Print ISSN : 2708-616X | Online ISSN : 2708-6178 | Title DOI: https://doi.org/10.62458/160224

Volume 9 | Number 2 | July – December 2024 | DOI: https://doi.org/10.62458/jafess923

Received : July 2024 | Revised: September 2024 | Accepted: December 2024

Zubir Azhar, PhD ![]()

Universiti Sains Malaysia, Malaysia

Email: [email protected]

CamEd Business School, Cambodia

Email: [email protected]

Monileak Siem

National University of Management

ABSTRACT

Purpose: This study seeks to explore the connection between corporate social responsibility (CSR) performance and tax avoidance (TA) among a sample of Cambodian companies listed on the Cambodian Securities Exchange (CSX). It also investigates whether board independence moderates the relationship between these two variables.

Methodology: Several statistical analyses have been conducted using the effective tax rate (ETR) and extracting accounting data from these companies’ annual reports.

Findings: The study reveals that Cambodian companies investing significant resources in charitable initiatives are less likely to participate in TA practices. It has also been realized that the influence of CSR in mitigating the likelihood of engaging in TA practices is boosted in firms with a higher proportion of independent directors.

Implications: The study’s findings have significant policy implications as they contribute to a better understanding of TA practices and CSR. This understanding can benefit numerous investors, regulators, and academics interested in firms’ tax behavior. Furthermore, the findings can aid tax administrations in identifying conditions that heighten the risk of TA practices, thereby assisting in formulating effective tax systems that enhance firms’ tax compliance.

Originality: This study represents one of the initial inquiries into the relationship between CSR and TA practices in Cambodia. It provides a unique perspective by furnishing empirical evidence on this relationship within the Cambodian context, which differs from other cultural and institutional environments where previous studies have been conducted. It also offers new insights into how the independence of board directors moderates the relationship between CSR and TA.

Limitations: This study primarily relies on firms’ disclosed donation figures in financial statements. As such, the study may only partially represent the extent of CSR involvement and potentially impact the accuracy of CSR assessment.

Keywords: Corporate social responsibility; Tax avoidance; Effective tax rate; Cambodia

INTRODUCTION

Taxation is intricately linked to the welfare of society as it serves as a vital source of revenue for national fiscal purposes, facilitating investments in domestic infrastructure, education, healthcare, national defense, public transportation, and law enforcement. Consequently, adhering to the fundamental principles of tax law is crucial for a firm to establish legitimacy within society and maintain a positive relationship with tax authorities (Ostas, 2004; Rose, 2007; Wierzbicki & Werner, 2023). It can be argued that a firm’s compliance with tax laws and the contribution of its fair share of taxes lawfully collected by governments in any country of operation is a fundamental obligation toward society (Christensen & Murphy, 2004; Rabbi & Almutairi, 2021).

Despite taxes’ crucial role in fostering a favorable corporate environment, some firms perceive them merely as costs to be minimized. They engage in legal but strategic tax practices aimed at reducing corporate taxes by avoiding tax payments due through formal compliance with the law without trying to breach it, which is known as tax avoidance (TA) practices (Avi-Yonah, 2008; Lenz, 2020).

Management may become incentivized to engage in TA practices to benefit shareholders in the short term due to the cash savings such practices provide. Managers can then utilize these savings to generate future shareholder wealth. However, engaging in such practices could jeopardize the firm’s sustainability and diminish its market value. The media frequently scrutinizes these practices, and consumers tend to be more aware of socially irresponsible activities than socially responsible ones. Consequently, the negative publicity surrounding TA practices can inflict reputational damage on firms, potentially leading to financial harm for their shareholders (Lanis & Richardson, 2012; Dhaliwal et al., 2022).

On the other side, there is a great awareness of the role of business toward society as a whole, leading to the emergence of corporate social responsibility. While the definition of this term is contested, the explanation given by Carroll (1979, p.500) is the most commonly recognized. He proposed this description of CSR: “… the social responsibility of business encompasses the economic, legal, ethical and discretionary expectations that society has of organizations at a given point in time.”

It can be argued that TA practices deviate from the principles of CSR, as TA practices harm companies and their shareholders and impact the citizens and governments of nations serving as tax havens for these practices. As earnings are stripped and shifted to jurisdictions with lower tax rates, governments struggle to maintain essential services. Consequently, TA behaviors are widely viewed as irresponsible by government institutions and the public (Knuutinen, 2013).

In line with legitimacy theory (Dowling & Pfeffer, 1975), a company’s legitimacy is essential for its survival, and society holds certain expectations regarding the proper conduct of businesses. Therefore, it can be claimed that TA practices are incongruent with CSR since they impose costs on society and may be perceived as unethical and irresponsible by the public and the press. Several empirical studies (Hoi et al., 2013; Landry et al., 2013; Lanis & Ricardson, 2012; 2015) have indicated that CSR-oriented companies tend to have higher effective tax rates.

In contrast, according to risk management theory (Fombrun et al., 2000; Moser & Martin, 2012), CSR can be viewed as a risk management strategy to prevent potential damage to a company’s reputation that might arise from involvement in harmful practices. Since TA practices can expose firms to significant risks, including loss of reputation, heightened political and media scrutiny, potential fines and penalties from tax authorities, and consumer boycotts of companies’ products, firms may seek to safeguard their reputation by actively managing CSR activities. Empirical support for this argument is provided by studies conducted by Borza and Stoian (2011), Davis et al. (2013), and Huseynov and Klamm (2012).

Given the conflicting findings from previous research, it is crucial to investigate this issue within the Cambodian context, particularly considering the need for more studies examining this topic among Cambodian-listed companies. Therefore, this study examines whether Cambodian non-financial firms with a tendency to engage in CSR endeavors exhibit a lower propensity to avoid their taxes. It also aims to investigate whether the proportion of independent directors can have a moderating influence on the relationship between CSR and TA, especially with their positive influence on motivating managers to participate in charitable activities and diminishing the firm’s likelihood of engaging in TA practices.

Independent board members are obligated to stockholders, other key stakeholders, and, most importantly, the general public (Ibrahim et al., 2003). Furthermore, Armstrong et al. (2015), Lanis and Richardson (2011), Minnick and Noga (2010), Richardson et al. (2013), and Salhi et al. (2020) demonstrated the effectiveness of independent directors as an internal control device about a company’s tax policy. Furthermore, previous research (e.g., Wang & Dewhirst, 1992; Ibrahim & Angelidis, 1995; Coffey & Wang, 1998; Johnson & Greening, 1999; Ibrahim et al., 2003; Webb, 2004; Dunn & Sainty, 2009; Jo & Harjoto, 2011; Post et al., 2011; Sahin et al., 2011; Shaukat et al., 2016) has established that such board members have a positive impact on motivating firms to engage in CSR practices.

Based on this argument, independent boards should know that fulfilling tax rules aligns with CSR and should also inform managers that enhancing CSR participation necessitates a commitment to pay a fair share of tax. As a result, independent board members can moderate the association between CSR and TA.

The remaining sections of this paper are structured as follows: Section 2 provides an overview of the literature and presents hypotheses based on theoretical background. Section 3 outlines the research methodology employed. Research findings are discussed in Section 4. Finally, Section 5 offers conclusions, discusses the implications of the results, acknowledges study limitations, and proposes avenues for future research.

LITERATURE REVIEW AND HYPOTHESES DEVELOPMENT

The Concept of Corporate Social Responsibility

The idea of CSR suggests that companies are real-world entities that must address the interests of the wider society and fulfill the expectations of various stakeholders such as personnel, stockholders, customers, societies, and governmental organizations (Jones, 1995).

A shift in perspective regarding a firm’s societal role has increased the focus on CSR. Traditionally, a firm was seen as accountable solely to its shareholders, with a relationship mainly between executives and shareholders (Friedman, 1962). The stakeholder-agency perspective has altered this view by recognizing managers as representatives of all stakeholders, not just shareholders (Hill & Jones, 1992; Jones, 1995), and perceiving the organization as a network of relationships with stakeholders with an implied social contract with the firm. Consequently, companies adopting CSR aim to fulfill stakeholder expectations and honor the social contract.

Although previous research has presented various definitions of this concept, Carroll’s (1979, P. 500) is the most commonly accepted. He defines the concept as “the social responsibility of business encompasses the economic, legal, ethical and discretionary expectations that society has of organizations at a given point in time.”

Based on this definition, CSR encompasses four obligations for companies: the economic duty focused on generating profit, the legal duty tied to adhering to regulations, the ethical duty involving just and fair actions, and the discretionary duty to be a responsible corporate citizen by contributing resources to benefit society as a whole.

The Concept of Tax Avoidance

Taxes are essential tools to provide governments with the necessary funds to manage and offer the necessary public goods and services and make them available to all members of society. However, the interest of companies in maximizing profitability in the short term resulted in considering the tax as a burden, and commitment to companies must be reduced or eliminated. Hence, management might contract with advisers and experts in the field of tax to formulate tax strategies aimed at avoiding payment of the tax due through exploiting the legal loopholes permitted by the law to exempt or circumvent the text in explanation or application or create facts that are compatible with the legal texts and contradict the content of the texts. Therefore, companies seek to avoid the tax aggressively through formal compliance with the law without trying to breach it, known as TA (Avi-Yonah, 2008; Lenz, 2020).

