemm, A., & Klemm, M. A. D. (2023). Tax distortions from inflation: What are they? How to deal with them? Public Sector Economics, 47(3), 353-386. https://doi.org/10.3326/pse.46.3.3

Benedek, D., Crivelli, E., Gupta, S., & Muthoora, P. (2014). Foreign aid and revenue: Still a crowding-out effect? FinanzArchiv/Public Finance Analysis, 70(1), 67–96. https://doi.org/10.1628/001522114X679156

Besley, T., & Persson, T. (2014). Why do developing countries tax so little? Journal of Economic Perspectives, 28(4), 99–120. http://dx.doi.org/10.1257/jep.28.4.99

Burgess, R., & Stern, N. (1993). Taxation and development. Journal of Economic Literature, 31(2), 762–830.

Camara, A. (2023). The effect of foreign direct investment on tax revenue. Comparative Economic Studies, 65(1), 168–190. https://doi.org/10.1057/s41294-022-00195-2

Crowe, D., Haas, J., Millot, V., Rawdanowicz, Ł., & Turban, S. (2022). Population ageing and government revenue: Expected trends and policy considerations to boost revenue. OECD Economics Department Working Papers No. 1737. https://doi.org/10.1787/9ce9e8e3-en

Deng, X., & Smyth, R. (2000). Non‐tax levies in China: Sources, problems and suggestions for reform. Development Policy Review, 18(4), 391–411. https://doi.org/10.1111/1467-7679.00118

Devarajan, S., & Do, Q.-T. (2023). Taxation, accountability, and cash transfers: Breaking the resource curse. Journal of Public Economics, 218, 104816. https://doi.org/10.1016/j.jpubeco.2022.104816

Dougherty, S., de Biase, P., & Lorenzoni, L. (2022). Funding the future: The impact of population ageing on revenues across levels of government. OECD Fiscal Federalism Working Paper Series. https://doi.org/10.1787/2b0f063e-en

Durán‐Cabré, J. M., Esteller‐Moré, A., & Salvadori, L. (2020). Cyclical tax enforcement. Economic Inquiry, 58(4), 1874–1893. https://doi.org/10.1111/ecin.12902

Ermasova, N., Haumann, C., & Burke, L. (2021). The relationship between culture and tax evasion across countries: Cases of the USA and Germany. International Journal of Public Administration, 44(2), 115–131. https://doi.org/10.1080/01900692.2019.1672181

Fu, Q., & Chang, C.-P. (2021). How do pandemics affect government expenditures? Asian Economics Letters, 2(1). https://doi.org/10.46557/001c.21147

Gaalya, M. S., Edward, B., & Eria, H. (2017). Trade openness and tax revenue performance in East African countries. Modern Economy, 8(5), 690–711. https://doi.org/10.4236/me.2017.85049

Gnangnon, S. K., & Brun, J. (2019). Trade openness, tax reform and tax revenue in developing countries. The World Economy, 42(12), 3515–3536. https://doi.org/10.1111/twec.12858

Gropp, R., Ebrill, L. P., & Stotsky, J. G. (1999). Revenue implications of trade liberalization. International Monetary Fund Occasional Paper. https://doi.org/10.5089/9781557758132.084

Gwartney, J. D., & Lawson, R. A. (2006). The impact of tax policy on economic growth, income distribution, and allocation of taxes. Social Philosophy and Policy, 23(2), 28–52. https://doi.org/10.1017/S0265052506060158

Han, X., Su, J., & Thia, J. P. (2021). Impact of infrastructure investment on developed and developing economies. Economic Change and Restructuring, 54(4), 995–1024. https://doi.org/10.1007/s10644-020-09287-4

Hemels, S. (2017). Tax incentives as a creative industries policy instrument. In S. Hemels & K. Goto (Eds.), Tax incentive for the creative industries. Springer. https://doi.org/10.1007/978-981-287-832-8_4

Högström, J., & Lidén, G. (2023). Do party politics still matter? Examining the effect of parties, governments and government changes on the local tax rate in Sweden. European Political Science Review, 15(2), 235–253. https://doi.org/10.1017/S1755773922000388

Ibadin, P. O., & Oluwatuyi, B. T. (2021). Tax revenue, economic growth and human development index in Nigeria. Journal of Taxation and Economic Development, 20(2), 52–76.