There is no globally acknowledged definition of TA. Hanlon and Heitzman (2010) define it as a sequence of tax strategic initiatives to lower the amount of stated tax, while Jones (2012) outlines it as a viable way to reduce taxes. Meanwhile, TA is expressed as the descending management of income tax through legal, questionable, or illegal tax planning methods (Lanis & Richardson, 2012). It is also described by Lee et al. (2015) as a company’s intentional endeavor to decrease its tax liability using legal or unlawful methods or plans.

The Relationship between CSR and TA

Companies’ decisions and practices directly impact society as a whole because business is an integral part of society that affects and is affected by it. Therefore, one of the key social responsibilities of companies is adhering to tax regulations, as taxation serves as a crucial mechanism for governments to acquire the essential funds required for delivering public services to all citizens.

The participation of firms in TA practices has depleted corporate tax funds, leading to a reduction in state tax revenue and, consequently, the incapability of the state to deliver public services. Firms’ involvement in such behaviors directly affects society. Hence, TA practices are inconsistent with the principles of CSR (Knuutinen, 2013).

Many scholars are driven to explore the connection between CSR involvement and TA practices, often employing legitimacy and risk management theories to interpret this relationship. These two theories propose two different viewpoints regarding the association between these two variables. Legitimacy theory (Dowling & Pfeffer, 1975) posits that a firm’s legitimacy is crucial for its survival, as society holds expectations regarding businesses’ proper conduct, while risk management theory views CSR as a risk management mechanism, aiming to protect the firm’s reputation from potential harm resulting from participating in adverse activities (Fombrun et al., 2000; Moser & Martin, 2012; Rehman et al., 2020).

From a legitimacy standpoint, tax payment serves as a CSR instrument for establishing corporate legitimacy within society and is deemed a significant community contribution (Preuss, 2010). Conversely, according to risk management theory, companies might strategically handle CSR endeavors to shield themselves from the repercussions of engaging in aggressive TA practices, which could result in substantial adverse outcomes for the firm (Hoi et al., 2013).

As theories vary in their interpretation of the relationship between CSR endeavor and TA practices, empirical studies offer differing evidence on the nature of this association. Some research suggests that CSR has a negative effect on TA. For instance, Hoi et al. (2013) examine the impact of irresponsible CSR activities on TA across a sample of 3,000 US firms from 2003 to 2009. Their study reveals that companies exhibiting extremely irresponsible CSR activities, which refer to corporate actions generally perceived as detrimental to corporate governance, employee relations, societies, public health, human rights, diversity, the environment, and other related aspects, are more aggressive in TA. They are more likely to participate in tax-shielding behaviors and display greater variations in discretionary and permanent book-tax items. Landry et al. (2013) also investigated the link between CSR activities and fair tax contributions through a sample of 168 Canadian corporations between 2004 and 2008. Their study revealed that socially responsible companies are less inclined to engage in aggressive TA practices.

Based on data from the Vigeo database, Laguir et al. (2015) examine if the link between aggressive TA practices and CSR varies based on the type of CSR activities. They analyzed a sample of 24 French-listed firms and found that firms with higher levels of social CSR engagement tend to engage less aggressively in TA practices, while those with higher levels of environmental CSR engagement tend to be more aggressive in such adverse practices. Moreover, Lanis and Ricardson (2015) utilized a KLD database to assess CSR performance across a sample of firms in the USA spanning from 2003 to 2009. Their findings indicate that higher commitment to CSR correlates with a reduced likelihood of involving in TA practices.

Muller and Kolk (2015) contributed to the research on this topic by examining local companies compared to multinational corporations. They analyzed data from 82 Indian firms between 2000 and 2001. Their findings revealed that Indian multinational corporations pay a larger amount of taxes compared to national companies. Additionally, they observed that multinational corporations and their affiliates engaged in more CSR activities tend to pay higher taxes than those not prioritizing CSR activities. Besides, Amidu et al. (2016) explored the link between CSR and TA among a sample of non-financial companies listed on the Ghana Stock Exchange (GSE) and non-listed entities sourced from the Ghana Revenue Authority (GRA) database over four years from 2010 to 2013. Their findings suggest that Ghanaian firms exhibiting high levels of CSR involvement tend to participate less in tax avoidance practices.

Zeng (2016) provides further evidence indicating that Canadian CSR firms are less involved in TA practices. Analyzing a sample of Canadian corporations included on S&P/TSX60 over five years between 2005 and 2009; the findings suggest that companies with higher rankings in CSR are less likely to engage in aggressive TA practices. In addition, Park (2017) investigated the correlation between CSR endeavors and TA by analyzing residual and total book-tax differences (BTD) of a sample of 1,148 Korean-listed firms from 2004 to 2009. The findings revealed that firms with heightened CSR engagement demonstrated a reduced propensity for TA.

Utilizing an international sample spanning from 2006 to 2014, López‐González et al. (2019) examined the impact of CSR performance on TA and reported a negative association between these two variables. This indicates that companies with higher levels of CSR performance exhibit reduced tax-saving behaviors.

On the contrary, some researchers argue that tax payments of companies involved in CSR are insufficient. For instance, Huseynov and Klamm (2012) investigated the influence of various CSR measures (i.e., Corporate Governance, Society, and Diversity) on TA practices using a sample of 500 US firms from 2000 to 2008. They categorized each CSR measure into strengths and weaknesses, with TA assessed through the long-term effective tax rate (ETR). Their findings suggest that weaknesses in the societal aspect of CSR were positively associated with the ETR. In contrast, strengths in the corporate governance aspect and weaknesses in the diversity aspect had a negative impact on the ETR.

Employing data from KLD and Compustat databases, Davis et al. (2013) investigated the relationship between CSR involvement and the level of corporate tax payments and the extent of investment in tax reduction strategies across all publicly traded American companies from 2002 to 2010. Their findings revealed a negative correlation between CSR involvement and ETR and a positive association with expenditures on tax lobbying. This suggests that firms committed to CSR tend to pay lower taxes and be more active in tax lobbying efforts. Moreover, Watson (2015) explored the correlation between CSR and both acceptable and unacceptable TA practices by analyzing ETR and unrecognized tax benefits among a sample of US firms during the period between 2000 and 2011 and suggested that CSR-affiliated firms tended to exhibit lower ETR and higher levels of unrecognized tax benefits, signaling a notable presence of both acceptable and unacceptable TA practices within CSR-oriented companies.

Gulzar et al. (2018) investigated the impact of CSR on TA among Chinese-listed corporations. The study utilized CSR ratings obtained from Rankins, an agency that rates the CSR practices of Chinese companies, from 2009 to 2015. The authors discovered that more responsible companies were more likely to engage in tax avoidance practices than those considered less responsible. Within an international context, Zeng (2018) explored the link between CSR and TA within listed companies from the top 40 countries by GDP, spanning from 2011 to 2015, and utilized multiple proxies for TA practices. The study uncovered robust international evidence indicating a positive correlation between CSR and TA.

Alsaadi (2020) investigated the influence of financial-tax reporting conformity jurisdictions on the relationship between CSR and aggressive TA using a sample of European firms from 2008 to 2016. The findings indicate a positive correlation between CSR and TA. Additionally, firms in jurisdictions with low financial-tax reporting conformity are inclined to adopt CSR practices to mitigate the adverse effects of aggressive TA, contrasting with those in countries characterized by high financial-tax reporting conformity. Likewise, Abid and Dammak (2022) examined the impact of TA on CSR performance using a dataset of French non-financial firms from 2005 to 2016. Their findings suggest that companies with higher CSR scores are inclined to participate in aggressive TA practices.

More recently, Pandapotan (2023) explored the impact of CSR on TA within a sample of consumer goods manufacturing firms listed on the Indonesia Stock Exchange from 2019 to 2020. The study revealed a positive and significant relationship between these two variables. Drawing from an extensive review and analysis of prior research, it is evident that investigations into the correlation between CSR and TA practices have been approached from various theoretical perspectives and implemented across diverse economic landscapes, encompassing developed nations and emerging markets.

Given the conflicting findings regarding the association between CSR and TA practices and the dearth of studies focusing on Cambodian enterprises, this study aims to fill this gap by examining the Cambodian context. It is also noticed that all of the previously mentioned studies depend on using ETR as a measurement of TA and employing quantitative research design through statistically analyzing measurable data; therefore, this study follows the same research methodology.

In Cambodia, businesses that adhere to environmental and social responsibility standards are eligible for a tax holiday, a temporary duration during which the government decreases or eradicates specific taxes. These tax holidays in Cambodia can extend up to nine years, comprising a three-year exemption period followed by a regular increment in the tax rate over the subsequent six years. In light of the foregoing discussion, this paper proposes the following two opposing hypotheses:

H1a: There is a negative correlation between Cambodian listed companies’ level of Corporate Social Responsibility (CSR) performance and their extent of engaging in tax avoidance (TA) practices.

H1b: There is a positive correlation between Cambodian listed companies’ level of Corporate Social Responsibility (CSR) performance and their extent of engaging in tax avoidance (TA) practices.

The Moderating Role of Board Independence on the Relationship between CSR And TA

One integral aspect of corporate governance responsible for supervising top management and protecting the interests of stockholders is the board of directors (Fama & Jensen, 1983). There are two types of board members: executive and independent directors. Executive directors have management duties, while independent directors have no responsibilities for daily business management or operations. As a result, independent directors are considered to be more compelled to monitor management actions (Jensen & Meckling, 1976).

The existence of independent directors strengthens the board’s function as an agent for the shareholders. Because they come from outside the firm, do not have direct financial interests in the company, have closer relationships with stakeholders, know their expectations better, and are more willing to satisfy their demands, it is argued that the presence of independent directors with a larger number can effectively monitor top management and protect stakeholders. Moreover, such directors are proposed to supply their firms with more information, resources, and legitimacy, which could result in the best managerial decisions and consequently improve company performance (Hillman et al., 2000; Boivie et al., 2021).

Independent directors enhance the quality of business decisions by providing independent and objective expert advice and guidance to the management to preserve the interests of the stockholders, other stakeholders, and the overall community (Anderson & Reeb, 2004; Dahya & McConnell, 2005; Boivie et al., 2021). Independent directors also supply the company with the resources required for its sustainability and long-term effectiveness (Pfeffer & Salancik, 1978; Hillman & Dalziel, 2003; Kavadis & Thomsen, 2023).

With independent directors in a higher proportion, top management is more motivated to be concerned with society when putting the company’s strategy into action. Therefore, it is assumed that the presence of independent directors with a higher percentage may lead to the development of the company’s CSR performance. Previous research (for example, Wang & Dewhirst, 1992; Ibrahim & Angelidis, 1995; Coffey & Wang, 1998; Johnson & Greening, 1999; Ibrahim et al., 2003; Webb, 2004; Dunn & Sainty, 2009; Jo & Harjoto, 2011; Post et al., 2011; Sahin et al., 2011; Shaukat et al., 2016; Zaid et al., 2020) indicated that CSR engagement is improved in companies with a higher percentage of independent directors.

Besides the impact of independent directors in enhancing CSR performance, the presence of such directors could also influence the firm’s engagement in TA practices. Independent directors are more aware of the possible risks of severe tax positions and, as a result, should make every effort to mitigate TA (Armstrong et al., 2015). Several previous studies (e.g., Minnick & Noga, 2010; Lanis & Richardson, 2011; Richardson et al., 2013; Armstrong et al., 2015; Salhi et al., 2020) showed that the higher the proportion of independent directors, the lower the level of TA.

Based on the foregoing explanation, independent directors shall actively advocate increased business response to society’s viewpoints, which have been progressively concentrated on concerns about TA due to its negative social implications. They would also advise management that compliance with tax laws is consistent with increasing engagement in CSR activities; as such, two practices are effective for ensuring a good relationship with stakeholders. As a result, the existence of independent directors should moderate the link between CSR and TA. Accordingly, the following hypothesis is tested:

H2: The presence of independent directors will reinforce the negative association between CSR engagement and TA.

RESEARCH METHODOLOGY

Like most of the previous research on this topic, this study follows a quantitative research design that depends upon gathering and statistically analyzing measurable data. Ethical considerations of research are discussed before the method of extracting data and determining the research sample, the way of measuring the research variables, and the regression equations are presented.

Ethical Considerations of Research

Some ethical considerations have been taken into account when conducting the current research. These considerations include data privacy, confidentiality, transparency, and integrity. Although the data is sourced from publicly available annual reports, care has been taken to ensure that no confidential or sensitive information about companies or individuals is inadvertently disclosed or misinterpreted. The findings are also presented objectively, without bias or manipulation, ensuring that the data accurately reflects the companies’ activities. Misrepresentation of results could raise ethical concerns.

Data and Sample

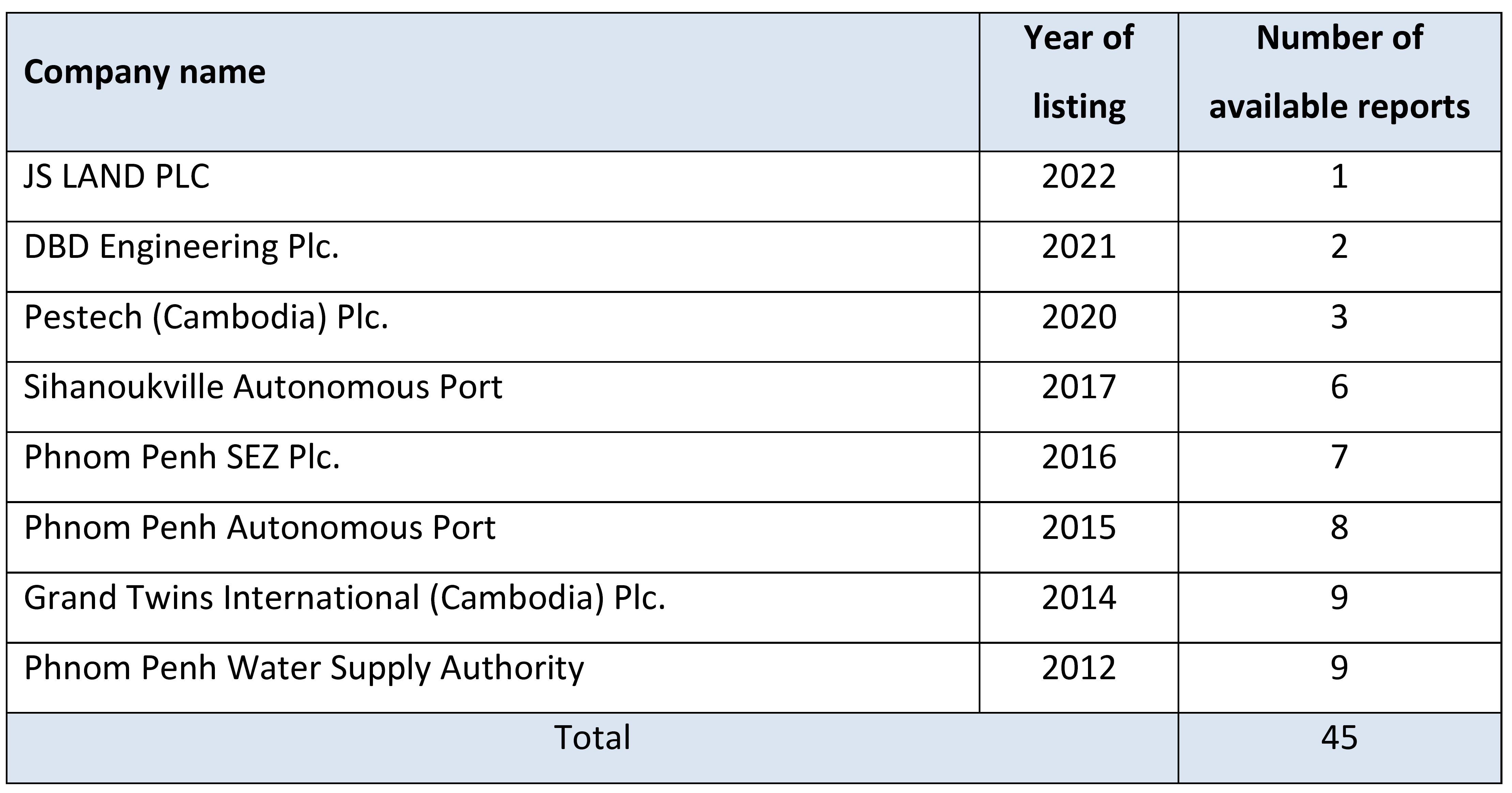

Financial data for the study variables are extracted from corporate financial statements. The research sample comprises all non-financial Cambodian firms listed on the Cambodian Securities Exchange (CSX) from 2014 to 2022. Given financial companies’ adoption of various accounting policies, they would be subject to different factors influencing TA. Therefore, these firms are excluded from the research sample. This study focuses on the eight non-financial companies listed on CSX during the study period. Despite the governmental nature of some of the sample companies, they are included among the research sample as it is argued that such entities might have incentives to engage in TA practices, as fraud has become a frequent issue in government agencies due to key factors such as perceived pressure, available opportunities, and rationalizations for engaging in fraudulent activities (Riskiyadi & Tarjo, 2021). Table 1 outlines the names of these companies, the year they were listed on CSX, and the number of available reports for each company since listing.