Karimi, M., Kaliappan, S. R., Ismail, N. W., & Hamzah, H. Z. (2016). The impact of trade liberalization on tax structure in developing countries. Procedia Economics and Finance, 36, 274–282. https://doi.org/10.1016/S2212-5671(16)30038-7

Khattry, B., & Rao, J. M. (2002). Fiscal faux pas?: An analysis of the revenue implications of trade liberalization. World Development, 30(8), 1431–1444. https://doi.org/10.1016/S0305-750X(02)00043-8

Kwak, S. (2013). Tax base composition and revenue volatility: Evidence from the US states. Public Budgeting & Finance, 33(2), 41–74.https://doi.org/10.1111/j.1540-5850.2013.12008.x

Lestari, F. A. P., & Yolanda, Y. (2023). Determinants of tax revenues and human development index in Indonesia. International Journal of Multidisciplinary: Applied Business and Education Research, 4(4), 1287-1298. https://doi.org/10.11594/ijmaber.04.04.24

Maryantika, D. D., & Wijaya, S. (2022). Determinants of tax revenue in Indonesia with economic growth as a mediation variable. JPPI (Jurnal Penelitian Pendidikan Indonesia), 8(2), 450-465. http://dx.doi.org/10.29210/020221522

Menon, J. (2023, February 20). Southeast Asian economies: Out of the storm, clouds on the horizon. Fulcrum. https://fulcrum.sg/southeast-asian-economies-out-of-the-storm-clouds-on-the-horizon/

Minh Ha, N., Tan Minh, P., & Binh, Q. M. Q. (2022). The determinants of tax revenue: A study of Southeast Asia. Cogent Economics & Finance, 10(1), 2026660. https://doi.org/10.1080/23322039.2022.2026660

OECD (2023). Revenue statistics in Asia and the Pacific 2023 ─ Cambodia. https://www.oecd.org/tax/tax-policy/revenue-statistics-asia-and-pacific-cambodia.pdf

Okey, M. K. N. (2013). Tax revenue effect of foreign direct investment in West Africa. African Journal of Economic and Sustainable Development, 2(1), 1–22. https://doi.org/10.1504/AJESD.2013.053052

Prezas, A. P. (1991). Inflation, investment, and debt. Journal of Financial Research, 14(1), 15–26. https://doi.org/10.1111/j.1475-6803.1991.tb00641.x

Prichard, W., Salardi, P., & Segal, P. (2018). Taxation, non-tax revenue and democracy: New evidence using new cross-country data. World Development, 109, 295–312. https://doi.org/10.1016/j.worlddev.2018.05.014

Robson, W. B., & Laurin, A. (2023). Double the pain: How inflation increases tax burdens. CD Howe Institute E-Brief, 344. https://dx.doi.org/10.2139/ssrn.4538814

Saptono, P. B., & Mahmud, G. (2021). Macroeconomic determinants of tax revenue and tax effort in Southeast Asian countries. Journal of Developing Economies, 6(2), 253-274. https://doi.org/10.20473/jde.v6i2.29439

Sen Gupta, A. (2007). Determinants of tax revenue efforts in developing countries. International Monetary Fund Working Paper. https://www.imf.org/en/Publications/WP/Issues/2016/12/31/Determinants-of-Tax-Revenue-Efforts-in-Developing-Countries-21040

Stone, M., & Saxena, S. (2020). Special series on fiscal policies to respond to COVID-19 preparing public financial management systems for emergency response challenges. International Monetary Fund, 1–6. https://www.imf.org/-/media/Files/Publications/covid19-special-notes/special-series-on-covid19-preparing-public-financial-management-systems-for-emergency-response.ashx

Syadullah, M. (2015). Governance and tax revenue in Asean countries. Journal of Social and Development Sciences, 6(2), 76–88. https://doi.org/10.22610/jsds.v6i2.845

Tagem, A. M. E., & Morrissey, O. (2023). Institutions and tax capacity in sub-Saharan Africa. Journal of Institutional Economics, 19(3), 332–347. https://doi.org/10.1017/S1744137422000145

Tanzi, M. V., & Zee, M. H. H. (2001). Tax policy for developing countries. International Monetary Fund. https://www.imf.org/en/Publications/Economic-Issues/Issues/2016/12/30/Tax-Policy-for-Developing-Countries-4010

Thornton, J. (2014). Does foreign aid reduce tax revenue? Further evidence. Applied Economics, 46(4), 359–373. https://doi.org/10.1080/00036846.2013.829207

Torgler, B. (2002). Does culture matter? Tax morale in an East-West-German comparison. FinanzArchiv/Public Finance Analysis, 504–528. https://doi.org/10.1628/0015221032500856

Wang, E. C. (2002). Public infrastructure and economic growth: A new approach applied to East Asian economies. Journal of Policy Modeling, 24(5), 411–435. https://doi.org/10.1016/S0161-8938(02)00123-0

World Bank (n.d.). Metadata glossary. https://databank.worldbank.org/metadataglossary/worldwide-governance-indicators/series/GE.PER.RNK.UPPER

Yaru, M. A., & Raji, A. S. (2022). Corruption, governance and tax revenue performance in Sub-Saharan Africa. African Journal of Economic Review, 10(1), 234–253.