Table 1: Details of companies listed on the Cambodia Securities Exchange

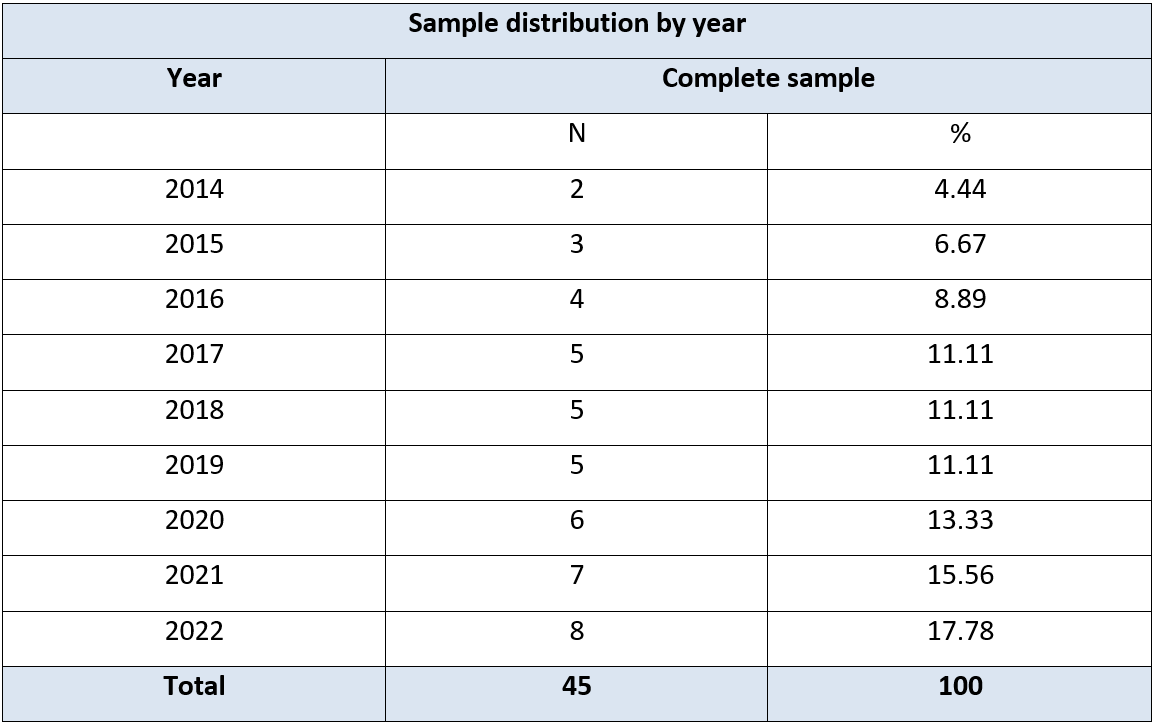

As illustrated in Table 1, the final sample comprised 45 firm-year observations. All observations classified by year are outlined in Table 2. According to Roscoe (1975, referenced in Sekaran & Bougie, 2016: 264), a sample size between 30 and 500 is sufficient for the vast majority of studies; therefore, it can be argued that the sample size of this study does not affect the estimated parameters of the regression.

Table 2: Sample distribution by industry and year

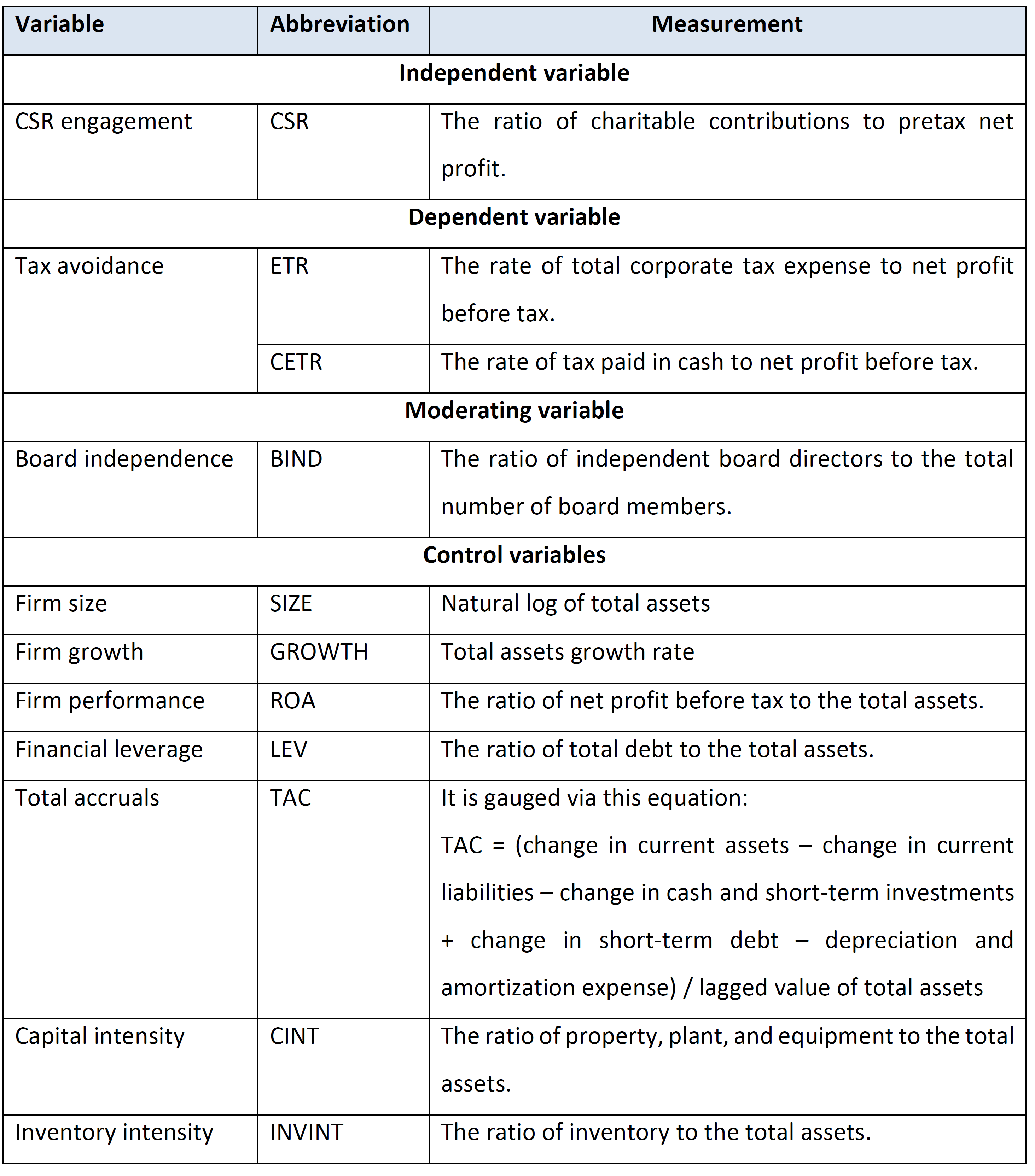

Variables Measurement

The Effective Tax Rate (ETR), commonly utilized as a gauge of TA, serves as the proxy for TA in this study. Two measurements were used in this study to calculate this rate. While the first measurement is the ratio of tax expense to pretax net earnings, the second is the fraction of taxes paid in cash to pretax net earnings. It is acknowledged that a distinction exists between tax expense and taxes paid. Tax expense encompasses deferred or accrued taxes, established based on accounting regulations yet susceptible to earnings management (Hanlon & Heitzman, 2010; Mamatzakis et al., 2023), while cash payments denote actual cash outflows. Due to lack of data about CSR engagement of Cambodian companies through databases, CSR engagement is evaluated by calculating the ratio of charitable contributions to pretax net profit as employed by previous research (e.g., Lev et al., 2010; Ramzan et al., 2021; and Vo et al., 2023).

The ratio of independent directors to the total number of board members is employed as a measurement of the power of board independence. Concerning control variables, prior research suggests some firm-specific variables that play a role in determining the level of TA. As a result, the base regression model incorporates various control variables related to the quality of earnings, financial performance, and other company characteristics.

The study incorporates firm size (SIZE) as a control variable to mitigate size-related influences. Drawing from Zimmerman (1983), smaller companies are anticipated to exhibit lower levels of tax avoidance than their larger counterparts. This expectation stems from smaller firms’ limited economic and political influence, which restricts their ability to minimize tax liabilities. In addition to firm size, the base regression model integrates variables such as total assets growth (GROWTH) and return on assets (ROA). This inclusion aligns with previous research by Gupta and Newberry (1997) and Adhikari et al. (2006).

According to Gupta and Newberry (1997), a company’s capital structure correlates empirically with its ETR, given that the tax deductibility of debt is inherent to the capital structure. Consequently, a company with substantial debt tends to exhibit a lower ETR; conversely, those with lesser debt tend to have a higher ETR. As such, financial leverage (LEV) is incorporated into this research as a control variable. Based on Desai and Dharmapala’s (2009) study, total accruals (TAC) are included as a control variable to ensure that the quality of earnings does not influence the correlation between CSR and tax avoidance.

Capital intensity (CINT) and inventory intensity (INVINT) are incorporated as control variables to manage the influence of fixed assets on the degree of tax avoidance. Stickney and McGee (1983) posit that capital-intensive firms may exhibit higher tax avoidance levels than inventory-intensive ones. The details regarding the study’s independent, dependent, and control variables are presented in the forthcoming table.

Table 3: Measurement of the study variables

Empirical Model

Upon data collection, the subsequent regression equations are assessed to check the first research hypothesis:

ETRi,t = α0 + α1 CSRi,t + α2 BINDi,t + α3 SIZEi,t + α4 ROAi,t + α5 LEVi,t + α6 GROWTHi,t + α7 CINTi,t + α8 INVINTi,t + α9 TACi,t + εi (1)

CETRi,t = α0 + α1 CSRi,t + α2 BINDi,t + α3 SIZEi,t + α4 ROAi,t + α5 LEVi,t + α6 GROWTHi,t + α7 CINTi,t + α8 INVINTi,t + α9 TACi,t + εi (2)

Where:

ETRi,t= The rate of total corporate tax expense to net profit before tax.

CETRi,t = The rate of tax paid in cash to net profit before tax.

CSRi,t= The ratio of charitable contributions to pretax net profit.

BINDi,t = The ratio of independent directors to the total number of board members.

SIZEi,t = The natural logarithm of total assets.

ROAi,t= The ratio of net profit before tax to the total assets.

LEVi,t = The ratio of total debt to the total assets.

GROWTHi,t= Total assets growth rate.

CINTi,t = The ratio of property, plant, and equipment to the total assets.

INVINTi,t= The ratio of inventory to the total assets.

TACi,t = Total accruals.

In order to test the moderating impact of board independence on the association between the level of CSR engagement and tax avoidance, an interacting variable between CSR and BIND (CSR*BIND) has been introduced in the following regression equations:

ETRi,t = α0 + α1 CSRi,t + α2 BIND + α3 CSR*BIND + α4 SIZEi,t + α5 ROAi,t + α6 LEVi,t + α7 GROWTHi,t + α8 CINTi,t + α9 INVINTi,t + α10 TACi,t + εi (3)

CETRi,t = α0 + α1 CSRi,t + α2 BIND + α3 CSR*BIND + α4 SIZEi,t + α5 ROAi,t + α6 LEVi,t + α7 GROWTHi,t + α8 CINTi,t + α9 INVINTi,t + α10 TACi,t + εi (4)

FINDINGS

Descriptive Statistics

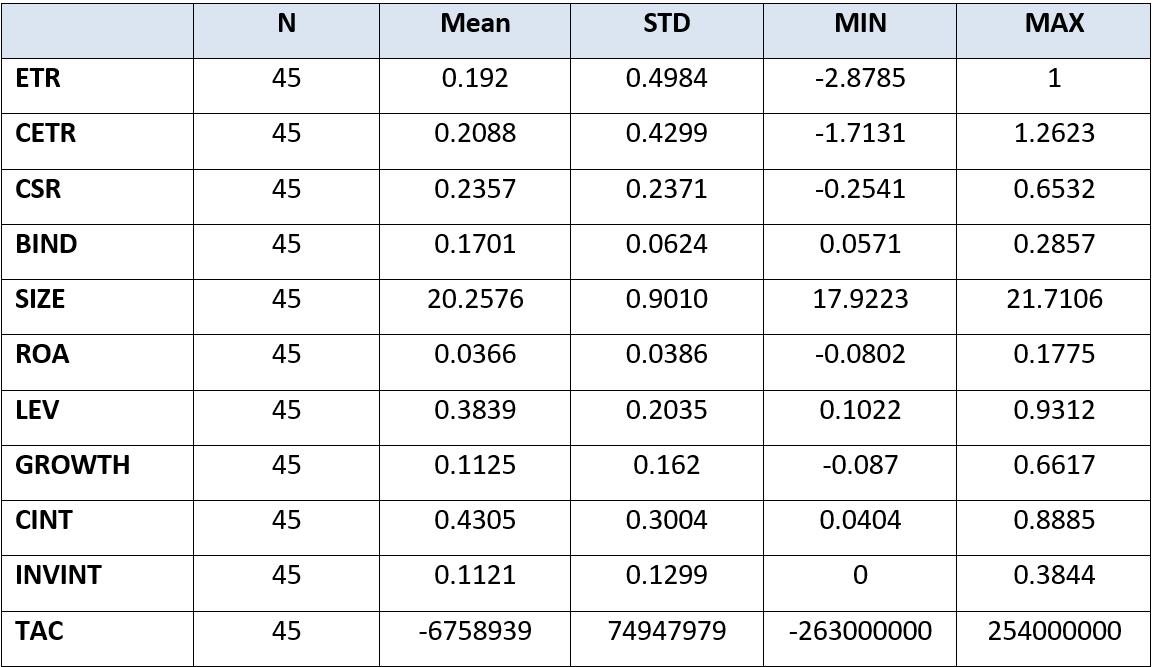

Table 4 presents the descriptive statistics of the research variables. The level of Cambodian companies’ engagement in TA practices differs significantly, as there is a significant variance between the lowest and highest values of both ETR and CETR. Similarly, the minimum and maximum values of CSR are -0.254 and 0.653, respectively, indicating that sample companies’ tendency to participate in charitable activities varies considerably.

Although there are no Cambodian listed companies without independent directors, the percentage of such directors does not exceed 29% of the total number of board members of these companies, as indicated by the descriptive statistics of the research variable related to board independence.

Although the descriptive statistics of SIZE specify that the size of sample companies is approximately similar, such indicators as ROA, LEV, and GROWTH exemplify the big variance in these firms’ financial performance, financial leverage, and growth opportunities.

The average of CINT is higher than that of INVINT, which illustrates that sample companies are more capital-intensive. The quality of earnings of Cambodian companies varies substantially, as revealed by the statistical indicators of TAC.

Table 4: Descriptive statistics of research variables

Pairwise Correlation

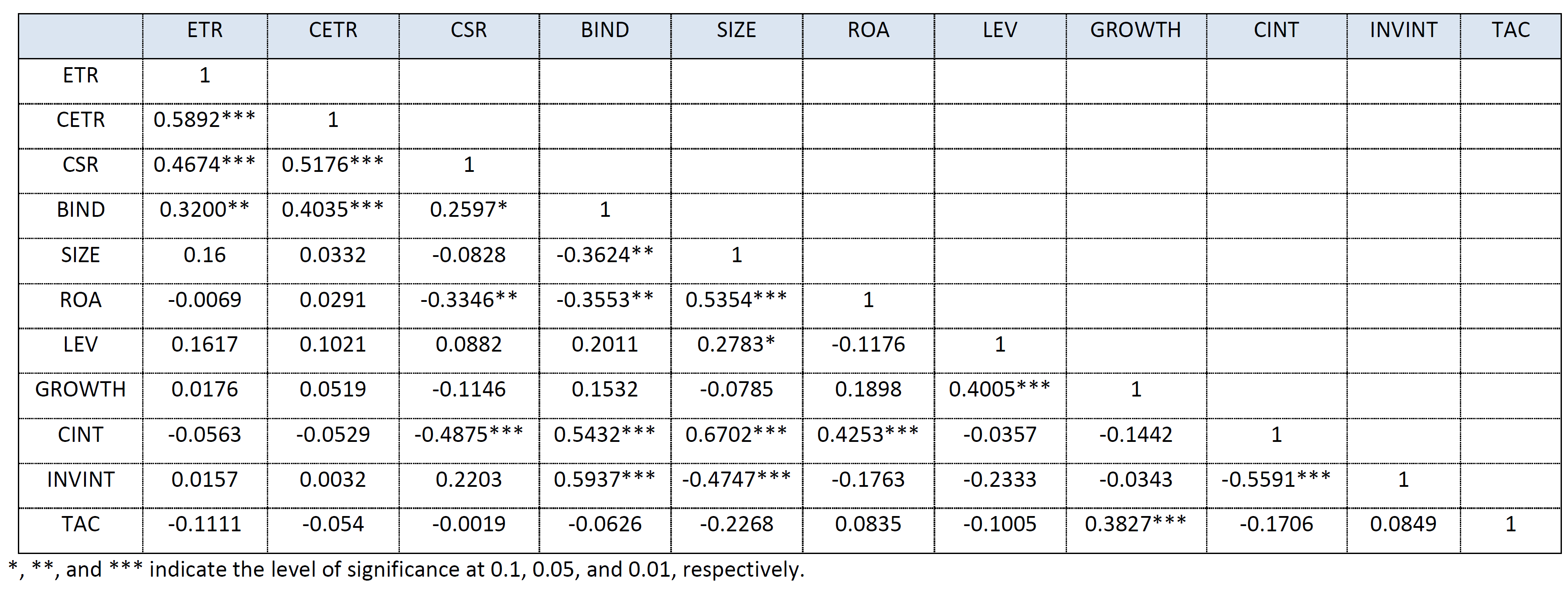

Table 5 illustrates the correlation matrix employed to examine connections among them and evaluate the existence of multicollinearity. Multicollinearity is a concern when a coefficient’s value exceeds 0.8 (Gujarati, 1995). In this study, all coefficient values remain below 0.80. The highest coefficient, 0.67, exists between CINT and SIZE. Consequently, multicollinearity appears insignificant in this analysis.

It can be shown that CSR correlates positively and significantly with both ETR and CETR, demonstrating that the level of engagement in TA practices is lower in firms with a higher tendency to be involved in CSR activities. As BIND is positively and significantly associated with ETR, CETR, and CSR, it can be specified that firms with a higher proportion of independent directors are less likely to engage in TA practices and more prone to participate in charitable activities. It can also be implied that Cambodian companies with superior earnings performance and significant capital intensity are less likely to participate in philanthropic endeavors.

Table 5: Correlation matrix

Multivariate Regression Analysis

Panel regression analysis is employed to investigate the influence of CSR and control variables on TA, as measured by both ETR and CETR. Initially, we conducted a Hausman test to ascertain the appropriateness of random and fixed effect models. The results presented in Table 6 reveal that the random effect model is more suitable for the first two regression models, as indicated by its insignificant p-value for both models.

Table 6: Hausman test for the first two regression models

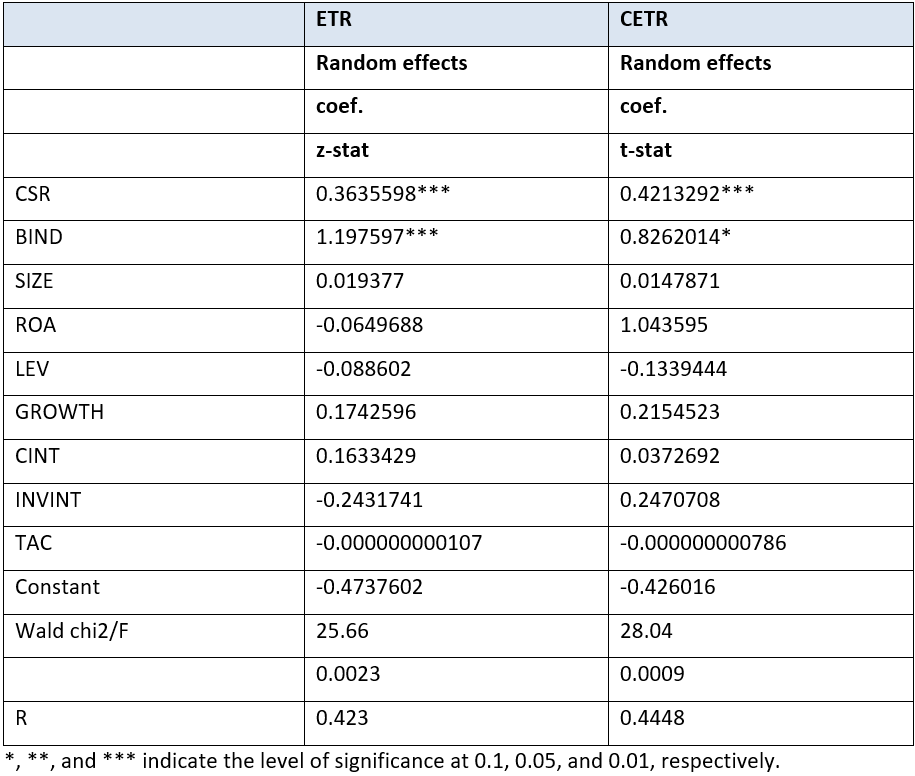

Table 7 displays the regression outcomes for CSR concerning both ETR and CETR. The results reveal positive estimated CSR coefficients in both regression analyses, specifically 0.3930528 and 2.12948, respectively. These coefficients are highly significant, with p-values below 0.01. This suggests that companies’ involvement in TA practices decreases as they exhibit a greater inclination toward charitable contributions or donations. This finding aligns with previous empirical research conducted by Landry et al. (2013), Lanis and Ricardson (2012, 2015), and Watson (2015).

Table 7: Panel Regression of CSR on both ETR and CETR

The above outcomes support the legitimacy theory, indicating that managers of listed Cambodian firms view tax payment as a CSR tool for fostering corporate legitimacy within society. They align with earlier empirical results by Landry et al. (2013), Lanis and Ricardson (2012, 2015), and Watson (2015), which suggest that CSR-focused companies eschew involvement in TA practices.

Panel data regression also explores how board independence moderates the connection between CSR and TA. Similar to prior regression tests, a Hausman test is first performed to determine whether a random or fixed effect model is more appropriate. As shown in Table 8, the random effect model is deemed more fitting for the latter two regression models, as evidenced by its non-significant p-value in both cases.

Table 8: Hausman test for the second two Regression models

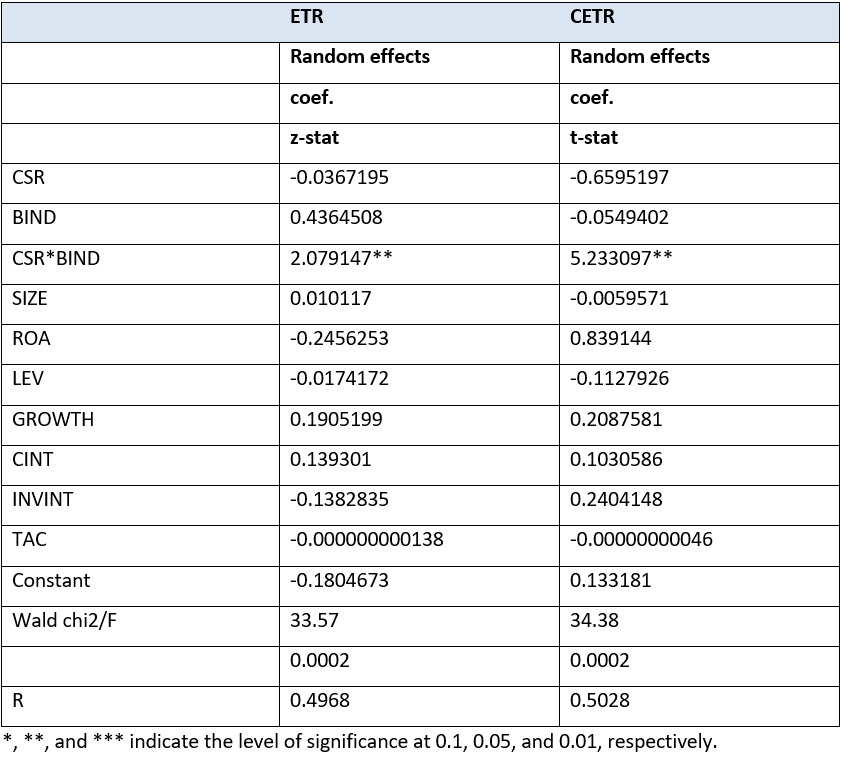

Panel regression results on the effect of the moderating role of board independence on the relationship between CSR and TA measured by ETR and CETR, along with the control variables, are presented in Table 9. In the first model of this table, an interacting variable (CSR*IND) is introduced in the regression, in which ETR measures the TA. It is revealed that CSR*IND (coef = 2.079147, P < 0.05) is significantly positively related to ETR. Thus, this result supports H2, as the results suggest that the negative relationship between CSR engagement and TA is strengthened in firms with a high percentage of independent directors.

The same regression analysis was run in the second model 4, with TA measured by CETR instead of ETR, and the results are fairly similar, as CSR*IND (coef = 5.233097, P < 0.01) is significantly positively related to CETR. The similarity of the results between the two models reflects no difference in the moderating impact of board independence on the relationship between CSR and TA, whether ETR or CETR measures it.

Table 9: Panel Regression of CSR on both ETR and CETR

These findings show that independent directors act with stakeholders’ interests by ensuring that companies comply with paying the fair share of tax besides motivating managers to engage in charitable activities.

CONCLUSION

Although several studies investigated the relationship between corporate social responsibility and tax avoidance, none have concentrated on examining this issue in the context of Cambodia. Therefore, this study delves into whether firms’ involvement in ethical activities in Cambodia stems from maintaining legitimacy within society or risk management by analyzing a sample of 45 firm-year observations from 2014 to 2022. It also investigates whether the association between CSR and TA is moderated by the presence of independent directors with a higher percentage.

After adjusting for firm-specific variables, the empirical results reveal that Cambodian firms emphasizing CSR are less inclined to engage in TA practices. This behavior is also boosted in companies with a higher proportion of independent directors.

This study has certain limitations to consider. Due to data constraints, it primarily relies on firms’ disclosed donation figures in financial statements, which might only partially reflect the genuine extent of CSR involvement. As a result, this could impact the accuracy of CSR assessment. It also depends upon the effective tax rate as a proxy of the engagement in TA practices. However, firms may benefit from various tax incentives, credits, or subsidies that lower their ETR. These benefits might not necessarily reflect aggressive TA but rather strategic tax planning within legal frameworks. It would be useful for future researchers to look at a sample of companies that have won awards with the American Chamber of Commerce regarding CSR and depend upon methodologies other than ETR in assessing the level of engagement in TA practices.

Although constrained by this limitation, it can be considered one of the first studies to explore the relationship between CSR and TA across a sample of Cambodian companies. The outcomes of this paper are also likely to enhance comprehension of CSR among regulators, standard setters, investors, and scholars concerned with ethical business practices. This study, in particular, strengthens the notion that maintaining a positive societal image incentivizes firms to participate in CSR initiatives. Subsequent investigations might explore this matter further by incorporating the moderating influence of diverse ownership structures and governance attributes other than board independence on the correlation between CSR involvement and TA.

REFERENCES

Abid, S., & Dammak, S. (2022). Corporate social responsibility and tax avoidance: The case of French companies. Journal of Financial Reporting and Accounting, 20(3/4), 618-638. https://doi.org/10.1108/JFRA-04-2020-0119

Adhikari, A., Derashid, C., & Zhang, H. (2006). Public policy, political connections, and effective tax rates: Longitudinal evidence from Malaysia. Journal of Accounting and Public Policy, 25, 574-595. https://doi.org/10.1016/j.jaccpubpol.2006.07.001

Amidu, M., Kwakye, T. O., Harvey, S., & Yorke, S. M. (2016). Do firms manage earnings and avoid tax for corporate social responsibility? Journal of Accounting and Taxation, 8(2), 11-27. https://doi.org/10.5897/JAT2016.0218

Anderson, R. C., & Reeb, D. M. (2004). Board composition: Balancing family influence in S&P 500 firms. Administrative Science Quarterly, 49(2), 209-237. https://doi.org/10.2307/4131472

Alsaadi, A. (2020). Financial-tax reporting conformity, tax avoidance and corporate social responsibility. Journal of Financial Reporting and Accounting, 18(3), 639-659. https://doi.org/10.1108/JFRA-10-2019-0133

Armstrong, C. S., Blouin, J. L., Jagolinzer, A. D., & Larcker, D. F. (2015). Corporate governance, incentives, and tax avoidance. Journal of Accounting and Economics, 60(1), 1-17. https://doi.org/10.1016/j.jacceco.2015.02.003

Avi-Yonah, R. S. (2008). Corporate social responsibility and strategic tax behavior. In: Schön, W. (Eds.), Tax and corporate governance. MPI studies on intellectual property, competition and tax law (vol 3., pp 183–198). Springer. https://doi.org/10.1007/978-3-540-77276-7_13

Boivie, S., Withers, M. C., Graffin, S. D., & Corley, K. G. (2021). Corporate directors’ implicit theories of the roles and duties of boards. Strategic Management Journal, 42(9), 1662-1695. https://doi.org/10.1002/smj.3320

Borza, A., & Stoian, C. D. (2011). Managing corporate social responsibility actions through tax avoidance practices. Managerial Challenges of the Contemporary Society, 2, 296-299. https://www.ceeol.com/search/article-detail?id=115717

Carroll, A.B. (1979). A three-dimensional conceptual model of corporate performance. Academy of Management Review, 4(4), 497-505. https://doi.org/10.5465/amr.1979.4498296

Christensen, J., & Murphy, R. (2004). The social irresponsibility of corporate tax avoidance: Taking CSR to the bottom line. Development, 47(3), 37-44. https://doi.org/10.1057/palgrave.development.1100066

Coffey, B. S., & Wang, J. (1998). Board diversity and managerial control as predictors of corporate social performance. Journal of Business Ethics, 17, 1595-1603. https://doi.org/10.1023/A:1005748230228

Dahya, J., & McConnell, J. J. (2005). Outside directors and corporate board decisions. Journal of Corporate Finance, 11(1-2), 37-60. https://doi.org/10.1016/j.jcorpfin.2003.10.001

Davis, A. K., Guenther, D. A., Krull, L. K., & Williams, B. M. (2013). Taxes and corporate sustainability reporting: Is paying taxes viewed as socially responsible? Working paper, University of Oregon.

Desai, M. & Dharmapala, D. (2009). Corporate tax avoidance and firm value. The Review of Economics and Statistics, 91, 537-546. https://doi.org/10.1162/rest.91.3.537

Dhaliwal, D. S., Goodman, T. H., Hoffman, P. J., & Schwab, C. M. (2022). The incidence, valuation, and management of tax-related reputational costs: Evidence from a period of protest. The Journal of the American Taxation Association, 44(1), 49-73. https://doi.org/10.2308/JATA-18-065

Dowling, J. & Pfeffer, J. (1975). Organizational legitimacy: Social values and organizational behaviour. Pacific Sociological Review, 18, 122–136. https://doi.org/10.2307/1388226

Dunn, P., & Sainty, B. (2009). The relationship among board of director characteristics, corporate social performance and corporate financial performance. International Journal of Managerial Finance, 5, 407–423. https://doi.org/10.1108/17439130910987558

Fama, E. F. & Jensen, M. C. (1983). Separation of ownership and control. Journal of Law and Economics, 26(2), 301-325. https://doi.org/10.1086/467037

Fombrun, C. J., Gardberg, N. A., & Barnett, M. L. (2000). Opportunity platforms and safety nets: Corporate citizenship and reputational risk. Business and Society Review, 105(1), 85-106. https://doi.org/10.4337/9781788970693.00006

Friedman, M. (1962). Capitalism and freedom. The University of Chicago Press.

Gujarati, D. N. (1995). Basic Econometrics, USA: McGraw-Hill.

Gulzar, M. A., Cherian, J., Sial, M. S., Badulescu, A., Thu, P. A., Badulescu, D., & Khuong, N. V. (2018). Does corporate social responsibility influence corporate tax avoidance of Chinese listed companies? Sustainability, 10(12), 4549. https://doi.org/10.3390/su10124549

Gupta, S. & Newberry, K. (1997). Determinants of the variability in corporate effective tax rates: Evidence from longitudinal data. Journal of Accounting and Public Policy, 16(1), 1-34. https://doi.org/10.1016/S0278-4254(96)00055-5

Hanlon, M., & Heitzman, S. (2010). A review of tax research. Journal of Accounting and Economics, 50(2), 127-178. https://doi.org/10.1016/j.jacceco.2010.09.002

Hill, C. W. & Jones, T. M. (1992). Stakeholder‐agency theory. Journal of Management Studies, 29(2), 131-154. https://doi.org/10.1111/j.1467-6486.1992.tb00657.x

Hillman, A. J., Cannella, A. A., & Paetzold, R. L. (2000). The resource dependence role of corporate directors: Strategic adaptation of board composition in response to environmental change. Journal of Management Studies, 37(2), 235-256. https://doi.org/10.1111/1467-6486.00179

Hillman, A. J., & Dalziel, T. (2003). Boards of directors and firm performance: Integrating agency and resource dependence perspectives. Academy of Management Review, 28, 383-396. https://doi.org/10.5465/amr.2003.10196729

Hoi, C. K., Wu, Q., & Zhang, H. (2013), Is corporate social responsibility (CSR) associated with tax avoidance? Evidence from irresponsible CSR activities. The Accounting Review, 88(6), 2025-2059. https://doi.org/10.2308/accr-50544

Huseynov, F., & Klamm, B. K. (2012). Tax avoidance, tax management and corporate social responsibility. Journal of Corporate Finance, 18(4), 804-827. https://doi.org/10.1016/j.jcorpfin.2012.06.005

Ibrahim, N. A., & Angelidis, J. P. (1995). The corporate social responsiveness orientation of board members: Are there differences between inside and outside directors? Journal of Business Ethics, 14(5), 405-410. https://doi.org/10.1007/BF00872102

Ibrahim, N. A., Howard, D. P., & Angelidis, J. P. (2003). Board members in the service industry: An empirical examination of the relationship between corporate social responsibility orientation and directorial type. Journal of Business Ethics, 47(4), 393-401. https://doi.org/10.1023/A:1027334524775

Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305-360.

Jo, H., & Harjoto, M. A. (2011). Corporate governance and firm value: The impact of corporate social responsibility. Journal of Business Ethics, 103(3), 351-383. https://doi.org/10.1007/s10551-011-0869-y

Johnson, R. A., & Greening, D. W. (1999). The effects of corporate governance and institutional ownership types of corporate social performance. Academy of Management Journal, 42(5), 564-576. https://doi.org/10.5465/256977

Jones, S. (2012) Principles of Taxation for Business and Investment Planning. 14th ed., McGraw Hill.

Jones, T. M. (1995). Instrumental stakeholder theory: A synthesis of ethics and economics. Academy of Management Review, 20(2), 404-437. https://doi.org/10.5465/amr.1995.9507312924

Kavadis, N., & Thomsen, S. (2023). Sustainable corporate governance: A review of research on long‐term corporate ownership and sustainability. Corporate Governance: An International Review, 31(1), 198-226. https://doi.org/10.1111/corg.12486

Knuutinen, R. (2013). International tax planning, tax avoidance and corporate social responsibility. Interdisciplinary Studies Journal, 3(1), 73-84.

Laguir, I., Staglianò, R., & Elbaz, J. (2015). Does corporate social responsibility affect corporate tax aggressiveness? Journal of Cleaner Production, 107, 662-675. https://doi.org/10.1016/j.jclepro.2015.05.059

Landry, S., Deslandes, M., & Fortin, A. (2013). Tax aggressiveness, corporate social responsibility, and ownership structure. Journal of Accounting, Ethics and Public Policy, 14, 611-645. http://dx.doi.org/10.2139/ssrn.2304653

Lanis, R., & Richardson, G. (2012). Corporate social responsibility and tax aggressiveness: An empirical analysis. Journal of Accounting and Public Policy, 31(1), 86-108. https://doi.org/10.1016/j.jaccpubpol.2011.10.006

Lanis, R., & Richardson, G. (2011). The effect of board of director composition on corporate tax aggressiveness. Journal of Accounting and Public Policy, 30(1), 50-70. https://doi.org/10.1016/j.jaccpubpol.2010.09.003

Lanis, R., & Richardson, G. (2015). Is corporate social responsibility performance associated with tax avoidance? Journal of Business Ethics, 127(2), 439-457. https://doi.org/10.1007/s10551-014-2052-8

Lee, B. B., Dobiyanski, A., & Minton, S. (2015). Theories and empirical proxies for corporate tax avoidance. Journal of Applied Business & Economics, 17(3), 21-34.

Lenz, H. (2020). Aggressive tax avoidance by managers of multinational companies as a violation of their moral duty to obey the law: A Kantian rationale. Journal of Business Ethics, 165(4), 681-697. https://doi.org/10.1007/s10551-018-4087-8

Lev, B., Petrovits. C., & Radhakrishnan, S. (2010). Is it doing good for you? How corporate charitable contributions enhance revenue growth. Strategic Management Journal, 31(2), 182-200. https://doi.org/10.1002/smj.810

López‐González, E., Martínez‐Ferrero, J., & García‐Meca, E. (2019). Does corporate social responsibility affect tax avoidance: Evidence from family firms. Corporate Social Responsibility and Environmental Management, 26(4), 819-831. https://doi.org/10.1002/csr.1723

Mamatzakis, E., Pegkas, P., & Staikouras, C. (2023). The impact of debt, taxation and financial crisis on earnings management: The case of Greece. Managerial Finance, 49(1), 110-134. https://doi.org/10.1108/MF-01-2022-0052

Minnick, K., & Noga, T. (2010). Do corporate governance characteristics influence tax management? Journal of Corporate Finance, 16(5), 703-718. https://doi.org/10.1016/j.jcorpfin.2010.08.005

Moser, D. V., & Martin, P. R. (2012). A broader perspective on corporate social responsibility: Research in accounting. The Accounting Review, 87(3), 797-806. https://doi.org/10.2308/accr-10257

Muller, A., & Kolk, A. (2015). Responsible tax as corporate social responsibility: The case of multinational enterprises and effective tax in India. Business and Society, 54(4), 435-463. https://doi.org/10.1177/0007650312449989

Ostas, D. T. (2004), Cooperate, comply, or evade? A corporate executive’s social responsibilities with regard to law. American Business Law Journal, 41(4), 559-594.

Pandapotan, F. (2023). The influence of corporate social responsibility on tax avoidance. Journal of Applied Business, Taxation and Economics Research, 2(3), 258-265. https://doi.org/10.54408/jabter.v2i3.158

Park, S. (2017). Corporate social responsibility and tax avoidance: Evidence from Korean firms. Journal of Applied Business Research, 33(6), 1059-1068. https://journals.klalliance.org/index.php/JABR/article/view/364

Pfeffer, J. M., & Salancik, G. R. (1978). The external control of organizations: A resource dependence perspective. Harper & Row.

Post, C., Rahman, N., & Rubow, E. (2011). Green governance: Boards of directors’ composition and environmental corporate social responsibility. Business & Society, 50(1), 189-223. https://doi.org/10.1177/0007650310394642

Preuss, L. (2010). Tax avoidance and corporate social responsibility: You can’t do both, or can you? Corporate Governance, 10(4), 365–374. https://doi.org/10.1108/14720701011069605

Rabbi, F., & Almutairi, S. S. (2021). Corporate tax avoidance practices of multinationals and country responses to improve quality of compliance. International Journal for Quality Research, 15(1), 21-44. https://doi.org/10.24874/IJQR15.01-02

Ramzan, M., Amin, M., & Abbas, M. (2021). How does corporate social responsibility affect financial performance, financial stability, and financial inclusion in the banking sector? Evidence from Pakistan. Research in International Business and Finance, 55, 101314. https://doi.org/10.1016/j.ribaf.2020.101314

Rehman, Z. U., Khan, A., & Rahman, A. (2020). Corporate social responsibility’s influence on firm risk and firm performance: the mediating role of firm reputation. Corporate Social Responsibility and Environmental Management, 27(6), 2991-3005. https://doi.org/10.1002/csr.2018

Richardson, G., Taylor, G., & Lanis, R. (2013). The impact of board of director oversight characteristics on corporate tax aggressiveness: An empirical analysis. Journal of Accounting and Public Policy, 32(3), 68-88. https://doi.org/10.1016/j.jaccpubpol.2013.02.004

Riskiyadi, M., & Tarjo, A. (2021). Uncovering Tax Avoidance at Government Agencies: A Phenomenological Research. Jurnal Ilmiah Akuntansi dan Bisnis, 17(1), 22-32. https://ojs.unud.ac.id/index.php/jiab

Rose, J. M. (2007). Corporate directors and social responsibility: Ethics versus shareholder value. Journal of Business Ethics, 73(3), 319-331. https://doi.org/10.1007/s10551-006-9209-z

Sahin, K., Basfirinci, C. S., & Ozsalih, A. (2011). The impact of board composition on corporate financial and social responsibility performance: Evidence from public-listed companies in Turkey. African Journal of Business Management, 5(7), 2959-2978. https://doi.org/10.5897/AJBM10.1469

Salhi, B., Al Jabr, J., & Jarboui, A. (2020). A Comparison of Corporate Governance and Tax Avoidance of UK and Japanese Firms. Comparative Economic Research. Central and Eastern Europe, 23(3), 111-132.

Sekaran, U., & Bougie, R. (2016). Research methods for business: A skill building approach. John Wiley & Sons.

Shaukat, A., Qiu, Y., & Trojanowski, G. (2016). Board attributes, corporate social responsibility strategy, and corporate environmental and social performance. Journal of Business Ethics, 135(3), 569-585. https://doi.org/10.1007/s10551-014-2460-9

Stickney, C., & McGee, V. (1983). Effective corporate tax rates the effect of size, capital intensity, leverage, and other factors. Journal of Accounting and Public Policy, 1, 125-152. https://doi.org/10.1016/S0278-4254(82)80004-5

Vo, D. H., Van, L. T. H., Hoang, H. T. T., & Tran, N. P. (2023). The interrelationship between intellectual capital, corporate governance and corporate social responsibility. Social Responsibility Journal, 19(6), 1023-1036. https://doi.org/10.1007/BF00872318

Wang, J., & Dewhirst, H. D. (1992). Boards of directors and stakeholder orientation. Journal of Business Ethics, 11, 115-123. https://doi.org/10.1007/BF00872318

Watson, L. (2015), Corporate social responsibility, tax avoidance, and earnings performance. The Journal of the American Taxation Association, 37(2), 1-21. https://doi.org/10.2308/atax-51022

Webb, E. (2004). An examination of socially responsible firms’ board structure. Journal of Management and Governance, 8(3), 255-277. https://doi.org/10.1007/s10997-004-1107-0

Wierzbicki, J., & Werner, A. (2023) Tax compliance: Development of the concept and change of approach. In Karwat et al. (Eds.), Tax compliance and risk management (1st ed., pp. 25-50). Routledge.

Zaid, M. A., Abuhijleh, S. T., & Pucheta‐Martínez, M. C. (2020). Ownership structure, stakeholder engagement, and corporate social responsibility policies: The moderating effect of board independence. Corporate Social Responsibility and Environmental Management, 27(3), 1344-1360. https://doi.org/10.1002/csr.1888

Zeng, T. (2016), Corporate social responsibility, tax aggressiveness, and firm market value. Accounting Perspectives, 15(1), 7-30. https://doi.org/10.1111/1911-3838.12090

Zeng, T. (2018) Relationship between corporate social responsibility and tax avoidance: International evidence. Social Responsibility Journal, 15(2), 244-257. https://doi.org/10.1108/SRJ-03-2018-0056

Zimmerman, J. (1983). Taxes and firm size. Journal of Accounting and Economics, 5(2), 119-149. https://doi.org/10.1016/0165-4101(83)90008-3